Finance is not just a man’s world, and it never should be.

Many women tend to distance themselves from financial matters, often believing it’s their husband’s responsibility. After all, they’re already juggling multiple roles—managing the home, raising children, and balancing work-life commitments. Shouldn’t finances be the least their husband can handle? That’s what many think.

But here’s the truth: A financially aware woman makes for a stronger family, a more secure future, and better financial decisions—both for herself and her loved ones.

When women actively participate in financial planning, they bring fresh perspectives, reduce overconfidence biases, and help prevent financial missteps. Plus, what happens if the husband is not around due to unforeseen circumstances? Wouldn’t it be wise to be prepared rather than depend on others?

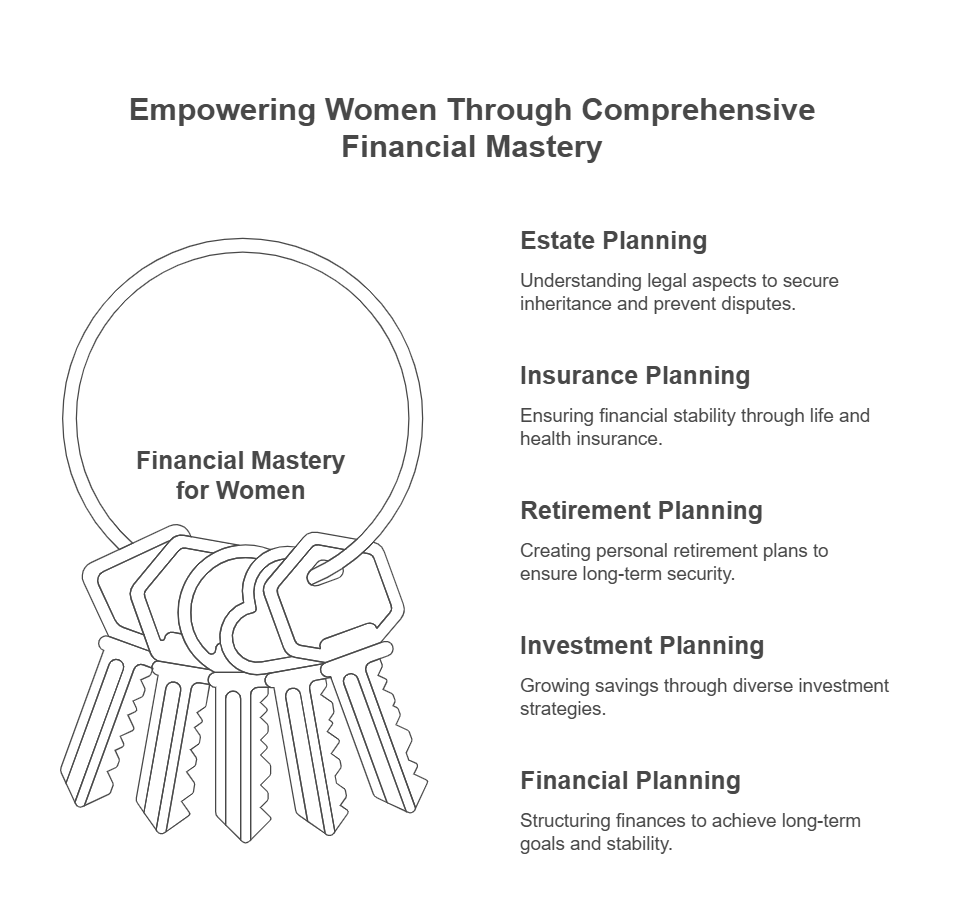

5 Financial Skills Every Woman Must Know -Let’s talk about that:

1. Legal Aspects of Estate Planning

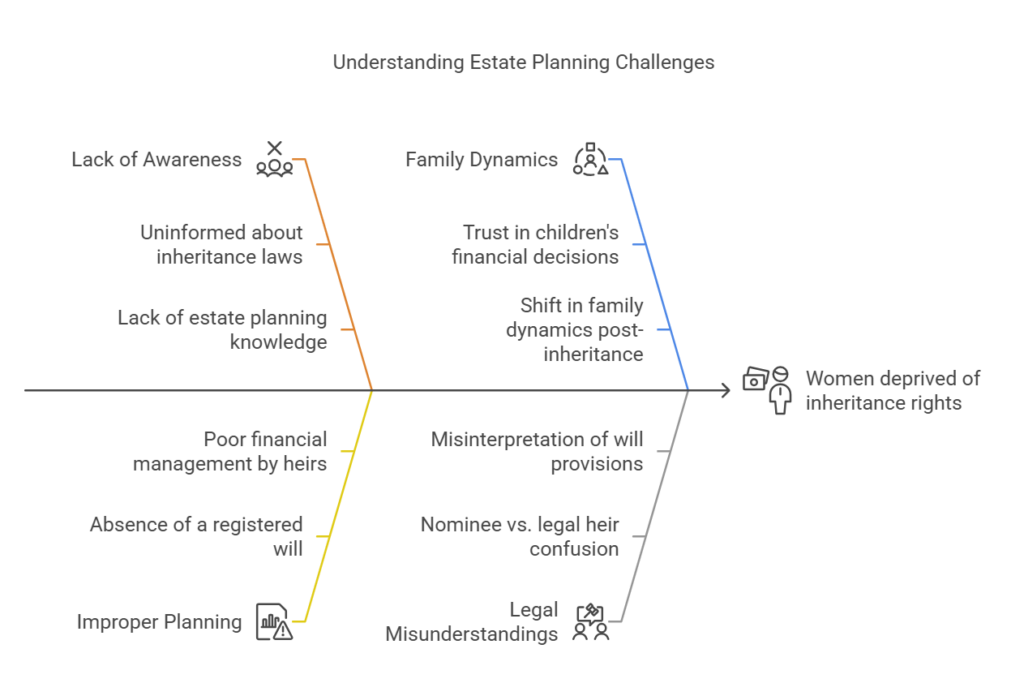

Understanding estate planning is crucial, especially concerning inheritance rights. Many women have been deprived of their rightful inheritance due to a lack of awareness or proper planning.

Legally, after a man’s passing, his assets are distributed among his wife, children, and mother unless a properly drafted will states otherwise. This applies to all assets, regardless of any nominations made.

Even when a will exists, some women, out of trust, allow their children to handle finances entirely. While the children may initially provide care and support, this dynamic can shift once they receive their anticipated inheritance, potentially leaving the mother financially vulnerable.

