Momentum Investing, as the name suggests, is all about capturing momentum. This means investing in stocks that have performed well in the past and are thus expected to continue growing even further.

This is how many (new and novice) investors participate in the stock market. They look at the recent performance and feel that this will continue for a long time and make them millionaires in a short period. They come from feeling and not a structure.

But when the Mutual funds follow this Momentum investing strategy, they have a defined methodology and keep rebalancing their portfolios every 6 months. They just don’t look at the price returns only but the volatility of those stocks too, with no Human bias involved. This means that what has not been performed will not be kept for long, come what the fundamentals say.

Where an Individual investor under the lure of high and faster return may overbuy a single stock and take high concentration risk which if backfires impacts their financial position very badly, the structure and regulatory provisions in Mutual funds don’t let them go overboard on a single stock, thus maintaining the basic nature of diversification.

Of course, the opposite is also true, as the concentration may pay off well, but in that case, your investment should be backed by high-conviction research, which is not everyone’s cup of tea.

Momentum Investing does not consider Market capitalization, Fundamentals, or Valuations, but only the last 6 and 12 months’ price returns adjusted to volatility, and this also may lead to high churning in the portfolio, which again if done at the Individual level leads to heavy taxation.

Now the question comes, how risky is this strategy and whether this is suitable to keep in the long-term portfolio of the investor.

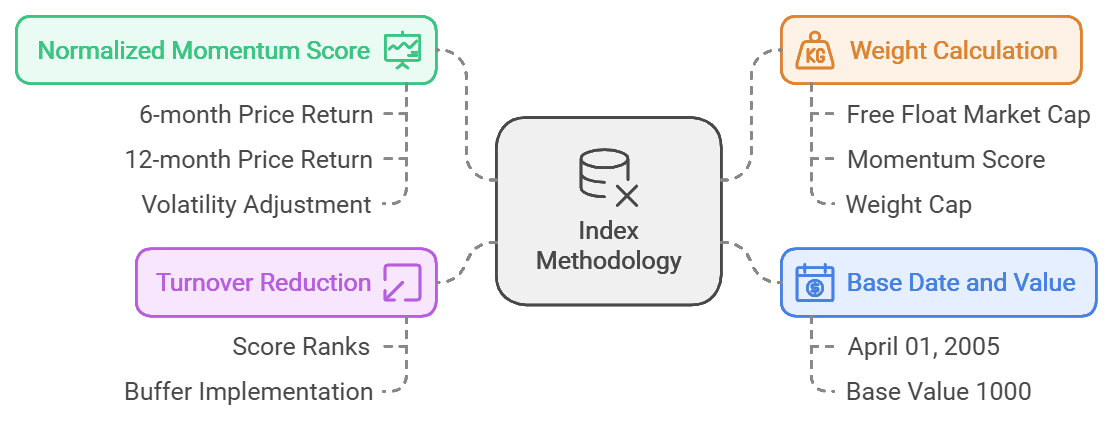

Momentum Investing in Mutual Funds

There are many Momentum funds in the market these days, which follow different Indexes. We have Momentum Schemes in the Large and Midcap Index (Nifty 200), In the Midcap 150, in the Small-cap 250, and even in the Nifty 500. All these follow the same stock selection and rebalancing strategies. To understand this in detail, let me pick one fund for you and look at it from a risk and returns perspective vis Vis the indexes and their Active counterparts.

In this article, we will focus on the Nifty 200 Momentum 30 Index and its respective schemes.

