Ankit, a 47-year-old professional, had spent over two decades in the UK building a career, raising a family, and securing his financial future through workplace pensions and investments. Yet, with teenage kids and aging parents, he felt a strong pull to reconnect with his roots in India. Coming from an agricultural background, Ankit decided to manage the farmlands owned by his family. However, the complexities of transitioning his financial life from the UK to India left him feeling overwhelmed.

Upon a friend’s recommendation, Ankit reached out to us for guidance. He sought clarity on managing his UK pension, taxes, and investments in a way that aligned with his plans to resettle in India. His main concerns were:

- Should he withdraw or retain his UK pension investments?

- How could he manage the tax implications effectively?

- What steps were necessary to safeguard his financial stability during this significant transition?

In most cases, The first step is always to address taxation and currency management. A written financial plan tailored to the Indian context usually resolves these concerns. However, the subjective debate between the standard of living and quality of life remains. This is where astute money management becomes crucial. While liquidating self-acquired investments and repatriating the funds to India is straightforward, UK pension plans necessitate a distinct approach.

There is no option for him to withdraw the corpus before his age of retirement as per UK pension rules. Moreover, For NRIs like Ankit, who want to retire in India after years of working in the UK, managing a UK pension can be complex. With options such as the Qualifying Recognised Overseas Pension Scheme (QROPS), transferring UK pensions to India offers NRIs the chance to avoid the UK’s lifetime allowance tax and to manage currency risks by converting their pensions to INR.

This guide covers how NRIs can transfer their UK pensions, the benefits of QROPS, and the tax implications involved.

This is the 3rd article on the series of International pension schemes for NRIs. Earlier we have written detailed article on

Understanding UK Pension Schemes

Pension schemes in the UK are essential for ensuring financial security during retirement. These schemes can be broadly categorized into three types: State Pensions, Workplace Pensions, and Personal Pensions. Let’s take a closer look at each.

State Pension

The State Pension is a government-provided income for individuals who have reached a certain age and have made sufficient National Insurance contributions throughout their working life. Here are the key points:

- Eligibility: To qualify for the State Pension, you need at least 10 qualifying years of National Insurance contributions, with a full pension requiring 35 years of contributions.

- Payment Amount: As of the 2024/25 tax year, the maximum new State Pension is £221.20 per week. Payments are typically made every four weeks.

- Age: The current State Pension age is 66, but it will rise to 67 between 2026 and 2028, and future increases to 68 are planned by 2046.

Workplace Pensions

Workplace pensions are employer-based schemes to provide retirement benefits. There are two main types:

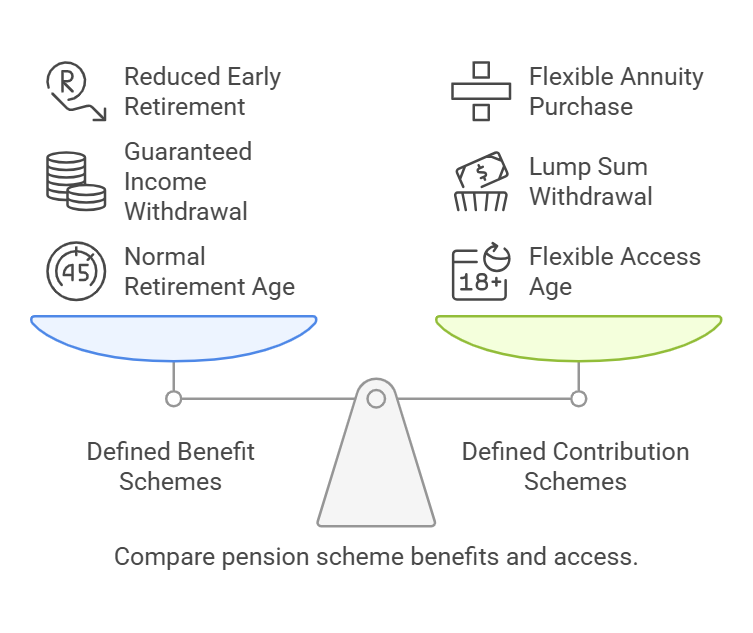

- Defined Benefit (DB): Guarantees a specific income based on your salary and years of service. Less common in the private sector today.

- Defined Contribution (DC): Contributions from both employee and employer go into a pension pot invested over time, with the final amount depending on investment performance.

Also read: How to generate Monthly income from your savings?

Personal Pensions

Personal pensions are individual plans anyone can set up, regardless of employment status. They offer flexibility in contributions and investment options.

