HDFC life has come up with one of its kind unit linked insurance plan with name HDFC life Click 2 invests. Why it is unique is because it is devoid of many charges that generally ULIP insurance plans have. It doesn’t have any allocation charge, administration charge and even the discontinuation charge. HDFC life click 2 invest can be bought online only and thus does not have any distribution cost attached too. But even after its no charge structure, does it make sense to invest in HDFC click 2 invest insurance plan. Let’s find out.

HDFC life click 2 invest – Key features

HDFC Life click 2 invest is an online unit linked insurance policy. Like any other ULIP you have to decide on the premium you want to pay, depending on which you will be covered with insurance. As in ULIP insurance cover will be the multiples of premium you pay.

Premium you pay after deduction of allocation charges (which is NIL in this product) will get invested in the fund option you chose. There are 8 fund options available for investors in this plan.

With a single, limited and regular premium pay option the maximum policy term available is of 20 years. You keep on paying the premiums and at maturity you will get the fund value accumulated or at death your nominees will get highest of the following:

- Sum Assured

- Fund value

- 105% of the premium paid

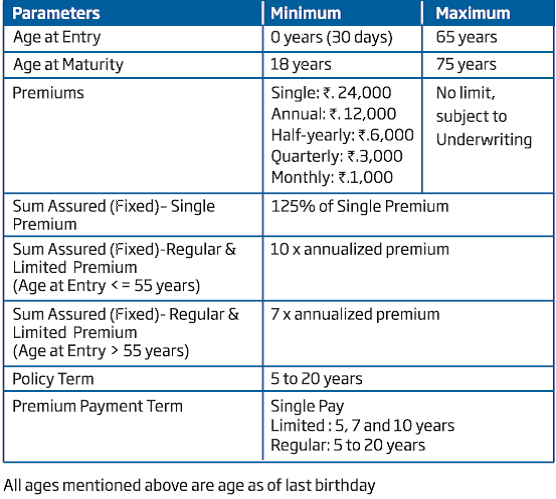

HDFC life click 2 invest – eligibility and other conditions

HDFC life click 2 invest – Other Features

- Charges: There is no Allocation, administration charges in this policy. There’s a fund management charge of 1.35% and being an insurance plan there’s mortality charges too. ULIP charges are also subjected to service tax.

- Discontinuation: There are no discontinuance fund charges. But if you discontinue the premium payment before the minimum tenure of 5 years, then the risk cover will cease and the fund value as on date of discontinuance will be moved to discontinue fund portfolio where you will get minimum guaranteed interest rate @ 4% p.a. You will be able to withdraw the funds only after completion of minimum of 5 years tenure.

- Partial Withdrawal: You can also make partial withdrawal after completion of 5 policy years. First 4 withdrawals in single policy year is free, subsequent withdrawals will be charged.

- Switch and Re direction: You may also switch the invested amount to some other funds of your choice or even redirect the premium payments.

- Surrender: You can surrender the policy in between, but if you do it with in first 5 years, your fund value will be shifted to discontinued fund and can be withdrawn only after 5 years.

- Settlement: There’s one settlement option too, where you can claim the maturity proceeds in monthly installments for 5 years. But as in accumulation phase, even in settlement phase investment risk will be borne by you.

HDFC life Click 2 Invest – Should you invest?

The reason this plan is different but no different for me is the charge and investment structure. Where ULIPs are generally full of charges, this plan has no charges at all. Mortality charges are meant to be there being an insurance plan and fund management charges are due to investment structure attached to it.

The main point of contention to me is the ULIP investment structure. I mean i have never been able to answer the question of why should someone invest in ULIP or even endowment, for investments or insurance or for both?

If this is for insurance, then will the investor be able to pay enough premium and that too regularly to buy adequate insurance cover? Say for e.g. If a healthy nonsmoker male needs an insurance cover of Rs 20 lakh, then in case of HDFC life click 2 protect (term insurance) he will pay Rs 3798/- p.a. of premium, where as in case of HDFC life click 2 invest or any insurance ULIP plan he needs to shell out Rs 2 lakh p.a.

Even if one has enough money to pay for premium, how one can be sure that he’ll be able to answer this commitment every year (at least from next 5 years)

If this is for investments looking at low fund management charges, then how would you track the funds performance, compare it among peers and above all by any chance you find that funds are not performing as expected, what options you are left with. You have to continue with this structure and keep on paying the premium for at least 5 years and if you don’t you will get returns of discontinuance fund account.

