There is 16 type of debt funds as defined and categorized by SEBI. And thus, overlapping of strategy and portfolio is quite normal.

Though the initial idea was to simplify the products for Investors to understand clearly and make informed choices, in many instances it has led to an increase in confusion too.

A lay investor has only one target i.e. to get Returns in fact “High Returns” and thus hardly pay heed to the type of debt funds and the portfolio the fund is having. The only parameter of fund selection remains the Past returns.

This is the reason many investors who had invested directly and looked at the Past returns are nowadays having a high allocation to the credit risk fund, which has resulted into the portfolio skewed towards Credit and default risk.

When you have a single type of debt funds allocation in the portfolio which may be the flavor of the time, expose you to High risk which may not be good for Investments portfolio health. Also read: Types of Risks in Investments

Today I will be discussing with you the different Type of Debt funds available in the market and what kind of portfolios they have, which you should consider while investing in any. It may sound a bit technical, but this is how investing goes. So please bear with me. And for any clarification, feel free to ask on Chat or Comments section.

Type of debt Funds – Knowing them well

The major difference in any 2 debt funds, and which has become the basis of this classification and categorization is

the Duration of the Papers (Bonds/Debentures), and the type of securities (Corporate bond/Government securities), a fund’s portfolio is carrying. Duration comes from the Average maturity of the Securities.

So broadly in terms of Duration, you will find, very short term, short-term and long-term kind of fund where the name itself suggest the maturity of portfolio papers,

and in terms of Type of securities, you will find Government securities fund and Corporate securities Funds.

However, there’s a specific differentiation in one fund where the Portfolio carries banking and PSU sector securities, which is why the name goes as “Banking and PSU fund”. This may have a mix of Maturity and Ratings. Since Banks sometimes issue long-term perpetual bonds and sometimes lower duration deposits and same goes with PSUs.

