New pension scheme, National pension scheme, National pension system, or whatever name you call it with is all the same. This article is to share with you the nps details of the product.

New pension scheme is a defined contribution scheme started by the Government of India for the central government employees excepting the Armed Forces with effect from 01 January ‘2004; gradually state governments also adopted this system.

Defined contribution means that unlike the old pension system, here the employee and employer (government) will make a defined contribution/deposit in the scheme (which is 10% of basic+DA), and at the time of retirement, the pension/annuity can be purchased with the accumulated corpus in this account.

With Effect from 1st May ‘2009, NPS is available to all citizens of India who can contribute on a voluntary basis.

NPS is a good product and slowly gaining popularity. The Indian Government is leaving no stone unturned to promote NPS.

Also read: Also Check- National Pension Scheme (NPS) for NRIs- a detailed guide

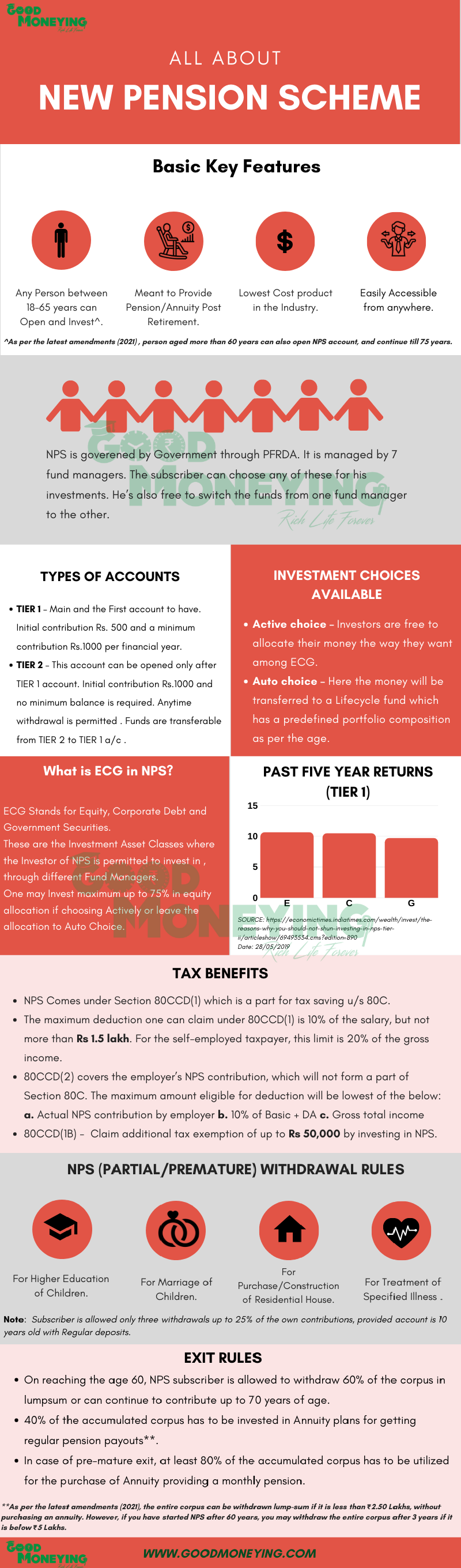

NPS details – Basic Features of new pension scheme

- NPS is regulated by PFRDA. As SEBI is for Stock markets and Corporates, RBI is for banking, IRDA is for Insurance companies…the same way PFRDA (Pension Funds Regulatory and Development Authority) is for NPS. So don’t confuse this with another insurance company’s product.

- It is Open to All citizens of India in the age bracket of 18 – 60 years. As per the latest amendments in NPS rules (2021), a Person aged above 60 years can also open an NPS account and continue till 75 years of age.

- The minimum contribution required is Rs 1000/- annually, with no limit on the number of transactions (there are charges per Transaction).

- The initial and minimum amount per contribution is Rs 500/-.

- As this is strictly a pension product, so subscriber compulsorily has to Purchase life annuity with some specified restrictions/flexibility.

- It is a very lost cost product. With a fund management charge of just 0.0009%, this product is perhaps the world’s lowest-cost pension scheme.

- Investment can be made in different Asset classes through 7 fund managers.

Working mechanism of new pension Scheme

It is very simple. It requires regular yearly/monthly/quarterly contribution from the subscriber and on maturity subscriber has to transfer the specified minimum corpus to any IRDA regulated Life insurance company to Purchase Life Annuity and the balance can be withdrawn in Lump sum.