On the other side investments products like mutual funds, PPF, bank FDs, Post office schemes etc. all are so flexible and one can invest as per his requirement and manage comfortably.

Conclusion:

Even though hdfc life click 2 invest is devoid of all unnecessary charges, I am still not convinced to advise on investing in this. My advice is still the same keep insurance and investments separate. Buy adequate insurance cover through term insurance plans and do investments in pure investment products as per your short and long term goals and risk profile. Keep your investments simple and flexible.

How do you find hdfc life click 2 invest? Do you agree with my views?

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.

Manikaran Singal is the founder and Chief financial planner at Good Moneying Financial Solutions. He is a CERTIFIED FINANCIAL PLANNER CM and SEBI registered Investment adviser (Regd no. INA 100001620). He’s having 20+ years of experience in financial services space.")

{kind=link}

I fully agree with your observations.

Thanks Rajiv.

Dear Mr.Singal,

“My advice is still the same keep insurance and investments separate”… is not just a simple sentence for this article.. It have real life meaning & implication. I learned this after loosing.

After separating insurance and investment, at present I feel more secure & flexible, than before.

Thanks for Quoting.

– Partho

Dear Mr Partho

What i can understand from your comment is you have bitter experience with the package of insurance and investments. Can i request you to share your experience for the benefit of other readers.

I am sure you can make other people’s financial life better by not letting repeat the same mistakes again.

regds

HI,

Can you suggest any pure invest plans?

Bank FD, PPF, Post office schemes, Mutual funds, Tax free bonds etc. all are pure investments plan

Come on…it’s a pretty good option considering it’s tax exempt…debt funds aren’t…and you can switch between asset classes easily…that’s pretty cool…

Ur idea of keeping investment n insurance separate looks like old tag line… They are offering 9 funds and hdfc has a past records of giving competitive return as mutual fund.. I have a ulips which is giving me average of 25% since 2006. I have played the game of timely switching once in 2 years . IF I continue doing so with this I can earn much more tax free under sec 10(10) d… This is a awesome product in the market.. n what more u can expect from a company… just 1.35% pa with full transperancy.. is better than 2.5% in mutual funds where many cost are hidden…

Your ULIPs are generating 25% ( i assume this is per annum though you have not mentioned it) since 2006, that’s a pretty nice return. And if you as an investor is getting this much return after allocation, administration, FMC and Mortality charges…that’s a gain commendable. because generally investments generate returns but investors don’t enjoy the same.

I also appreciate your game of “timely” switching once in 2 years, as i have never been able to time the market. Parul, you are really a Smart Investor.

Though i have already mentioned my points of contention, but just to reply your comment, i would like to reiterate the same….

” The main point of contention to me is the ULIP investment structure. I mean i have never been able to answer the question of why should someone invest in ULIP or even endowment, for investments or insurance or for both?

If this is for insurance, then will the investor be able to pay enough premium and that too regularly to buy adequate insurance cover? Say for e.g. If a healthy nonsmoker male needs an insurance cover of Rs 20 lakh, then in case of HDFC life click 2 protect (term insurance) he will pay Rs 3798/- p.a. of premium, where as in case of HDFC life click 2 invest or any insurance ULIP plan he needs to shell out Rs 2 lakh p.a.

Even if one has enough money to pay for premium, how one can be sure that he’ll be able to answer this commitment every year (at least from next 5 years)

If this is for investments looking at low fund management charges, then how would you track the funds performance, compare it among peers and above all by any chance you find that funds are not performing as expected, what options you are left with. You have to continue with this structure and keep on paying the premium for at least 5 years and if you don’t you will get returns of discontinuance fund account.”

I still find Bank FDs, Mutual funds etc. are much more easily manageable, and pls note that no charges are hidden in those products.

ManiKaran, I am a small investor without much knowledge of finance and economy. But I dont tend to agree on your statement about the Insurance part of ULIP. You said in case of term insurance with 20 lakh cover, one just pays Rs 3798 Per annum whereas in case of ULIP the same person has to shell out 2 lakh per annum. I am sure you know that 2 lakh per annum goes towards your investment and not towards your mortality charges. The mortality charges are same or comparable to the term insurance. I dont know how can you make such as assumption.

Secondly you said what will one do if the fund doesnt perform? There are more than 5 equity funds to chose from you can switch to them. and in case of a fall in the market you can switch to debt fund which is not possible in mutual fund.

