Last week, I met Raghav, a software engineer from Mumbai, at a coffee shop through a client. Raghav had questions about his personal finances and wasn’t sure who to consult, so he reached out to his friend, who is also my client.

Raghav’s financial challenges stemmed from investing through a Fintech app. He began with mutual funds, then moved to stocks and Futures & Options (F&O). Due to a liquidity crunch, he took a loan against his securities to manage personal finances. Now, his portfolio is showing losses, and he is hesitant to liquidate, which led him to borrow against his investments for financial stability.

Raghav’s situation is not unique. Many individuals today, enticed by free investing through fintech platforms or lacking awareness of financial planning resources, have fallen into similar pitfalls of self-inflicted investment errors. While the platforms themselves are not the sole issue, a prevalent mindset exists that prioritizes free offerings over professional guidance. In a previously favorable market environment, many felt they possessed sufficient knowledge and dismissed the need for expert advice, a decision they now regret.

In this article, I’ll share the advice I provided to Raghav and numerous other investors over the years. The key is to keep things simple and manageable. Ensure a strong financial foundation is in place before investing. Acknowledge that your knowledge will always have limitations, regardless of the resources available for research. Therefore, seeking professional financial guidance will be beneficial. This article focuses on managing finances during economic uncertainty. We will cover budgeting, building an emergency fund, and adopting prudent financial practices. These strategies will help you remain calm, focused, and financially secure, regardless of market fluctuations. If this information isn’t directly relevant to you, please consider sharing it with others who may benefit.

1. Budgeting: The Foundation of Financial Stability

Budgeting should be a fundamental practice. You need to understand where your money is going; otherwise, you cannot make informed financial decisions or corrections. It’s common for individuals to become less disciplined with their spending once they feel financially secure, but this can be detrimental. I have personally witnessed how a well-structured budget can significantly improve financial well-being. Your spending habits reflect your values and priorities, so it’s crucial to use your money wisely to achieve your goals. Consider implementing the following strategies, if you do not have a written financial plan and no adviser to guide you.

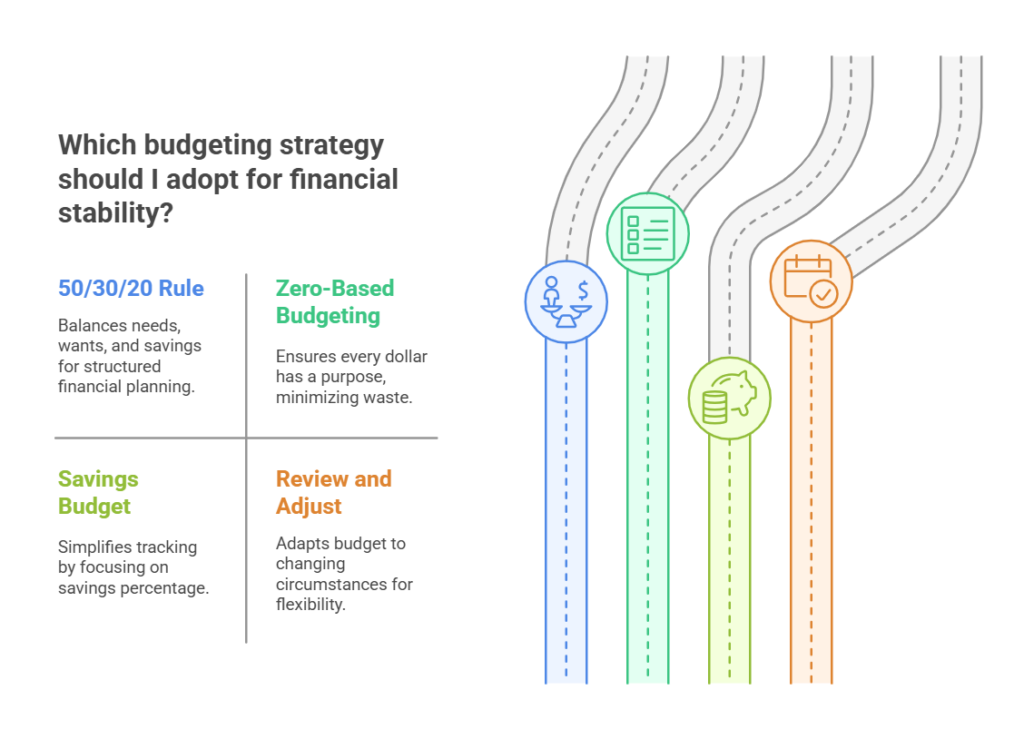

- The 50/30/20 Rule: This is a framework I often recommend. Allocate 50% of your income to needs (housing, utilities, groceries), 30% to wants (entertainment, dining out), and 20% to savings. If you have loans to repay, work on your spending pattern and dip into the other 80% or the 30% of Wants Spending. Also, if you have a modest lifestyle, then also try to increase the savings in a structured manner for your goals.