Why is it important?

- A nominee is not necessarily the legal heir. Understanding inheritance laws is crucial.

- A properly drafted will prevents family disputes and ensures financial security.

- If your husband owns assets, do you know how they will be transferred in case of an unfortunate event?

What should you do?

- Ensure there’s a clear estate plan in place, including a registered will.

- Learn about the legal rights of women in inheritance, joint ownership, and taxation aspects of estate planning.

- Discuss these matters openly with your family. (Read : Estate Planning for NRIs – Should NRIs Write Two Wills?)

2. Insurance Planning (Including the Married Women’s Property Act – MWPA)

Life insurance often forms a significant portion of total assets, yet many families either neglect it or fail to renew policies on time. The financial burden of an untimely event can be overwhelming, and life insurance ensures your family’s financial stability.

Married Women’s Property Act (MWPA) is a provision that ensures life insurance proceeds go ONLY to the wife and children, protecting them from creditors or legal claims. This is particularly crucial if your husband or even you run a business with liabilities.

Equally important are health and disability insurance. Many couples rely on employer-provided policies, only to realize later that coverage is inadequate. I have seen cases where, after a husband’s untimely demise, the wife struggles to get new coverage due to her health conditions—something that could have been avoided with timely action. ( Here check out – Need Based Insurance Calculator)

Why is it important?

