SIP has become one of the popular ways of investing in equity Mutual funds. Investors have started accepting Mutual funds as a product to generate long-term wealth. SIP itself seems to have become a product in itself as nowadays people generally ask “Which SIP is good to Invest in?”, without realizing that SIPs are just a way of investing, and will help in averaging out the market volatility.

Let’s look at the numbers. In October 2024, the mutual fund industry witnessed its highest-ever monthly SIP inflows at ₹25,323 crore, alongside ₹59,362 crore in equity net sales. Gross sales stood at ₹1,02,983 crore, but the other side is that ₹43,621 crore (roughly 42% of equity investments) was redeemed within the same month. Given the heightened market volatility, the upcoming data for November might reveal even more about investor behavior.

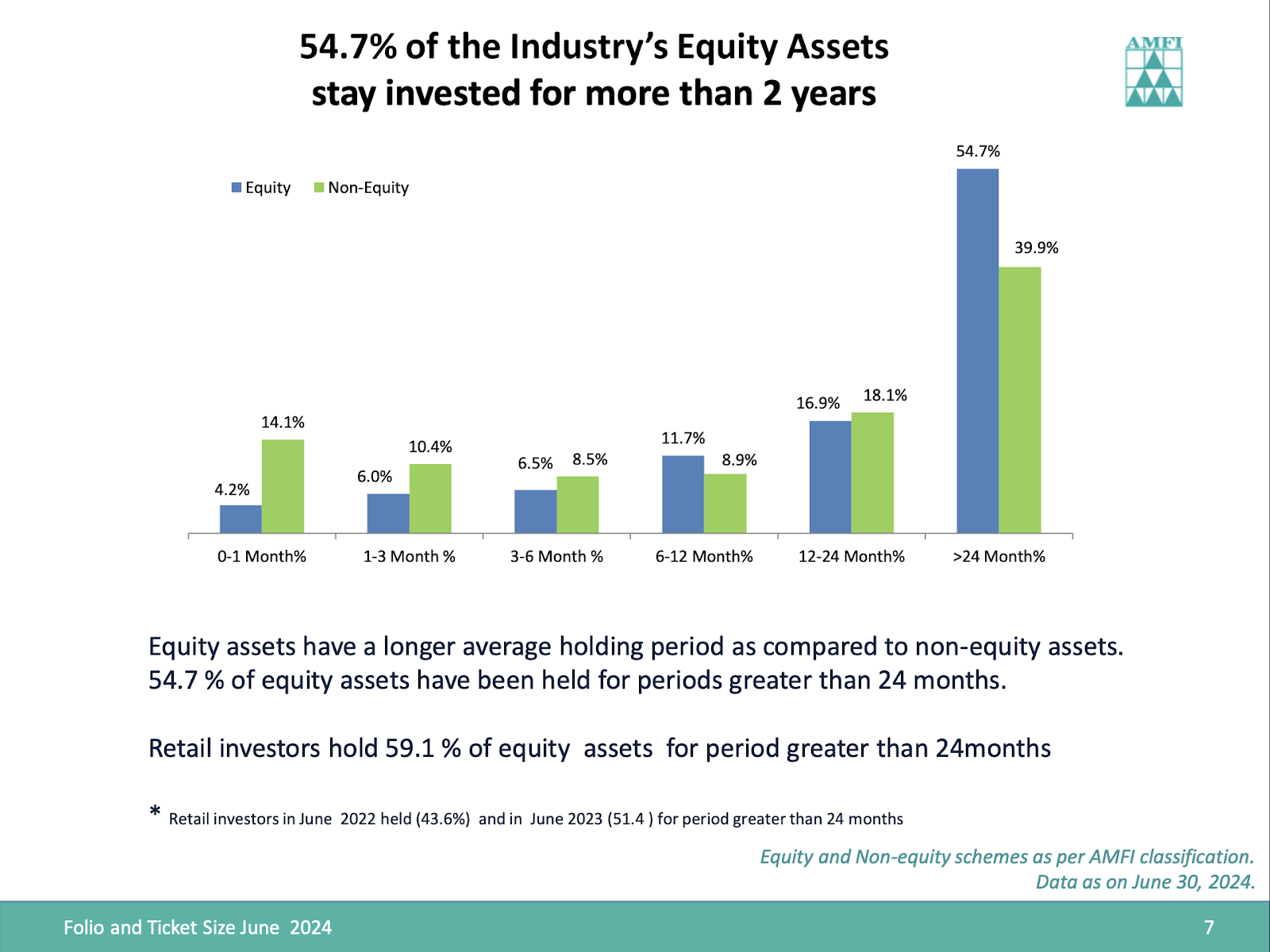

AMFI data from June 2024 paints a similar picture. Only 54.7% of equity investments stay invested for over two years, with this figure being slightly better (59.1%) for retail investors. This means over 40% of equity investments are redeemed within two years, despite equity being an asset class meant for the long term.