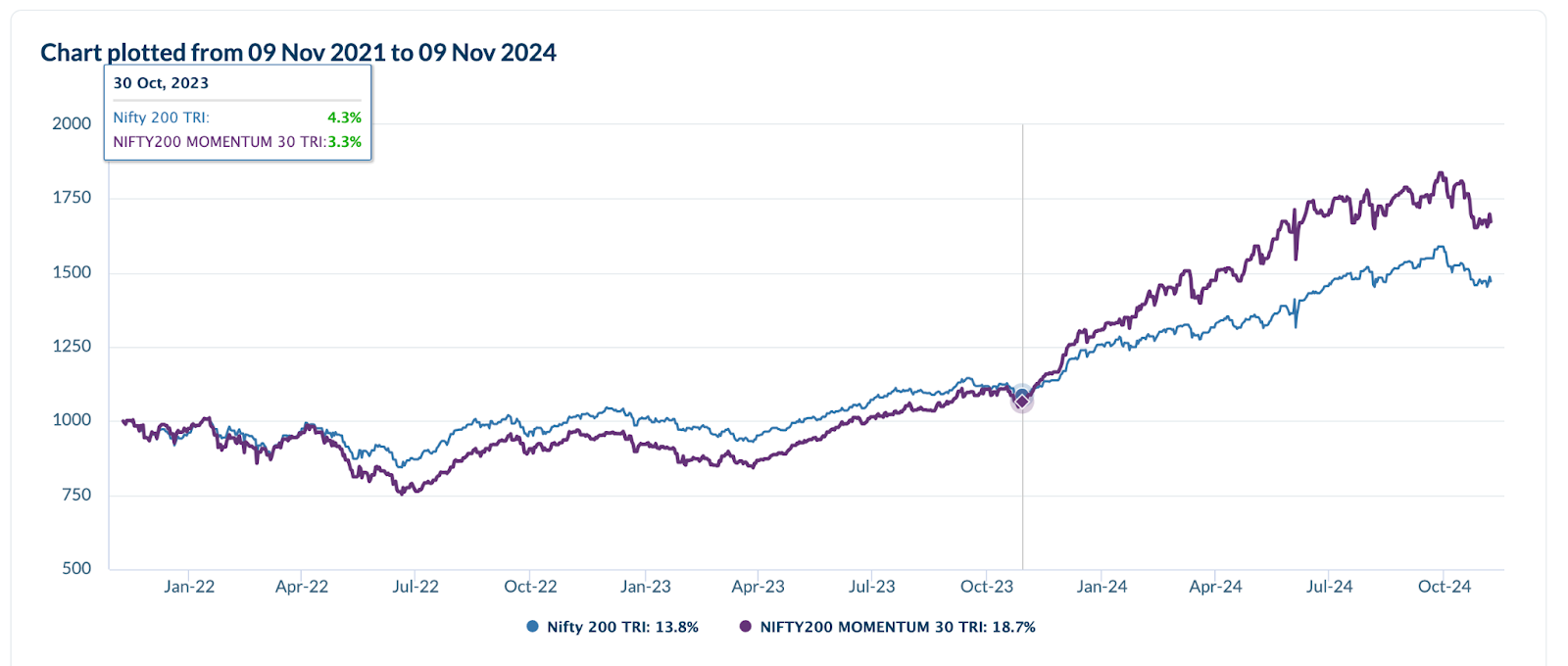

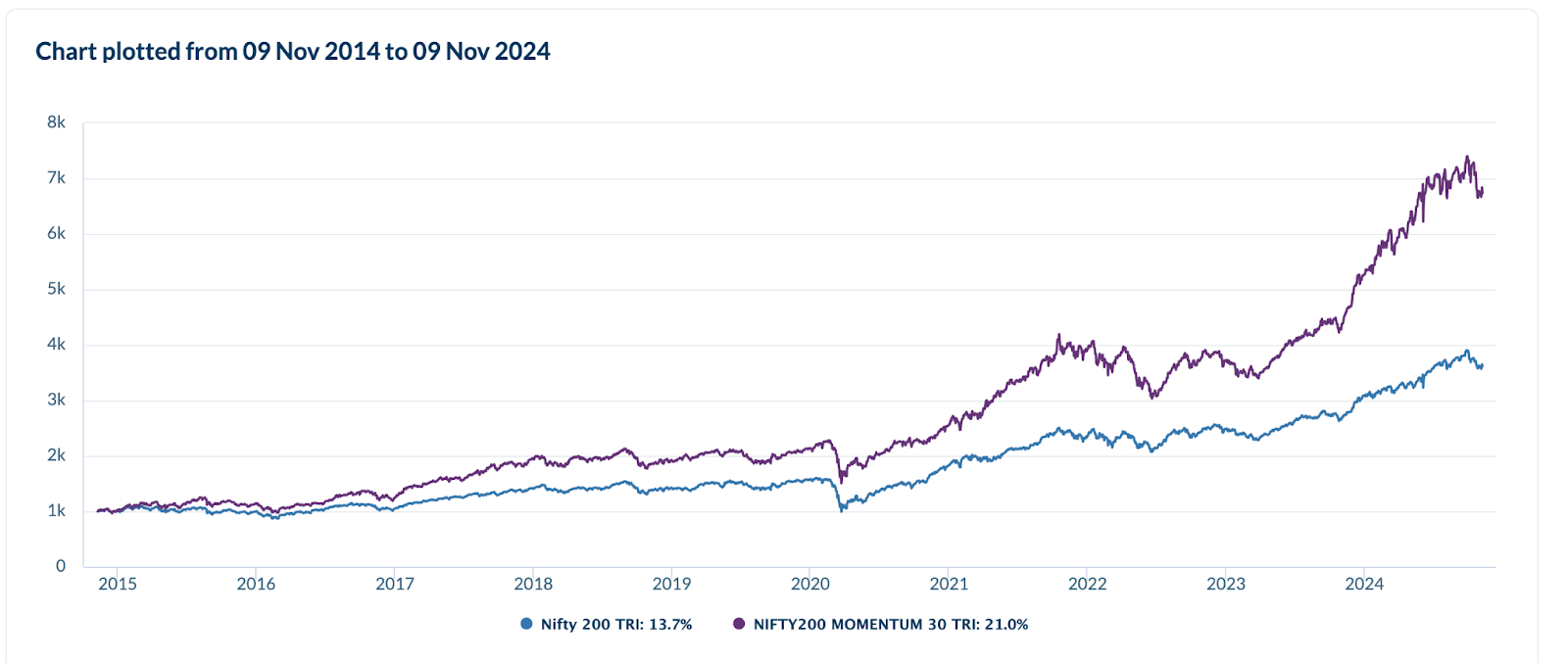

Nifty 200 Vs Nifty 200 Momentum 30

3 years Returns ( Point to Point)

This is Visible that though the Momentum strategy has delivered quite high returns as compared to the Broad index, before 30 Oct 2023 it was underperforming.

However, If you look at 10 years point to point returns, the chart shows that Momentum Investing has paid a lot