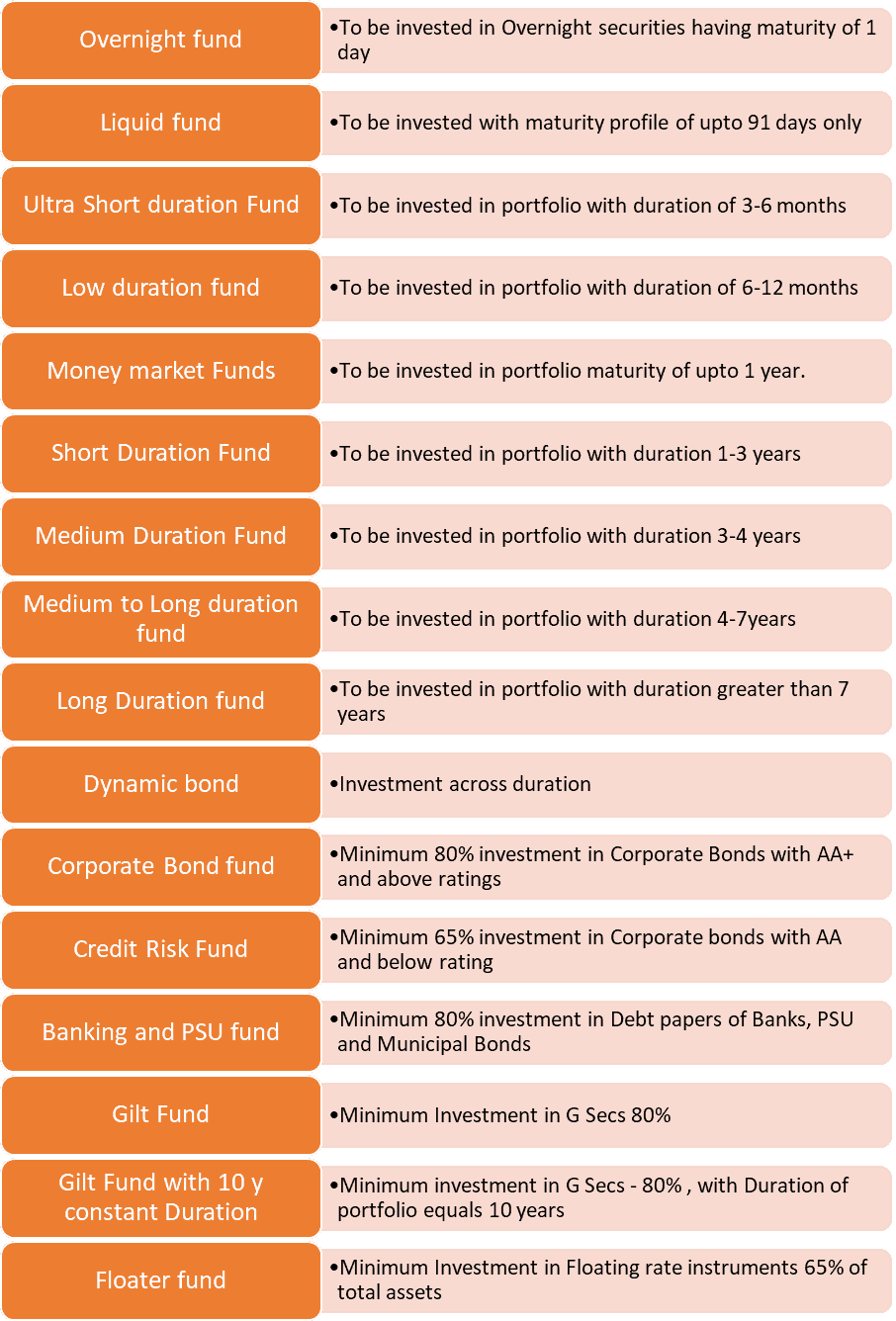

Below is the List of categories on the type of debt funds

These category names will guide you on what kind of portfolio you may expect the fund has, but the confusion will come when you want to be in duration fund but not sure what kind of portfolio the same will have.

The quality and rating of papers are very clear in Corporate Bond and Credit risk funds, but in the duration funds, you will not be sure unless you go into the portfolio in detail.

Here comes the role of Good advisor to help you invest into Suitable Debt mutual funds.

Type of Debt Funds – How to make the selection?

This depends on your Requirement. First of all, one thing that is important to understand is that the debt funds should definitely be a part of one’s portfolio.

The purpose of a debt fund is not to generate High returns but to provide a stability and less volatile portfolio, along with a tax-efficient return as compared to the other traditional instruments.

Also read: Fixed maturity plans, a tax-efficient alternative to Fixed deposit

There are 3 different criteria while selecting a Debt fund.

- Your Investment time horizon. Your time horizon comes from the goal that you are targeting.

You may very well see from the chart/table above that what tenure of the portfolio a specific fund would carry. So, your investment time horizon should match with the fund portfolio duration. It may be lower but should not be higher.

Please understand that since Bond prices are Inversely related to Interest rates, so higher the duration of the fund higher would be the volatility. In Rising Interest rate scenario, your high duration portfolio would be showing you very volatile and even falling returns, and in the falling scenario, it will be showing you mouth-watering returns too.

But Like equity, you never know which side the Interest rates will move and when so better to stick to the fundamental selection process.

For long-term allocation, you may go with Long duration funds (even through SIP route) and may have a mix of Short and Long duration funds. But for shorter Horizon, you should stick with Short duration funds.

- The type of portfolio. This is important when you understand the Credit Risk in the fund. Government securities are the safest in this segment, but due to high duration papers, they are always exposed to Interest rate risk.

Corporate papers are rated by credit rating agencies, which shows how risky the papers are. Though High rating does not guarantee full safety, still you may assume papers are of good quality, at least better than the lower rated ones.

Lower-rated papers will be giving a higher rate of interest than good quality ones, so here you need to decide, what you want. Good quality at a low rate, or High rate with low quality.

- The expected interest rate scenario. Now, this is like predicting where will you see equity markets in near term. Some part of it depends on your understanding, some of your recent readings and “Experts Views” and some on wisdom. If your Wisdom says “I don’t know” then its best to go to Step 1. Else you may select among the duration plans.

Conclusion:

Knowledge of the type of debt funds available is very important to design a good sustainable Investments portfolio. These are the must-have component in any portfolio.

Like equity, Debt also has a tendency to be volatile and give you negative returns, and unlike equity, the recovery in debt funds would be slow. So it is very important to have the right categories, with right duration suitable to your risk profile as well as goals.

{kind=link}

I think very nicely explained about the types of debt securities and duration of debt securities. Very nice way to explain the nuances of debt funds.

Thank you very much.

Thanks, Kamal Ji.

Today is 11th January 2020. I have some spare cash I need to park for 6 months to 2 years. How do scenario of “Ultra Short Term Bond” and “Short Term Fund” look to you and which one will you prefer and why.

Being SEBI Registered Investment Advisors, we give advice only to our clients and cannot provide the name of the fund without knowing your financial background, on this open platform.