Also read: Read – The new rules announced on NPS withdrawals 2021.

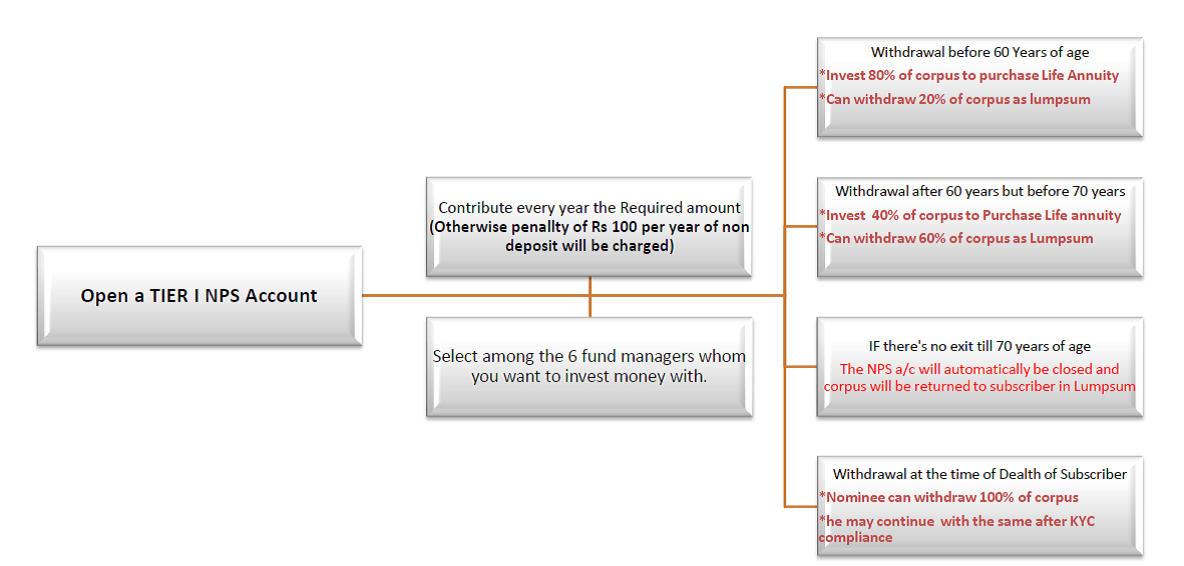

NPS details – Types of Accounts in New Pension Scheme

TIER 1 – This is the First account that subscriber has to opt for. Withdrawal in this account is permitted as per the above chart.

TIER 2 – This account can be opened only after the TIER 1 account. Anytime withdrawal is permitted through this account. You may also transfer the funds from TIER 2 a/c to TIER 1 but not the other way round.

NPS details – Investment style and Asset Allocation in New pension scheme

Pension Portfolio Fund Managers

Right now there are 7 fund managers appointed under “All Citizens account” category. The subscriber can choose any of these for his investments. He’s also free to switch the funds from one fund manager to another without any extra charge.

- Birla Sun Life Pension Scheme

- HDFC Pension Fund

- ICICI Prudential Pension Fund

- Kotak Pension Fund

- LIC Pension Fund

- SBI Pension Fund

- UTI Retirement Solutions

The fund managers may keep changing or stay the same as per the new criteria and costs structure laid down by the government from time to time.

What is ECG in NPS?

Every portfolio fund manager has to manage the money in 3 separate accounts having separate asset profile. Here E stands for Equity, C stands for Corporate Bonds and G stands for Government securities.

Asset Allocation

There are 2 choices available for subscribers.

Active choice – In Active Choice, the investor can choose his asset mix among four asset classes as per his choice – Equities (E), Corporate debt (C), Government securities (G). With the recent changes, the maximum permitted allocation to E has now been enhanced to 75% up to 50 years of age. From 51 years onwards, the maximum equity allocation allowed will keep reducing by 2.5% per annum, and become a maximum 50% at the age of 60. Prior to this change, the exposure to E was capped at 50% of the portfolio.

Auto choice – Here, the money will be invested in asset classes – E, C, and G – in defined proportions based on your age. As an individual’s age increases, exposure to Equity and Corporate Debt are gradually reduced, and that in Government Securities is increased. Depending upon the risk appetite of the subscriber, there are three different options available within Auto Choice-Aggressive, Moderate and Conservative.

- Aggressive (LC-75) – Maximum Equity exposure is 75% up to the age of 35.