Hope you agree with my rationale.

Hi parul, I am also interested in hdfc C2I plan as i can see total charges including FMC and risk charges are 2% which is at par with usual SIP charges 2-2.5%.so we can get life cover with no extra cost.

I understand it has a locking period of 5 yrs but then for tax exemption we have to put money in ELSS also for 5 yrs.if anyone has taken any other traditional plan then i think he can go for this plan.

Can you please provide some info about returns u got so far.

Dear manikaran singal,

I am Avinash had started a policy in click to invest with monthly invested of 2000/.i selected equity plus bond 20%. and the other 80% i kept in bond fund. so i kept in 15 year time period. hence guide me whether i placed the money in correct investment or not. if this policy i selected is risk means i am ready to withdraw it.

Hence please guide me

Avinash, the fund selection is totally dependent on your risk profile and risk tolerance level. generally when investment is for 15 years time frame then investment allocation should be more into equity and not debt.

Hi ,

I am planning to take this policy considering the tax savings and investments where i can save my tax in 80c and at the time of maturity with 10 d tax rules, but reading your comments i am again stuck how about if i go with mutual funds as you said … will i get the good returns and tax exemptions

Sandani, you will definitely get good returns and tax exemptions in ELSS. See this HDFC policy and ELSS Mutual funds both are market linked products, so if you want to generate returns from equity exposure then i believe ELSS could be a better option which like ULIP will keep the taxation to NIL on maturity proceeds.

Hi.

I am not agreed with your statement. In Elss you are going to put your money in single fund.However in Hdfc ULip plan has 8 different fund option to invest .So investers can reduce the market risk. And Every elss has minimum charges is 2% to 2.5% per year .However same in Hdfc Click 2 invest Ulip has 1.35% per year only..Now This is about charges comparison. Now lets talk about returns.

Check the elss return.

https://www.valueresearchonline.com/funds/newsnapshot.asp?schemecode=10826&&utm_medium=vro.in

Check the hdfc click 2 invest opportunity fund return.

http://www.moneycontrol.com/insurance/ulip/hdfc-standard-life-insurance-HD/hdfc-life-progrowth-plus-opportunities-fund-IHD391.html

All The best 🙂

Hi Sir,

Myself Gowrishankar, 30yrs old and i want to invest for my child (6 months) old. Some one has suggested to invest in hdfc click to invest and i want to go for long term period between 15 to 20yrs which will be useful or benefit to my child education or marriage. Help to go for investment plan or insurance plan(kindly suggest me if any better scheme available)

Gowrishankar, its a question of your child’s future. Plan properly. Rather than buying a single product you should chalk out a suitable plan for your kid. Make estimate of the expenditure on education and marriage and start saving through open ended mutual funds, PPF and other debt instruments as suitable to your risk tolerance. Get yourself adequately insured so in case of your absence his future should not be at risk.

And the most important point…don’t ignore your retirement planning while saving for your child. Always remember, you can get loan for children education but not for your retirement.

I am 27 year unmaried men. Looking for my first investment. My yearly saving is Rs.12000/-. What is good policy for me? I want good maturity fund after 15 year.. which is best for me “Hdfc click 2 invest or SBI PPF??????

Anil , first of all congratulations for starting with your investment life. I would advise you to divide the money into PPF and balanced equity oriented mutual funds. Though i can understand you want to stay invested for 15 years, but still this is your start of investments. Learn more about the various options, understand the pros and cons and slowly and gradually build your portfolio with proper planning.

ULIP plans will become more unpopular in coming days as people are analyzing them gradually. Even with so many attracting features HDFC click 2 invest is able offer very bad life cover and return. Complete disappointment.

I have a reason to invest in this HDFC ULIP. So, can I ask here to get your feedback or you are no longer monitoring the comments on this post?

Thanks!

Mahesh, regarding HDFC Click to invest i have already shared my feedback in the post itself. If there’s any specific question related to this product, feel free to ask.

Hi Manikaran,

Yes, my question is about ULIP itself (specific to this HDFC Plan). I can see that no one actually recommends an ULIP plan — whether it’s for investment or for insurance. And I also agree that it makes sense to buy a term insurance cover (for insurance) + an ELSS (for investment & 80c benefits).

When I read about this hdfc plan I felt that its a better choice for me (correct me if am wrong or missing something here).