- Zero-Based Budgeting: Every penny has a job. At the start of each month, assign a purpose to every rupee you earn. This method ensures nothing is wasted and helps you stay intentional with your spending.

- Spending Vs Savings Budget: If you find it difficult to track your money and don’t like to go deep into your spending, the alternative is to have a savings budget in place. You need to fix a specific percentage you need to put into your savings.

- Review and Adjust: Life changes, and so should your budget. I advise my clients to review their budget monthly, especially during economic uncertainty. Are there subscriptions you’re not using? Can you cut back on discretionary spending? Small tweaks can make a big difference. In my book The Art of Being Good with Money, I have shared some practical examples on how a proper budgeting exercise can improve your finances. Do read.

2. Emergency Funds: Your Financial Safety Net

One of the most common mistakes I see is people underestimating the importance of an emergency fund, especially in bull markets supported by positive economic sentiments. Positive times make you believe everything is going in your favor and you can manage any challenge comfortably. In my more than two decades of Career as a financial planner, I’ve worked with clients who’ve faced job losses, medical emergencies, and unexpected repairs, travels. Those with an emergency fund were able to handle these challenges without derailing their long-term goals.

- How Much to Save: While the standard advice is 3-6 months’ worth of expenses, I tailor this based on individual circumstances. For example, if you’re a freelancer or have irregular income or even are above 40 years of age, aim for 6-12 months. If you’re young and in a stable job, 3 months might suffice.

- Where to Keep It: I always recommend not to look at the emergency fund from an Investment angle, still there are liquid avenues which one may explore to park the emergency fund for better yields. Also read: Emergency Fund Investment Options. It’s safe, earns interest, and is easily accessible. Avoid tying this money up in investments—it’s there for emergencies, not growth.

- Start Small, Think Big: If saving several months’ worth of expenses feels overwhelming, divert your minimum 20% Income savings as explained above completely towards the emergency fund, and gradually build up the volume.

3. Avoid Borrowing at all costs

Regardless of circumstances, avoid substantial borrowing until you have established a basic financial safety net. Maintaining an emergency fund and liquidity within your investments is crucial. Failing to adhere to these fundamental principles and accumulating debt will lead to financial difficulties, similar to the situation Raghav faces.

Borrowing can create a disconnect from financial reality. Market conditions are constantly changing. If you’ve already invested in high-risk assets that are susceptible to external factors, taking out a loan against those volatile assets further increases your risk. Even if you have initial success, consistent gains are not guaranteed. Often, early profits can lead to overconfidence and greed, which may result in significant losses later on. It’s important to remember that even if you’ve made money in the beginning, that doesn’t mean you will keep making money always.

Even when you are in a better financial position with sound financial habits and sufficient income to comfortably manage EMI payments, it’s crucial to distinguish between beneficial and detrimental loans. Also read: Types of Loans: Beneficial vs Detrimental. Aim to finance only 50% of your needs through borrowing, using your resources for the remainder. Alternatively, prioritize saving first and then making the purchase later.

Financial Prudence is the first step to a good Investment Management

4. Prudent Financial Practices

- Avoid Lifestyle Inflation: When times are good, it’s easy to upgrade your lifestyle—bigger house, nicer car, more dining out. But during uncertain times, it’s crucial to live below your means. I’ve seen clients who maintained a modest lifestyle fare much better during downturns.

That does not mean you should not spend for fun or not spend lavishly, but you should know your limits. Having a written financial plan can act as a guiding light for your actions, and can give you the answers on how much you can afford, how much is required for other goals, how to set limits on your expenses, and let you learn to delay Gratification.