Withdrawal Rules for Various Pension Schemes in the UK

Here’s an overview of the withdrawal rules for State Pension, Workplace Pensions, and Personal Pensions:

State Pension

- Eligibility Age: The State Pension can be accessed at the State Pension Age (currently 66, rising to 67 by 2028).

- Withdrawal Process: Once eligible, the State Pension is paid automatically without any action required on your part, based on your National Insurance contributions. NO Lumpsum Withdrawals allowed.

Workplace Pensions

The withdrawal rules for workplace pensions in the UK differ between Defined Benefit (DB) and Defined Contribution (DC) schemes.

- Defined Benefit (DB) Schemes:

- Access Age: Benefits can typically be accessed at the Normal Retirement Age (NRA), often 65. Early retirement may be possible but results in reduced benefits.

- Withdrawal Method: Provides a guaranteed income based on salary and years of service, rather than a lump sum.

- Early Access: With employer consent, early retirement may be possible but usually with reduced benefits.

- Defined Contribution (DC) Schemes:

- Access Age: Individuals can access their pensions from age 55, rising to 57 by 2028.

- Withdrawal Options: Individuals can take a tax-free lump sum of up to 25% of the pension pot. After age 55, withdrawals can be made flexibly.

- Annuity Purchase: An individual may choose to convert the pension pot into a guaranteed income via an annuity.

Personal Pensions

Personal pensions generally follow similar rules to workplace pensions.

- Access Age: Individuals can access funds from age 55, rising to 57 in 2028.

- Withdrawal Options: Up to 25% of the pension can be taken tax-free, and the rest can be converted into an annuity or withdrawn as flexible sums.

- Tax Implications: Withdrawals beyond the tax-free lump sum are taxed as income.

Tax Implications for UK Pensions

For those planning to return to India, understanding the tax rules related to UK pensions is crucial.

In simple words, withdrawals beyond a permissible tax-free limit of 25% in respective pension schemes are taxable, taken either in lumpsum or in annuity form. However, If you withdraw when in India, you can take DTAA advantage to avoid double taxation.

Options for NRIs Moving Back to India

When Indians who have worked in the UK decide to move back to India, they face important decisions regarding their pension funds. Let’s explore the primary options available, along with their pros and cons.

Option 1: Leave the Pension in the UK

Pros:

- Continued Growth: Keeping the pension in the UK allows it to continue growing tax-deferred until withdrawal at retirement age.

- Access to Tax-Free Lump Sums: Upon reaching retirement age, individuals can withdraw up to 25% of their pension as a tax-free lump sum. (However, this depends on the Tax residency then)

Cons:

- Currency Risks: Holding a UK pension exposes individuals to currency fluctuations, which can affect the value of their retirement savings when converted to Indian Rupees.

- Restricted Access Before Retirement Age: Accessing pension funds before reaching retirement age is generally not permitted, limiting financial flexibility.

Option 2: Transfer Pension Funds to India

- Transferring UK pensions to India involves moving funds into a Qualifying Recognised Overseas Pension Scheme (QROPS), which is approved by HMRC.

Why Consider UK Pension Fund Transfer to India?

Transferring your UK pension can make sense if you’ve moved out of the UK or if managing it within the UK isn’t the most efficient option for your financial goals. For instance, one of my clients, Shekhar, returned to India after spending 15 years in the UK. He wanted better control over his retirement funds, given the currency risks and the changing tax landscape. A pension transfer seemed like a logical step for him.

Also read: How do Pension Plans in India work?

However, it’s not a one-size-fits-all decision. The potential benefits include:

- Simplified Management: Consolidating your pension into one place makes it easier to track and manage.

- Tax Efficiency: Depending on the destination country, you could reduce tax liabilities.

- Currency Alignment: Avoid the impact of unfavorable currency movements by holding your funds in a currency you spend in.

Many Indians who have worked in the UK and are planning to return may want to transfer their pensions back to India through a Qualifying Recognised Overseas Pension Scheme (QROPS). This allows the pension to be managed more effectively within the Indian financial system and avoids the UK’s Lifetime Allowance Tax.

It’s also important to note that the UK State Pension can continue to be received in India, though it may be frozen at the amount when individual moves abroad, and future increases might not apply.

Considerations Before Deciding on the UK Pension fund Transfer to India

- Regulations for Transferring: To transfer a pension, individuals must ensure their UK pension is eligible and that they select a QROPS in India that meets HMRC criteria. Most private or workplace pensions qualify for this transfer, but some defined benefit schemes may have restrictions.