I do not have a term insurance cover so.. I was considering this ULIP plan as they are offering upto 40 times coverage (on ther website its written as 10x but they told me that they are offering upto 40x -–will confirm that before buying). I am actually not interested in their Equity fund as I prefer to invest in stocks myself. But still…. I can switch from debt to equity when there is, say a 20-30% stock market correction.

Do you think that this strategy is better than ELSS + Term Insurance?

My goal is to save tax and at the same time to get insurance benefits as I do not have a term insurance plan. Also, I want to make sure that the ROI is positive after 5 years. I might have preferred ELSS over ULIP if it had the ability to switch between debt/equity. But I was unable to find an ELSS fund that gives us the flexibility to switch between debt and equity. All of them were equity only fund (let me know if there is a hybrid fund available).

They say those ELSS offered say 20% or 30% returns over the past two years. But I do not want to trust that. Because the market can crash anytime and if I invest in ELSS today the fund value could be negative after 3 years if a 20 to 30% correction happend before that.

Thanks a lot!

Switching from debt to equity when market is down is a strategy which looks good on papers but i have not seen anyone practically applying it. We all are suffering from some investment biases which restrain us from taking rational decisions.

Investor switch to equity at 15% fall, but market does not stop there and fell another 20%. Now the investors portfolio is 20% down. Market doesn’t recover for next 6 months. Losing patience, investor switch back the negative portfolio again to debt just to make sure that it should not fall further and one can enjoy the safe returns. And after few months, mkt bounced back and gave 50% return. This is something which is a real life example of one of my friend who wants to follow buy on dip strategy.

See the key is not in timely switching but following a process. Follow Asset Allocation, with a proper allocation into debt, equity, gold. You don’t know which side , which asset class will move. So balance it out and take the benefit of both worlds. Rebalance your portfolio timely to book profit or get into down market.

Go for term plan, as the premium would be small which you can continue paying without bothering about the expenses or economy.

Hi Manikaran,

Thanks a ton for that. Btw, the HDFC guy gave the wrong information about its insurance part. The premium for insurance (when the coverage is high) is actually higher than traditional term plans.

But without insurance benefits (that is with single premium plan)… this ULIP plan still looks good as I checked the historical NAV of its debt funds.

So, now considering this ulip debt fund (to save tax) and an online term insurance.

Thanks! 🙂

Hi I am atul, 44 years old, planning to go for click 2 investment plan (1.5 lakh / year premium). please advice

Hi Atul. Would request you to please go through the article once again and come up with specific queries.

Sir

I want to invest rs 5000 per month in hdfc click to invest for 15-20 years. Kindly suggest me to divide my amount so that I can get good returns. And also tell me how much life insurance cover will I get since I do not have any life insurance cover. And is it safe to do online cuz I m frequently getting calls from policy bazar. Please suggests

Sir

I want to invest rs 5000 per month in hdfc click to invest for 15-20 years. Kindly suggest me to divide my amount so that I can get good returns. And also tell me how much life insurance cover will I get since I do not have any life insurance cover. And is it safe to do online cuz I m frequently getting calls from policy bazar. Please suggests

Hello sir

sir we are recently blessed with a angle angle our place. now I m ok in forward to invest 50000 rs in longterm which also gives me tax be night.

plz suggest me where should i invest my money.

Hi,

Can you also give feedbacks on New Endowment plan of LIC. Is it better to invest in this plan then investing in ULIPS.

Dear Sir,

i have doing job .

Recently I Have Purchase HDFC Click 2 Invest plan and Started 5000 rs. quaterly for 10 yrs.

please guide me that future of this Investment ?

can it is given profit to me in future ?

Amit, you are asking wrong question at wrong time. This should have been asked before investing.

Structure wise product is good, but i can’t comment on performance , as it is a ULIP and Investment wise not much data is available in public domain.

Dear sir,

I am having this click2protect, as you mentioned in your findings I find it very difficult to allocate my funds. My fund values are keep on going down. Can you please suggest What will be the best areas that I can switch my funds.

My present portfolio is as follows

Fund Name * Unit Price (Rs.) Unit Balance Fund Value (Rs.)