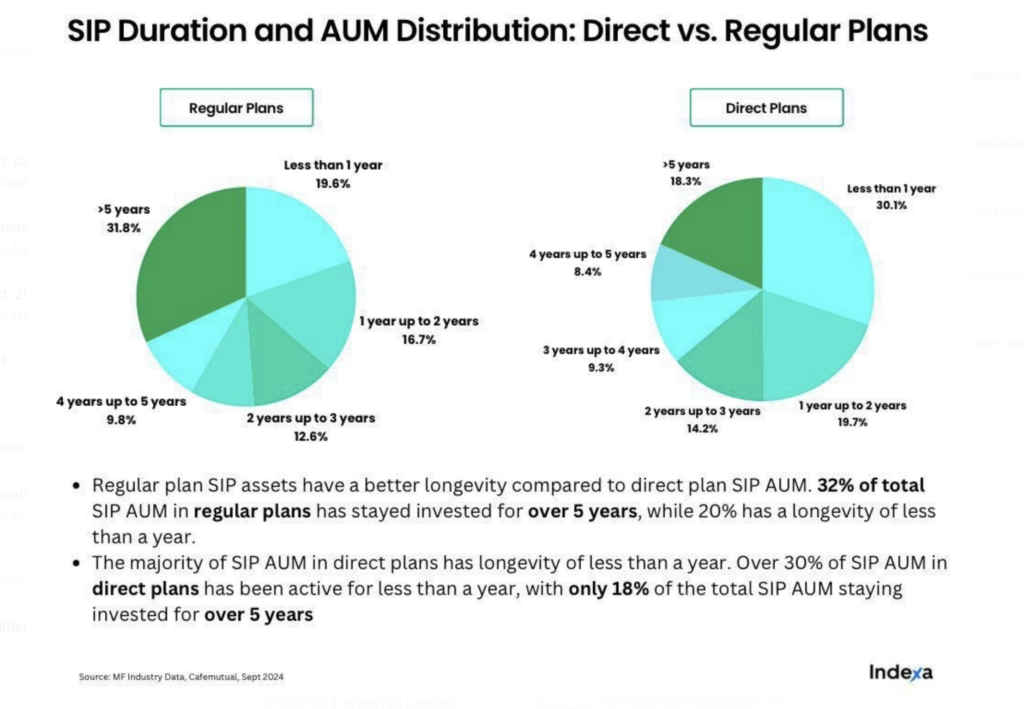

Further, one more data recently released, tells that the Majority of the SIPs get discontinued in the first 3 years.

All this raises a critical question:

Why do investors, who start SIPs with enthusiasm and a “long-term” mindset, struggle to stay invested for even 5-7 years—the minimum time frame required for equity investments?

While data highlights the problem, it doesn’t explain the reasons. However, from observation, the key culprits are mismanagement in other areas of personal finance and unrealistic expectations from investments.

Also check - Our Financial calculators for easy number crunching

Common Mistakes That Derail SIP

1. Unrealistic Expectations of Quick Returns

Many investors enter mutual funds with the lure of quick gains but soon shift to other avenues like stocks or derivatives (futures and options) in pursuit of faster returns. This frequent switching, driven by impatience and greed, disrupts the compounding process that SIPs rely on. Also read: Balancing Expectations and Reality

Fintech platforms add fuel to this behavior. They promote direct mutual fund investments, often for “free,” drawing investors in with past performance data and “successful strategies.” While direct investments may lower costs, these platforms profit by upselling other products and pushing investors toward impulsive decisions, ultimately undermining their discipline.

2. Redeeming Due to Market Falls

Many investors panic during market downturns, redeeming investments to avoid further losses. However, equity investments inherently demand participation in market volatility to reap the rewards of eventual growth. Without the courage to stay invested during dips, one cannot enjoy the highs that follow. Also read: Why do Average Investors earn below Average Returns

To truly build wealth, you need to avoid such distractions and work on other foundational areas of personal finance, discussed below.

Building a Strong Foundation for Long-Term Investing

1. Lack of an Emergency Fund

An emergency fund should be the first step in anyone’s financial plan. Life is unpredictable, and unexpected expenses can arise at times. Without readily available liquid money, investors are often forced to dip into their long-term investments like Equity SIPs to cover emergencies. This disrupts their financial journey and impacts their long-term goals.

2. Inadequate Insurance Coverage

Having adequate insurance, both for yourself and your dependents, is critical. You should not rely solely on employer-provided insurance, which can leave you vulnerable, as such policies often have limitations, like sub-limits or caps on specific surgeries, and also will not cover you when you are not in a job, or during times of transition from old to new job. When faced with unexpected medical expenses, investors without sufficient coverage often tend to redeem their SIPs, defeating the whole purpose of long-term investing.

Also read: The Only 3 Reasons, you need a Financial Planner

3. No Goal-Oriented Savings

Investing without clear goals often leads to withdrawing funds for any and every need. To avoid this, divide your savings into three buckets:

- Short-term goals: For annual expenses like insurance premiums, vacations, or small gadgets.

- Medium-term goals: For bigger purchases, like a car or maybe a high-end gadget.

- Long-term goals: children’s education, retirement or house purchase and other future needs.

Without having dedicated short- and medium-term savings, you’ll likely tap into your long-term investments, or worse, take on EMIs, which only strain your financial health further. Also read: Why your Retirement Plan may fail?

4. Unchecked Borrowing

Borrowing for consumption—be it a phone, vacation, or gadget—is a habit that can seriously derail your financial discipline. Such loans create a disconnect with your cash flows, leading to tighter budgets. And when finances get squeezed, SIPs often become the first casualty, since EMIs are non-negotiable.

The Bottom Line

SIPs need discipline then only can be called as powerful tool for wealth creation. Wrong expectations for Quick gains, or poor financial planning, will not yield good results. You need to maintain the financial hygiene in your profile by building an emergency fund, ensuring adequate insurance, saving with goals in mind, and avoiding unnecessary borrowing, to stay on track and give your investments the time they need to grow.

Remember, wealth creation is not an overnight thing. You need to keep yourself safe from distractions that may blur your long-term vision.

To understand this better – read this article

Hope you liked the thoughts. Do share your views in the comments section below.

{kind=link}