- Recognized Overseas Pension Schemes (ROPS): QROPS allows for tax-efficient transfers of pension funds. The process includes checking eligibility, selecting a reputable QROPS provider in India, and informing the UK pension provider about the intended transfer. There are various QROPS options available in India, such as those offered by ICICI Prudential, Kotak Mahindra, and HDFC.

- can generally be transferred to a QROPS-compliant Indian pension scheme.

Costs and Taxes on Transferring a UK Pension fund to India

Overseas Transfer Charge: A 25% charge applies if you transfer your pension to a country other than the one in which you’re living. However, if you’re relocating to India permanently, this charge doesn’t apply as long as the funds stay within the overseas transfer allowance limit of £1,073,100.

Lifetime Allowance: Transferring to QROPS can help you avoid the lifetime allowance tax of 25% on UK pensions exceeding £1,073,100.

Income Tax on Withdrawals: Once in India, you’ll be subject to Indian tax laws on pension withdrawals. A tax-free lump sum of 25% is available, with the remainder taxed as income in India. However, even for the tax-free withdrawal in the UK, you may have to pay taxes in the country of your tax residency.

QROPS Eligibility and the Five-Year Rule

QROPS eligibility requires:

- Being aged 18 to 75

- No withdrawals from UK pensions in the past five years

- Active UK-based pension fund(s)

The “five-year rule” mandates that any withdrawals made within five years of the transfer must be reported to HMRC, ensuring compliance with UK tax laws.

How to make a QROPS transfer?

This QROPS transfer process can take up to 5-8 weeks.

Step 1: Consult with your advisor

Before making any final decision about transfers, you must be aware of the applicable rules and regulations for QROPS-compliant transfer to India, if required take guidance from a professional financial advisor. The rules and laws keep changing and it is of utmost importance that you stay on top of your game when handling your hard-earned post-retirement income.

Step 2: Select a QROPS provider in India

After thorough analysis and professional advice, pick a QROPS provider in India. Do keep in mind that not all pension plans in India are QROPS compliant. Please take into consideration factors such as annual charges/fees, investment options, payout options, etc. as part of the selection process.

Step 3: Inform your UK pension provider

After selecting the pension provider in India, inform your pension provider in the UK with whom you are currently enrolled. After this formal notice, you will be provided with a set of transfer forms and other documents required to transfer funds under the HMRC-approved QROP scheme.

Step 4: Apply for the transfer

You’ll need to download and complete Form APSS 263 from the UK Government website. This asks for information such as:

- Your details and National Insurance number

- Address and contact information for you in the UK (or your previous UK address if you’ve already moved)

- Details of the QROPS – including the name, address, country in which the scheme is established and regulated, and its HMRC reference number

- Your employment details (if relevant)

Step 5: Complete & Submit the transfer forms

Once you’ve filled out the form, send it to your UK pension scheme manager to kick off the transfer. Make sure you include all the info needed on the form. If any details are missing, regardless of other transfer specifics, it will be taxed 25% if you don’t submit everything within 60 days.

Once your QROPS request and forms are checked along with the needed papers, your UK pension funds will move to an India plan under the UK QROP scheme.

NOTE: You can’t transfer a UK state pension over to India, but you can receive your pension payments from it once you move. To be eligible, you’ll need to be up to date on National Insurance (NI) contributions. People who’ve lived or worked abroad may also be eligible.

You’ll just need to apply to the International Pension Centre within 4 months of your state pension age.

Timeframes and costs involved

The time it takes to move a UK pension abroad depends on the companies you’re dealing with and how quickly you reply to their requests.

After sending your application form, make sure you provide all the needed details within 60 days. You might need to contact your pension provider, and maybe also the QROPS provider in India, to learn more about how long the process might take.

As for costs, there’s a key fee you should be aware of: the overseas transfer charge of 25%. If you’re relocating to the country of the QROPS, you likely won’t need to pay this.

But, if your transfer is over your overseas transfer allowance (OTA), which is £1,073,100, you might have to pay 25% on the excess amount.

UK Pension Fund Transfer to India – Is Transferring Your Pension the Right Move?

For NRIs planning to stay in India permanently, transferring UK pensions to a QROPS can provide more control, currency stability, and potential tax savings. However, consider factors like annual fees, investment control, and potential penalties if you exceed the transfer limit.

Transferring a UK pension to India isn’t for everyone. For NRIs intending to keep ties with the UK or needing income flexibility, retaining UK pensions could still be viable. Weigh the pros and cons with your financial advisor to make the most informed decision.

Disclaimer: This article is for general information purposes and is written referring to the sources we could find online. As the rules also keep changing, it is advisable to consult a professional financial advisor in your country and decide as per your financial plan and requirements.

{kind=link}