- Moderate (LC-50) – Maximum Equity exposure is 50% up to the age of 35.

- Conservative (LC – 25) – Maximum Equity exposure is 25% up to the age of 35.

Also read: Read More – NPS Investment choices – which is a better option?

NPS details – Taxation aspects in New Pension Scheme

Taxation aspect is very interesting to understand and if used properly it will help in a decent reduction in tax payment.

This is covered under Section 80CCD of the income tax act, which says

Deduction in respect of contribution made by the individual in the previous year to his account under a notified pension scheme is allowed in the computation of his total income –

a) In the case of employee 10% of his salary in the previous year.

b) In any other case 10% of his Gross Total Income in the Previous Year.

It is further clarified that the aggregate limit of deduction under this section along with Section 80C, 80CCC shall not, in any case, exceed Rs 1.5 lakh.

Where the central government or any other employer makes any contribution to the account of employee for the pension scheme, the assessee shall also be allowed a deduction in the computation of his total income of the whole of the amount contributed by the central government or any other employer, provided it does not increase 10% of his salary (Basic +DA).

Any contribution made by subscriber in NPS a/c in a financial year will be eligible for tax benefits up to Rs 1.5 lakh u/s 80CCD, subject to overall Limit of Section 80C.

Further, as per Section 80CCD (2) of income tax act says W.E.F 1st Apr 2012 up to 10% of the salary (basic and dearness allowance) of employers Contribution can be deducted as ‘Business Expense’ from their Profit & Loss Account.

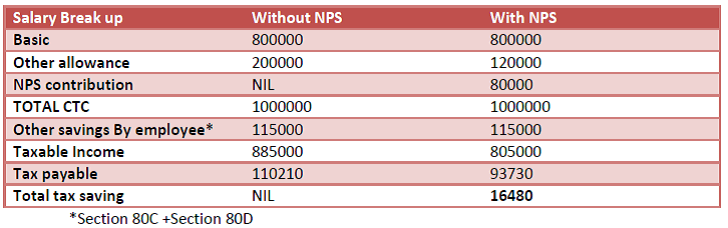

Thus from now onwards if you can negotiate with your employer on salary break up or increment at the time of appraisal, you may include NPS contribution by the employer in your total CTC. This will help you in a significant reduction in tax payment. You can make use of this change from your Retirement planning purpose.

W.e.f April 2015, there’s new section added in IT act 80CCD(1b). Now you can save tax over and above section 80C limit, by investing maximum of Rs 50,000 in New pension scheme account. (Check a detailed article on Income Tax Deductions)

Pros and Cons of New Pension Scheme

Pros

- Low-cost structure has definitely made it a product to consider.

- Additional Tax saving u/s 80CCD (2) on employer’s contribution is another attractive option.

- Flexibility on part of investors on asset selection and choice of 7 fund managers with good track record.

- This account is completely portable. Unlike other products like PPF/EPF where you have to get the account transferred the time you change your job to some other place, this account is accessible everywhere in the country with the same account number.

- Now it is also possible to start SIP in NPS. Click here to know how to set up SIP in NPS online using the D-Remit Facility.

Cons

- Taxation on withdrawal at maturity is the biggest disadvantage in choosing this product. However, as per budget 2016, FM has allowed 40% of withdrawal on maturity as tax-free. In Budget 2019, the whole withdrawal of 60% is declared tax-free. ( Read: NPS withdrawal rules)

- Data on the performance of fund managers and respective schemes is not readily available. However, there are some media houses that track the performances and share every week in their publications. But now you can go to the NPS Trust website to view the scheme performances.

- Restriction on Equity Investment to 50% may be unacceptable to some. Though in Auto Investment choice, a new provision has come up where subscriber can have aggressive allocation and get 75% of equity exposure up to 35 years of age

- Not so flexible in pre-closure or prematurity withdrawal.

Also read: Also Check- How much pension can you get from NPS Annuity Plans

Should you invest in New Pension Scheme?

Now you have gone through all the NPS details. You can see that the low-cost structure and now the tax exemption on the employer’s contribution have made this product a very attractive one. Otherwise, all other features can be brought in the portfolio through other products with proper investment planning.

Tax at maturity used to be a big drawback in this, but in budget 2019, the whole 60% lump-sum withdrawal was declared tax-free by the Govt and the extra tax benefit u/s 80CCD(2) makes it a must-buy option. I feel that if one is a disciplined investor and has done proper Retirement planning then he may include some portion of his investments into this. ( Read more: NPS details – All you wanted to know about New Pension Scheme )

– Infographics")

{kind=link}

Good article.