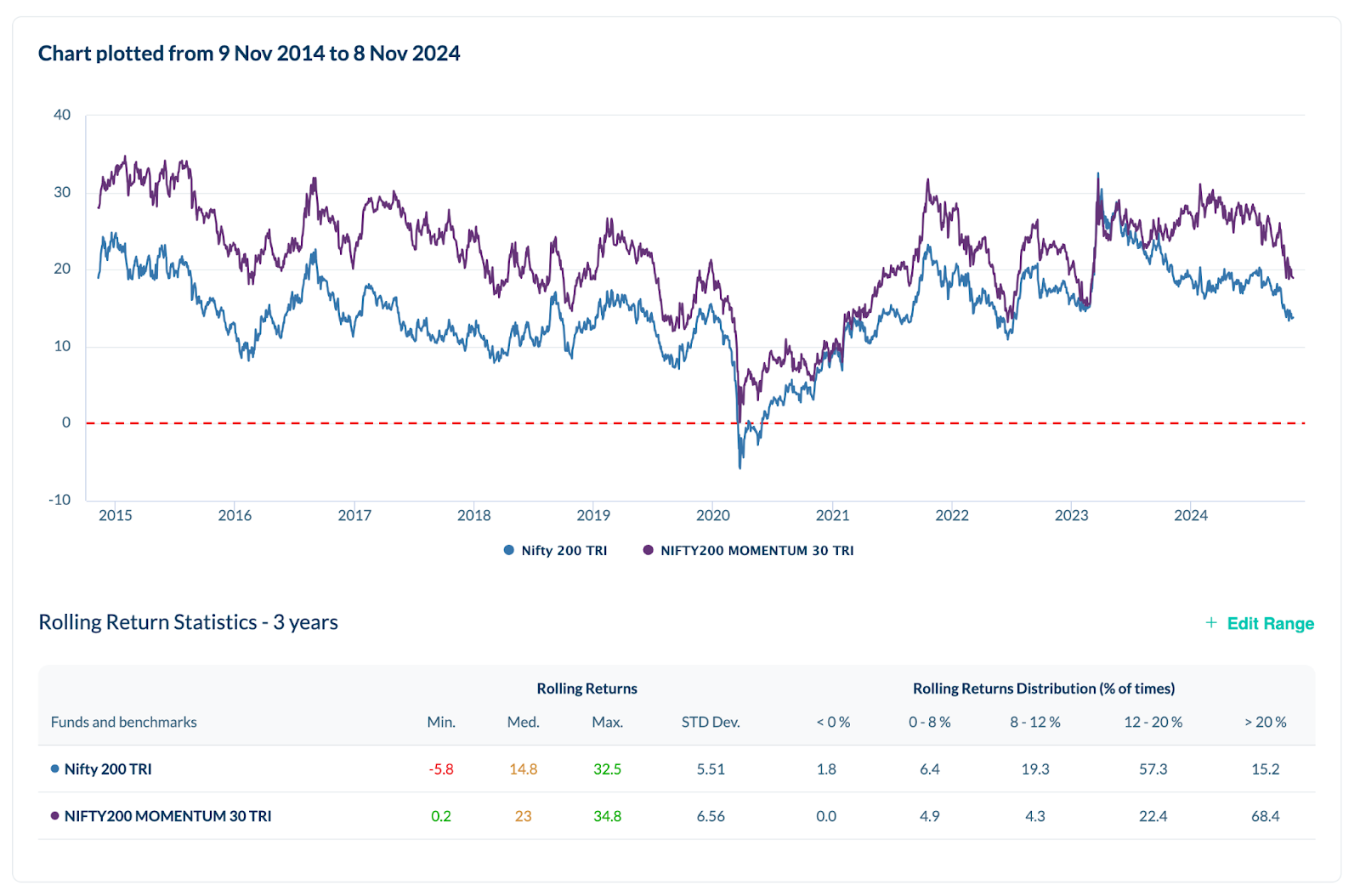

But checking point-to-point returns never shows how volatile and consistent the fund has been during this time frame. So we should better check the Rolling returns. Below is the 3 years rolling returns in the last 10 years

Of course, with a bit of high volatility, the returns generated by the Momentum investing fund are way ahead of that of the benchmark. One thing I need to point out is, that if you check the covid fall time, March 2020, you can see that Momentum has done quite well in protecting the fall also.

All the above charts show a comparison with the Parent index i.e. Nifty 200, which is mostly considered to be the benchmark of Large and Midcap along with Nifty 250. So we should also see the returns comparison with some Good active funds as well as nifty 250, to understand it better.

The below chart shows the same.

In the last 10 years if we see 3 years of rolling returns, Nifty 200 Momentum 30, has performed decently even if compared to the Nifty 250 index.