Income Fund 16.13570 638.61294 10,304.47

Balanced Fund 15.12220 623.13538 9,423.18

Blue Chip Fund 15.50580 301.76483 4,679.11

Opportunities Fund 19.47530 257.90278 5,022.73

Equity Plus Fund 10.26010 1,726.74515 17,716.58

Total 47,146.07

Hope you understood my query, an awaiting your response

Thank you

Kishore

Mr Kishore, i don’t track ULIP funds. You better contact your insurance agent or HDFC Life people for this.

Hi Manikaran,

NEED YOUR ADVICE.

recently i bought HDFC click2invest for 12000/ pm for 20 years through policy bazar.

I did not want to choose it, my 1st choice was mutual fund.

But the policy bazar guy convinced me to go for it…as it will have more returns compare to any mutual fund.

he showed me in money control web site as it how performing in last 3 years i.e 25% returns in opportunity fund.

Now by going through your article i doubt whether it will at least 10% returns.

If you will suggest i will withdraw it as i have not submitted the documents.

Hi Satish…See this happens when your focus is only on returns and numbers. Numbers can deceive easily. I will not comment on returns, but on convenience of withdrawal and investment. You stop paying in MF nothing will happen, you can redeem easily and move your money to some other fund, this is not the case in Insurance policies. You have to continue paying the premiums at least for first 5 years otherwise your policy will get taxable, you have to take insurance cover and pay mortality costs as compulsion even if you don’t require it.

See, as per me Mutual funds are easy to operate and manage.

Sir I want to invest 1000 per month for 5 year to get a high return.suggest me where and how should invest

Hello Sir,

As I am planning for 20 years with good return, also want to cover up my investment under 80 C.

So I have considered few option-

1. HDFC Click to invest – ULIP

2. Axis LT Equity Fund(G) – ELSS

3. Franklin India Taxshield(G) – ELSS

4. ICICI Pru LT Equity Fund (Tax Saving)(G) – ELSS

Could you please suggest where I should invest.

Thanks,

Prashant

AXIS and Franklin has good ELSS products, with consistent track. Avoid ULIP . Keep reviewing, and better to have a financial plan first before you start with any investment

Dear Sir,

I am 38 old and have set retirement age of 55. I would want a monthly return of 1 lakh per month upon retirement for up to 90 years . How much should i invest monthly for 15 years to attain that figure.

Kindly advise

warm Regards

Sanjana

You want maths behind it. Though i will reply your query, but keep in mind that all maths in financial planning is based on some assumptions which may or may not be right. As you have assumed that you will live upto 90 years of age, and what could be required post retirement is Rs 1 lakh per month

1 lakh at present will be around Rs 275903 after 15 years @7% inflation. What you require is Rs 2.75 lakh per month for next 35 years adjusted to inflation. I am assuming that after retirement you would not prefer to park much of money volatile instruments and would be able to generate return of 8% post tax from your investment management. This results into 1% of real return assuming inflation continues to be 7% post retirement. Considering all this you would need a corpus of Rs 9.77 crore at the age of 55.

To reach this corpus if you invest in a portfolio which generates 12% of annualsed return, then you need to invest 1.95 lakh per month.

Hi Mani,

I am an IT professional, I have invested in HDFC Click to Invest quarterly for Rs, 12,500/- make Rs,50,000 annually. Initially I invested in Balanced Fund for 6 months however after checking the Fund Value in -tive I have switched 80% to equity and 20 to Balanced Fund as of now.

After going through many Blogs I am confused now, rather than doing more damage in paying premium, will you recommend to discontinue the ULIP and buy a Term and Start SIP’s in ELSS? Or Should I continue with the same and then surrender after 4.5 years? Also I am investing in SIP in equity for long term additionally.

Please revert!

Thanks,

Kunal.

Though i don’t recommend anyone to go with ULIP at the first place and the reasons i have properly explained in my article only. Term plan in any case is must with high sum assured even if you continue with this policy.

Now question of continuing this policy or not, totally depends on your requirement, any near term goals. Keeping all other things constant and assuming that you have other arrangements at place, you may continue with this plan but with 100% of equity allocation and without bothering about its performance in 6-18 months time frame. i am assuming that you are young and have 20 years or more of time frame left with you for investment.

Don’t play with allocation. Just decide upon your overall required asset allocation in your financial plan and stick to it.

Please guide, my age is 30 & married too.

I am planning to buy “HDFC click to invest” with 5 year term, please guide me is it worth buying.

I want this for tax saving, or should i go for 5 year FD option.