- MWPA protects life insurance proceeds from creditors or legal claims.

- Many women don’t have their own health or life insurance, leaving them vulnerable.

- Many households are underinsured, meaning if something happens to the primary earner, the family may struggle financially.

What should you do?

- Get a life insurance policy under MWPA for added security.

- Ensure you have adequate health insurance—even if you’re a homemaker.

- Re-evaluate existing policies with your spouse to see if they truly cover your family’s needs. (Read :Free Health Insurance for Senior Citizens by Government of India)

3. Retirement Planning – Because No One Else Will Do It for You

Women tend to live longer than men, meaning more years to fund in retirement. Yet, many women don’t have personal retirement plans.

Men often chase the “best” investments, seeking quick returns, but wealth generation requires discipline and process. Every family member should understand their financial standing and ensure there’s a structured retirement plan in place. Women should know how investments will be managed or withdrawn in unforeseen situations.

Why is it important?

- Relying solely on your husband’s retirement savings may not be enough.

- Inflation will make future expenses higher than today.

- Career breaks often lead to lower savings—this needs to be compensated for.

What should you do?

- Start investing in growth-oriented products like mutual funds, NPS, and PPF.

- Calculate how much you’ll need post-retirement and start saving accordingly.

- Ensure you are part of all retirement planning discussions. And (Read: 20 Hidden Risks to Your Retirement Plan)

4. Investment Planning – Don’t Just Save, Grow Your Money

Most women are excellent savers but hesitate to invest. Keeping money idle in a bank account isn’t enough—it must grow to beat inflation. You have your own goals and desires beyond family responsibilities, and investing wisely ensures you achieve them.

Understanding different investment products and their risk-return profile is essential. Women, by nature, are cautious and nurturing, making them better at taking calculated risks—unlike men, who often chase high returns impulsively.

Why is it important?

- Investing can help you achieve financial independence.

- Savings alone will not secure your financial future.

- Many women rely on FDs or gold, but better options exist.

What should you do?

- Learn about mutual funds, SIPs, stocks, bonds, and other investment avenues.

- Diversify between equity and debt based on your goals and risk tolerance.

- Track your investments regularly rather than leaving them unattended. ( Read: Your Investments Reflect Your Life: Learn from Mistakes and Rebuild Smarter )

5. Comprehensive Financial Planning – See the Bigger Picture

Financial planning is not just about saving or investing—it’s about structuring your entire financial life smartly. From budgeting and cash flow analysis to estate planning and goal-based investing, every financial decision impacts your long- and short-term security. In your family life directly or indirectly you will encounter many financial issues connected to savings, investments, loans, estate planning, goal based management, big assets purchase like house or car, travel planning etc. every financial decision involves budgeting, cash flow analysis, and wise decision making keeping your long and short term goals in mind.

By actively participating in your family’s financial decisions, you contribute significantly to overall financial well-being.

Why is it important?

- A well-planned financial strategy ensures stability, liquidity, and security.

- It helps allocate money for different goals—children’s education, home purchase, vacations, retirement, etc.

- It minimizes debt and optimizes tax savings.

What should you do?

- Set clear financial goals with your spouse and create a roadmap.

- Maintain joint accounts, joint ownership of assets, and shared responsibility in financial decisions.

- Keep a check on household expenses and create a budget to avoid financial stress.( Read: Know Your Advisor- A Crucial Step for Your Financial Health )

Final Thoughts – Your Money, Your Responsibility

A woman’s financial empowerment doesn’t mean she has to manage everything alone. It simply means she knows how to manage finances, asks the right questions, and makes informed decisions.

By taking control of these five key areas, you ensure a secure financial future, not just for yourself but for your family. Because financial planning isn’t just a man’s job—it’s a family’s responsibility.

So, are you ready to take charge? check out- Women’s Day and Financial Planning: A Reality Check for Women

{kind=link}