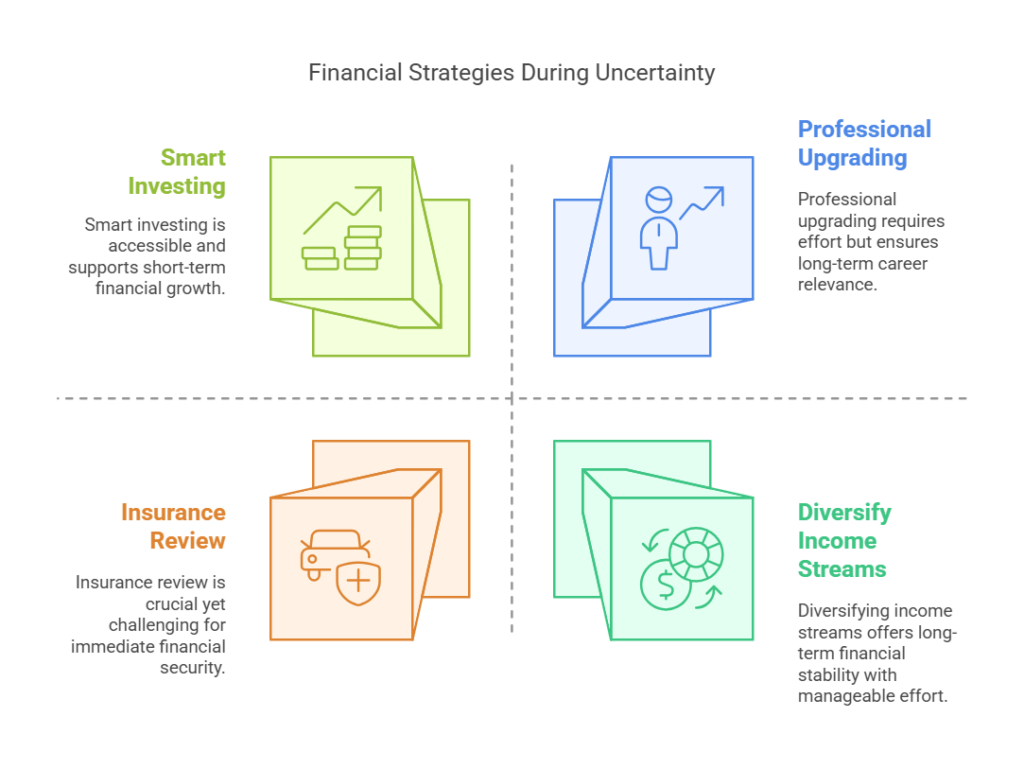

- Diversify Your Income: It may be easier said than done, but if possible, this could be one area which can give your finances a good level of confidence to deal with future uncertainties. Also read: How to build a second source of income. Having 2 or more income earners in the family, or having a decent corpus to let you earn through dividends or Interest income. I am not sure of Rental Incomes, as rental yield is so low in India, and if the purpose is to have income support, real estate may not suit you well. These days youngsters do side hustles, online freelancing work..so keep looking for options. But don’t stress yourself out

- Keep upgrading professionally: If adding multiple Income streams looks difficult, keep upgrading yourself by adding new certifications, reading books, learning new things, to stay relevant in the job market. This will at least help you save your current income and even let it grow.

- Stay Invested, But Be Smart: Market volatility can be nerve-wracking, but I always remind my clients that investing is a long-term game. Panic selling during a downturn locks in losses. This is the time to rebalance your asset allocation. Instead, focus on a diversified portfolio that aligns with your risk tolerance and goals. If you’re unsure, consult a professional to review your strategy.

- Insurance: Your Financial Safety Net: Over the years, I’ve seen how the right insurance policies can prevent financial disasters. Review your health, auto, home, and disability insurance to ensure you’re adequately covered. It’s better to have it and not need it than the other way around.

5. Mindset Matters: Staying Calm and Focused

In my experience, the emotional side of money is just as important as the numbers. Economic uncertainty can trigger fear and anxiety, but staying calm and focused is key. Here’s what is important to know

- Focus on What You Can Control: You can’t predict the stock market or the economy, but you can control your spending, saving, and investing habits.

- Celebrate Small Wins: Did you stick to your budget this month? Add Rs.1000 to your emergency fund? Celebrate those victories! They add up over time.

- Seek Support: If you’re feeling overwhelmed, don’t hesitate to reach out to a financial planner or a trusted advisor. Sometimes, an outside perspective can make all the difference.

Managing personal finances in economic uncertainties — Concluding thoughts:

In the last 2 decades of my experience, I’ve seen market crashes, recessions, and bull markets, slowdowns. Also I’ve seen incredible resilience and success stories. The common thread? Those who took proactive steps to manage their finances came out stronger on the other side.

Economic uncertainty can feel daunting, but it’s also an opportunity to reassess, refocus, and strengthen your financial foundation. By budgeting wisely, building an emergency fund, and adopting prudent financial practices, you can navigate any storm with confidence.

If you’re feeling uncertain about your financial future, know that you’re not alone. Whether it’s creating a budget, building an emergency fund, or crafting a long-term financial plan, my goal is to empower you to take control of your money and your life.

{kind=link}