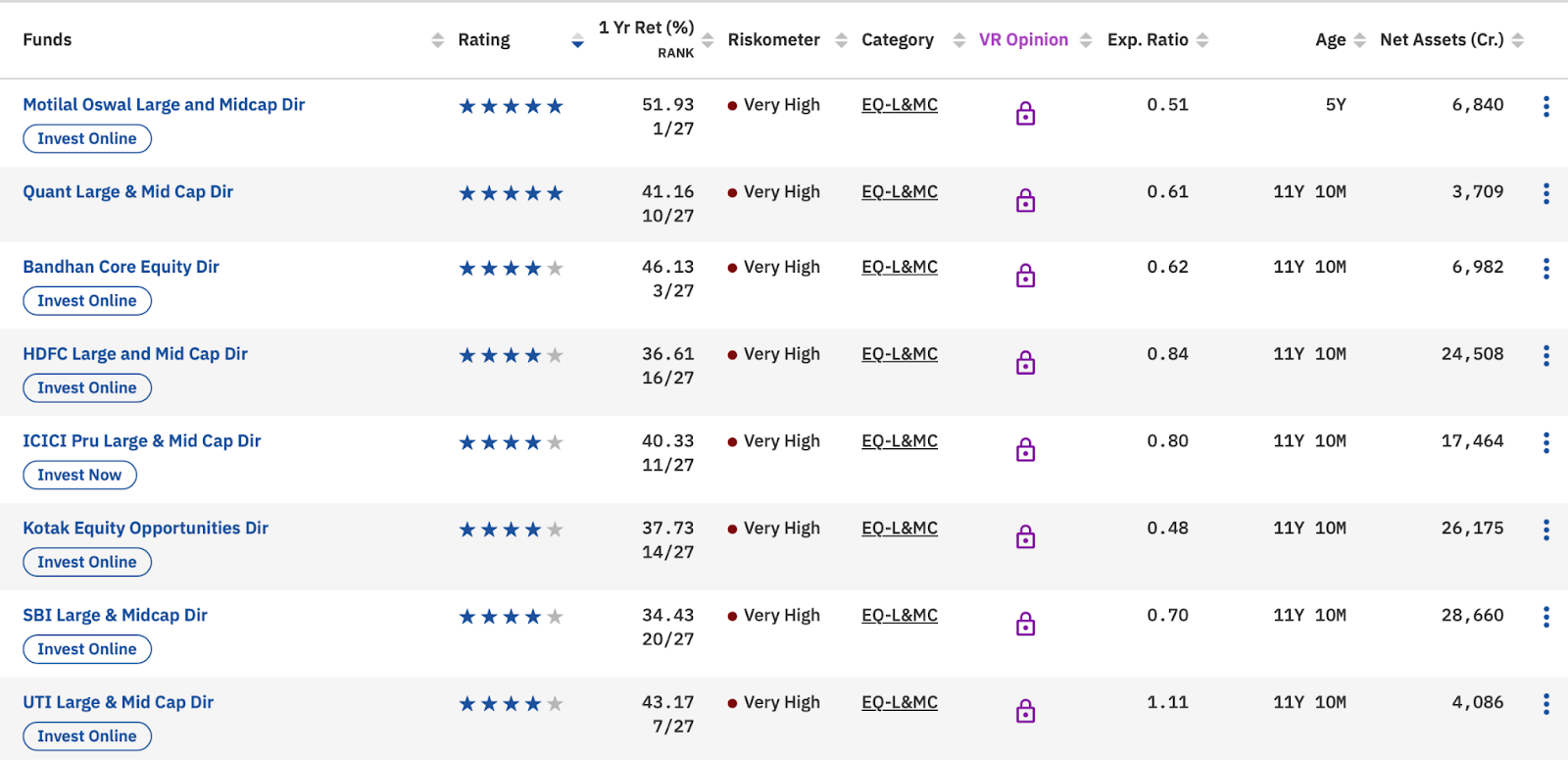

Now to have a last check, let us see, how well this strategy has performed in comparison to the active funds. Active funds that come under the large and Mid-cap category are required to keep at least 35% in large cap and 35% in mid-cap.

For my comparative analysis, I have taken those funds which as per value research online come under 4 and 5-star ratings, shown below

Mutual funds were recategorized in 2017-18, so if we have to compare the active funds then it is wise we do not look at 10 years’ data, but the last 7 years’ numbers. And for only those funds which has at least this much history. Besides the above, I have taken the liberty to add Mirae Large and Midcap and Canara Robeco emerging Equity into the list

Also read: Why Beating the Benchmark Isn’t Always the Best Investment Strategy

Longer the time frame median and average returns is something which you should look at. Min returns tell you the maximum drawdown this scheme has experienced and Standard deviation is the volatility in the scheme during this period.

Conclusion:

Momentum investing does sound like a volatile strategy, but after seeing all the numbers I found the results to be very much comparable to the other active and passive counterparts, and do not find any reason to not mix it up with the long-term portfolio. It has even done better in some cases in comparison to active funds which normally be considered for long-term investing.

As I mentioned in the beginning, momentum funds are benchmarking different broad indexes, so you need to be watchful of the liquidity concerns that may come up in bear phases, in the small and mid-cap segments. This factor-based index does not consider the hygiene of stocks, it just chases the momentum, which may create a problem in some segments

Now, when I say that this fund is fine to be a part of a long-term portfolio, please do not consider this to be advice. The final decision to invest in this or not lies with you and your advisor. Please do your research, and decide as per suitability and risk profile.

The Sources of all the above tables and charts are www.dspim.com/portfolio-creator

Explore: Smart Beta Funds – Is this the new age way of Investing? and How Mutual Fund Benchmarks helps in selecting the Right Fund for you?

{kind=link}