Thumbs down to the NPS because of 50% cap, non flexibility and taxation at maturity..Big NO for any investor.

[…] W.E.F from 1st may’2009; New pension scheme is open for everyone to invest. It is a defined contribution scheme primarily started for government employees but later extended towards everyone. This is another long term Investment option where one may invest for his Retirement goal and takes exposure to equity and debt asset classes. The cost advantage i.e. the lowest fund management charge (@0.0009%) and the recently introduced feature where employee gets tax benefit if he invest through his employer (U/s 80 ccd (2))are the major attractions in this making it among best investment options in India. You may maintain the liquidity in your investments using Type 2 accounts. Though no flexibility in using the accumulated corpus and taxability at maturity is a concern, but some of the taxation is getting taken care by provisions u/s 80ccd (2) and the balance will be taken care by Direct tax code which if implemented as it is than it may make the maturity of NPS tax free. Ask any certified financial planner and he will tell you why you must take NPS as one of your personal financial planning options. (Read : All about NPS) […]

[…] 1.) Negotiate with your employer on the changes in the breakup of your salary structure. There are many companies which ask the employees in April to design the salary structure themselves suitable to their individual financial profile. They call it as Flexible benefit plan. Make the most this opportunity. Sit with you planner, CA or any other Tax professional and find out what amount of HRA benefit is suitable to you, what should be the different allowances that can be added in to this break up. You may also ask your Employer to start contributing into New pensions Scheme on your behalf to reduce your in hand salary and thus helps in tax saving. (Read : All about New Pension scheme) […]

very informative post.

It is actually a very good Retirement Plan for those who wish to get some pension even if their employer is not providing. Investors having investment in share market may find it non-attractive as they expect more returns and more flexibility in premature withdrawals.

Shaju, it is indeed a good option for retirement planning. Looking at the changes in the pension market and other costly products this product will definitely earn good word in coming days. And also by investing in NPS one can satisfy his desire to have decent equity exposure and that too at less cost.

I transfer 1000/- from my “State Bank fund transfer service” under “NPS Contribution” on 4th Apr 2013 to my “NPS account” but NPS account not showing effective till today (7th Apr 2013). Any idea how much time does it take? SBI customer care says to talk to your SBI branch whether I live far from my branch. Any idea?

I think is should take the normal time that any NEFT or fund transfer takes. You better get in touch with your bank branch.

it does take a week generally. I transfer from SBI all the time and there are no issues. Check it after 10 – 15 working days. You can check your PRAN account online at the CRA-NSDL website.

That’s strange ramana. I mean a week is a very long time for this kind of transaction. And just for information and readers’ knowledge sake, what NAV gets alloted to the investor, the day of transfer or day of reciept?

It takes up to 20 days sometimes even. And the NAV is always of the day of receipt by the NPS. And by some strange co-incidence, that NAV is always HIGHER than the NAV of the date of transfer. Someone should investigate this…

I don’t recommended anyone to invest their valuable money in NPS. Their process is pure sarkari. My 13,000/- are still stuck in the scheme. Govt officials are not a bit cooperative. That was my mistake that I could not made payment on time and my account got freezed. After that I tried two times to un-freeze it but they did not cooperate.

I live in Delhi but my account was opened at my native Hardoi (A city near lucknow in UP). I put 12,000/- at the time of opening but next year due to cash-crunch I could not deposited on time. When I visited that branch during Diwali 2013, no one was able to cooperate there. All I was looking like “Musaddilal of Office Office”, from one desk to other, other desk to other. Customercare told me to fill Form “NPS-UOS-S10A-Tier-I” from their website and submit it with amount to POPSP at the office. I was surprised to know that no one was even know what is “POPSP”. All they had to say that Scheme was started by a Post Master on a huge level. Many people’s money is also stuck in the scheme. Delhi office does not cooperate with them bla bla bla.

And now I think their customer care is also abandoned. No one picks the call. I tried few months before near 14-15 times. Finally it was picked by a man who was not talking like a customer care representative like before. He only told me how much I have to pay to unfreeze the account, nothing else. I visited this Holi also, but their behaviour was same. No one still know process to unfreeze it.

If anyone of you know how can I get my money back must share here. Also if I can get it back from their New Delhi headquarter, that would be great. Me, my borther, my few friends all are looking for a solution 🙁

Vaibhav pls lodge your grievviance at pfrda.org.in site and follow up it through pfrda diretly.