Equity is not for 5 years horizon. and FD also does not suit in 5 years term. If it is for investment then better to have a mix of equity and debt. You seem to be a conservative investor, so my view for your tax saving investments should be mix of ELSS mutual funds and FD. Else, its better to have your financial planning done and your financial planner will guide you what suits you best .

I am Amiya Ranjan from Vishakhapatnam.

Today i brought HDFC click to invest plan with Rs 3000/months. with following options

Blue chip fund: 30%

opportunity fund: 30%

Balance fund: 20%

Bond Fund: 20%

I purchased this plan through policybazar. They shown me the above funds are performing well from last two years. Also I have checked the performance of the above funds in moneycontrol website. The performance shown as below.

Absolute return in Bluechip Fund in last two years: 20.20%

Absolute return in opportunity Fund last two years: 37.90%

Absolute return in balance fund in last two years last two years: 21.81%

Absolute return in Bond fund in last two years last two years: 21.10%

If we see these figures then it looks attractive. But still I want your suggestion to continue with plan or shall I discontinue this plan as I am in free look period of 15 days.

Waiting for your reply.

See, my concern is not performance but the ULIP structure in itself. Hope you have gone through my article in detail. I am not in favor of ULIPs at all.

I have burnt my fingers badly by investing in HDFC young Star a decade back . The returns were negative ,terms draconian and customer care poor .

In C2I , allocation charges are nil and advangate touted is switching to save when market is down . Very much like switching to lower gears in cars when we face slower speed . In your experience , is it possible to predict and switch in time to save ?

In case of pure MF investment , not only is allocation charge higher , but in case of panic exit , gains would be taxable in short term.

Also , a down turn after 2 good years will wipe out all the gains in third year (principal*1.15*1.15*.85 = 12% gain only). A good fund manager would sense a downturn and save the 15% drop on overall fund . Is there some scheme where such switching is possible without an ULIP ?

Mr. Bhat, there’s no way one can predict the market movements. NO ULIP or NO MF/Fund manager can do that. That’s why it is the investor who will bear the market risks. In HDFC C2I, there may not be any allocation charges, but there are Insurance charges which you may not want or required to pay. Also there’s no flexibility to come out of the scheme if the Fund is not performing well, unlike Mutual funds ( through there may be some exit load or even taxation)

You can have a fund with a structured process, which can reduce the equity exposure depending on market valuation and increase the same in lower valuation. These structures are there to mitigate the risks, but returns are something which are not guaranteed. To reduce the MF costs you may go with DIRECT Funds which are sans distributor charges, and manage the portfolio on your own.

You have to bear the volatility and in long term returns will also get averaged out.

Hi, I invested in this plan and seeing a loss in 6 months period. My payment period is 5 years and policy period is 10 years. I invested in Balanced fund for 5 months and last I redirected the amount to Income fund. Please suggest what can be done about it as its not too late to act upon it.

Arshal, first thing first 6 months is too less a time frame to judge the performance. You should not make frequent changes. I have given my views about product in the article itself, but for the portfolio allocation and fund selection you should better consult a financial planner or ask your insurance advisor to guide you properly as per your risk profile and goals targeted

Hi, Feb 2016 I have purchase HDFC Click2 Invest Plan for 5 Yrs and pay 4000 per month As per research and Customer reviews After Completion 5 Yrs Got around 13% to 17% Return.After One Year got only 7.5 %Return. But today realize I have Blocked money for 5 yrs and after 5 yrs not getting the good return.

please let me know what would best for me.

Well this is something you have to be answered first. WHY have you invested in this plan at first step. If this policy is answering your WHY then continue, else discontinue. My views are very clear …never mix investments with insurance.

Hi my age is 28. I Need approx 1 crore after 20 years. Also want to go on international holiday (current approx cost 2.5- 3 lakh for couple) with my wife after every 2 or 3 years. I can take maximum risk for my investment. How much should I invest per month for achieving my goals. Confused between MF and direct investment in BSE index stocks/or some other good stocks. I know you can’t predict actual returns of MF/Index Stocks. But guide me thought best way to invest for getting close to my goals

Please suggest

Hello Sir,

I am an IT professional 24 years old. Going through this article I felt no to go with ULIP plan ( am about take a plan today paying 2000 per month) . As I told I am from IT background I have zero knowledge about this market. After 10years from now, I need an amount of 4 to 5lakhs (not expecting very much too) from my savings. Can you please suggest me, the best pans.

I have gone through PPF, FDs RDs they are giving me 7 to 8% returns.