Is NPS contribution cover under section 80C? As government has increased the 80C limit in recent budget, I want to know which avenues can I invest in under 80C. Thanks for your help.

Yes NPS contribution is a part of Section 80C investments. You can also deposit in ELSS Mutual funds, PPF, 5 year bank Fixed deposit. pay life insurance premium etc. to take section 80C tax benefit. Your home loan principal repayment and also children tuition fees also comes under this section

Hi, I am 35 Yrs. Wanted to know if it makes sense to put 60k in NPS? A lot of banks were suggesting not to put in NPS and that last 3 years returns on all 7 funds are negative. Pl suggest. I am not looking for investment, just savings.

See when you are a long term investor you should not look at short term performance. NPS is the most cost efficient investment. If one takes the tax benefit from this investment then the effective return further improves. This is also true that pension is taxable at the end, but post retirement you in any way should park some amount for regular income, just assume that you have already started doing that.

Invest only that amount from which you can derive some tax benefit, like Rs 50k u/s 80ccd(1b).

can u pl explain in detail tax benefit example including employer (if any) and employee and section wise with and without NPS

Thanks in advance

NPS arrangement from employer is the same like EPF arrangement. If employer deducts NPS contribution from your salary then it will be counted under section 80C as a part of 80ccd, if employer deposits his own share into your account it comes under section 80ccd(2). Besides this now employee can make contribute more in NPS upto Rs 50000 which will give tax benefit u/s 80ccd(1b).

If you go through my article in detail, i have shared the example too.

WHAT DOES UOS MEANS

Its POS – Point of Sales

Sir, I am regular central Govt. Employee since 20 years and has old pension scheme. Can I invest in NPS !

Under what category is choosed for this scheme to invest my money. Can I opt benefit of contribution to me from my employer.

How can avail income tax benefit for this year to my employer ie India Post.?

You can have NPS account at a personal level. Your employer will not contribute to this. You can avail section 80CCD benefit by investing Rs 50 k in your personal NPS account.

I AM 62 YERAS OLD. CAN I OPEN AN ACCOUNT IN NPS???

Yes, you can. One may enter NPS till 65 years of age. Please do speak with your financial planner before going for it.

Sir i opened my personal nps account online, as I am a state government employee can i shift this nps account to state government please explain

We are not sure. You can visit the nps website to enquire about the same.

https://www.npscra.nsdl.co.in

Sir,I joined in central government service in 2004.NPS deduction started from 2004 itself.but no data getting from 2004 to 2008.how can I get that data about NPS amount.

you have contact the NPS helpdesk. They may help you on the same. Check with the Accounts Department, see if they may help you.

I opened nps for my spouse and she is homemaker so can I claim tax exemption on it?

You may not be able to claim extra tax exemption for the same.

Employee’scontribution to NPS @ 10% and employer’s contribution @ 14% of basic and DA.

Pls brief about the tax provisions

The contribution to NPS made by you only would be considered as an income tax deduction, not the employer’s contribution.

Is there any benefit on continuing NPS after attaining the age of 60 years (upto 70 is allowed)? Are the contributions tax free after 60?

It is up to your requirements. If you need the funds then you may withdraw. Else, there is no harm in continuing. If you stay invested, the money would get compounded for 10 more years.

Here the bigger question is that if I do not close my NPS account at 60 years of age and continue it with minimum contributions till 70 years of age, then, at 70 years, when I withdraw the balance available in my NPS account, will the 100% be tax exempt or again 60% will be tax free and balance 40% compulsory annuity.

No sir, the rules of taxation would remain the same even if you continue your NPS Account till 70 years.

save money in NPS or mutual fund

It depends upon your requirements, goals, and other investments you have. In short, an overall analysis of your financial profile is required, then only we may advise which product would suit you.

i am 35 years old, what option should i select for NPS,

Auto or Active

Dear Harshal,

If you are an aggressive investor, you may go for the active choice with a higher allocation to equity, say around 60-70% and if you are a conservative one, you may lower the equity allocation, which would reduce the risk as well.

If you do not know your risk appetite and do not have any financial planner by your side then, it would be better to go with the auto option in which the equity allocation gets decreased according to age.

If I change the ECG scheme in between, whether my full accumulated amount till date will be transferred to next scheme or only further investment will come under changed scheme?

Hi Abhishek,

If you change the asset allocation of ECG of the NPS scheme, the new investment, and the existing portfolio both would get invested as per the new asset allocation.