I had call with policy bazaar financial adviser and he is convincing me to invest in HDFC click2invest. He made me to visit below links.

http://www.moneycontrol.com/insurance/ulip/hdfc-standard-life-insurance-HD/hdfc-life-progrowth-plus-opportunities-fund-IHD391.html

http://www.moneycontrol.com/mutual-funds/nav/hdfc-high-interest-fund-dynamic-plan/MZU008

http://www.moneycontrol.com/mutual-funds/nav/sbi-dynamic-bond-fund/MSB048

going through above links he is convincing me to invest in hdfc click 2invest and using hsbc sip caluclator he is telling even in crisis the average returns will be 8%. I asked him a week time to tell my opinion. Now after going to this article am in dilemma, If I have to enter into this field or not else go with small savings scheme. We are not that rich too to handle the down fall. So kindly suggest me the best plans please.

I like your view on not to mix investments with insurance. I have some queries

1. is ULIP at least better than PPF if we ignore its mixure of insurance and investment plan. Since in case of HDFC click to invest they guarantee at least 8% return in case market goes down, And PPF is giving 7.9% from this financial year

2. Can you guide how to start with your own research on mutual funds invetsments.

Hi Manikaran,

I would like to invest in Mutual Funds. I am looking for best equity funds which give me good returns in one or two years. I see there are some funds displayed in money control website in top ranking which have given around 31% returns in one year and around 15% for two years (15% annually).

Examples:

Kotak Select Focus Fund – Regular Plan

Birla Sun Life Frontline Equity Fund – Direct

L&T Infrastructure Fund (G) ===> this gave 46%, very high in one year

Please suggest me if I am expecting returns one or two years or 3 years or 4 years macimum, can I go for MF or not

Hello Sir,

As I am planning for 20 years with good return, also want to cover up my investment under 80 C.

So I have considered few option-

1. HDFC Click to invest – ULIP

2. Axis LT Equity Fund(G) – ELSS

3. HDFC Young Star Plan

Could you please suggest where I should invest from the above list or apart from this list

Thanks,

Tarun

I would like you to have mix of ELSS/ pure term insurance and PPF. It’s better to have a detailed investment plan at place, then only you would be able to continue with the structure for 20 years, else would keep withdrawing now and then for your short term requirements. Though the lock in structure of ELSS and PPF would not allow you to.

Hi Manikaran,

I am 26 years old and my time frame for investment is 15 to 20 years but I will be withdrawing money on major occasions. I am focusing mostly on equities mutual funds Like SBI Bluechip and Kotak select focus fund.

Is it safe to investments major portions in equities? Since i have the age factor i consider that Risk can be taken.

Please provide your suggestions.

Monthly savings: 4000

I just started 2 months back and invested 2000 rs per Month for 5 years in click 2 invest , and I am not able to take a risk then please suggest this is a suitable plan for me or I have to drop out now…..

Hi sir,

I started the plan click2invest monthly rs.10000 paying term 5years.my age is 28 anf NRE.This plan better for me or any other good plan .one more i dont want to take risk.

Hi sir,

I started the plan click2invest monthly rs.10000 paying term 5years.my age is 28 anf NRE.This plan better for me or any other good plan .one more i dont want to take risk.

I have shared my apprehensions about investing in this plan in the article itself. Whether it is good for you or not…not sure. Please consult your personal financial planner.

Hi,

I was planning to take this plan with 20k monthly premium. One thing which is not clear is, while paying the premiums do i have to pay GST also? I am an NRI.

Thanks is advance

Hello,

I am planning to take this plan with 20k monthly premium for 5 years. Do i have to pay GST along with the premium every month? I am an NRI.

Thanks

Yes. But not over and above. GST will be the part of the Premium.

Do i have to pay more than 20k p.m.? if not, on what amount the interest be calculated on? if its 20k, then where the GST be applied?

Out of the premium, GST will be deducted, Mortality expenses and other policy related expenses will be deducted and the balance amount will be invested as per your choice of fund

Thanks for information.

Sir I want to invest around 10,000rupees per month for at least 10 -15 years, which would be the best mutual funds though I don’t want to take risk but at least return should be @>12% .

Plz Guide me

thank sir

12% is kind of return for which you cannot ignore the risk. So you have to be comfortable in that first.

Keeping in mind the LTGC, if someone is starting young have low mortality charges, could this be a lucrative option because of the lower tax liability?

Maybe. Not Sure. Mortality charges keep increasing with age

Hi, myself sanjay jeena my investment is 2k per month please suggest what would be better options for me, I got a call from paisabazaar.com for HDFC click 2 invest plan but I have read so many reviews and comments but its not positive.

Mr. Manikaran please suggest whether I would go to ULIP or SIP and if SIP then which one is the best with minimum risk.

Waiting for your reply.

SIP should work good, as it is a Flexible product.

Hi,

My banker has suggested to invest 5lac per annum for 5 years. He says it will be good to save LTCG tax as 25 lac should get good return in long run and when I withdraw all amount it will be tax free?

He is correct in saying that the maturity in this plan would be tax-free if only you continue paying the premium for the full term and your policy should have sum assured of 10 times of the annual premium.

But with this, you will bear the Mortality cost.

In the article, I have listed down the issues that I feel every ULIP policy have. MFs can be a better bet according to me even after the LTCG taxation

Can I surrender click 2 invest policy within first 15 days beacuse I invested in it and now I don’t like this ?

Yes, you can surrender the policy in first 15 days

Hi,

My banker has suggested to invest 5lac per annum for 5 years ( till the lock in period) in HDFC CLick to invest ULIP. He says it will be good to save LTCG tax as 25 lac should get good return in long run and when I withdraw all amount it will be tax free? , i have already invested in SIP, lumpsum MF’s and have some money in FD. He suggested to liquidate underperforming MF’s and to move to this ULIP ?.

I need few clarifications, 1. I had invested in ICICI Prudential dynamic plan – dividend in 2015 end ( it has got changed to ICICI Prudential Multi Asset plan ( i get my dividends till date), current value is in negative value. Banker suggests to redeem and move this to ULIP premium for 1st year saying with upcoming elections in 2019, the value would further go down and be like this till next 1 to 1.6years. Iam thinking i should stay invested for some more time and not redeeem now. Please advise.

2. Is it ok to liquidate my FD and move to ULIP premiums , is that a better option in terms of having a diversified portfolio ?. Not able to decide , i thought i will use this corpus to add it to my son college education fund. He suggested me to take it in my sons name as the mortality charges are less. He gave me a projections at 8% and 12% and seems ok.

Please advise.

If any happening in Equity market impact Equity Mutual fund, the same thing will impact ULIPs too. So saying that Elections will impact an only icici dynamic and not HDFC ULIP, that is wrong.

Moving FD to ULIP may not be a wise choice as both are different Products exposing to different Investment asset classes. and i am not sure why have you kept money in bank FDs?

rather than investing money haphazardly, you should better follow a well-designed Investment plan, where you will be advised with suitable investment products based on your risk profile and goals targeted. If not, then such kind of questions keep bothering you with time and you will not be able to make a concrete decision.

8%-12% Projection is fine, but what is the action Plan if that return does not come. How would you accept the change in market sentiments?

You have to look at your financial Life in totality, and not just from your child’s education point of view. You have limited resources which need to be deployed sensibly, expecting all the good and bad from markets.

Hi Sir ,

A few questions if you could help clarify

1. Will hdfc click2 invest help if I want to invest for a 10 year long goal ? Assuming I take the policy in the name of my kid(8yrs) so that mortality rate is low.

2.i read that this ulip allows me to move funds across different categories to arrest any fall due to market crash. Isn’t this any advantageous?

3. I am not looking at liquidity , and don’t want to pay the LTCG is there any other option. I already have ppf and don’t want to invest in FD.

4 insurance or tax savings is not a requirement but at the same time I have a low risk appetite.

Hello Sunny

Please find my Replies as below:

1. Yes, it will. It’s a ULIP product. But buying Insurance in the name of a child does not make sense to me. Of course, this will have lesser Mortality cost, but still, it is a cost. so you need to do some cost-benefit analysis before moving ahead.

2. It may help. If you are actually so active in making the changes and can predict the fall timely. Both I don’t think is humanly possible.

3. Not sure. Your financial Planner may guide you well on this.

4. ok.

Hi Sir,

The bankers and agents have sold me HDFC progrowth plus and HDFC click to invest without fully briefing me the charges. Can I surrender the policy within 30 days grace period without any charges.

Regards

Yes, you may ask for surrender within the required time frame. They may deduct some charges in the form of Stamp duty charges. Do check the policy wordings for complete details