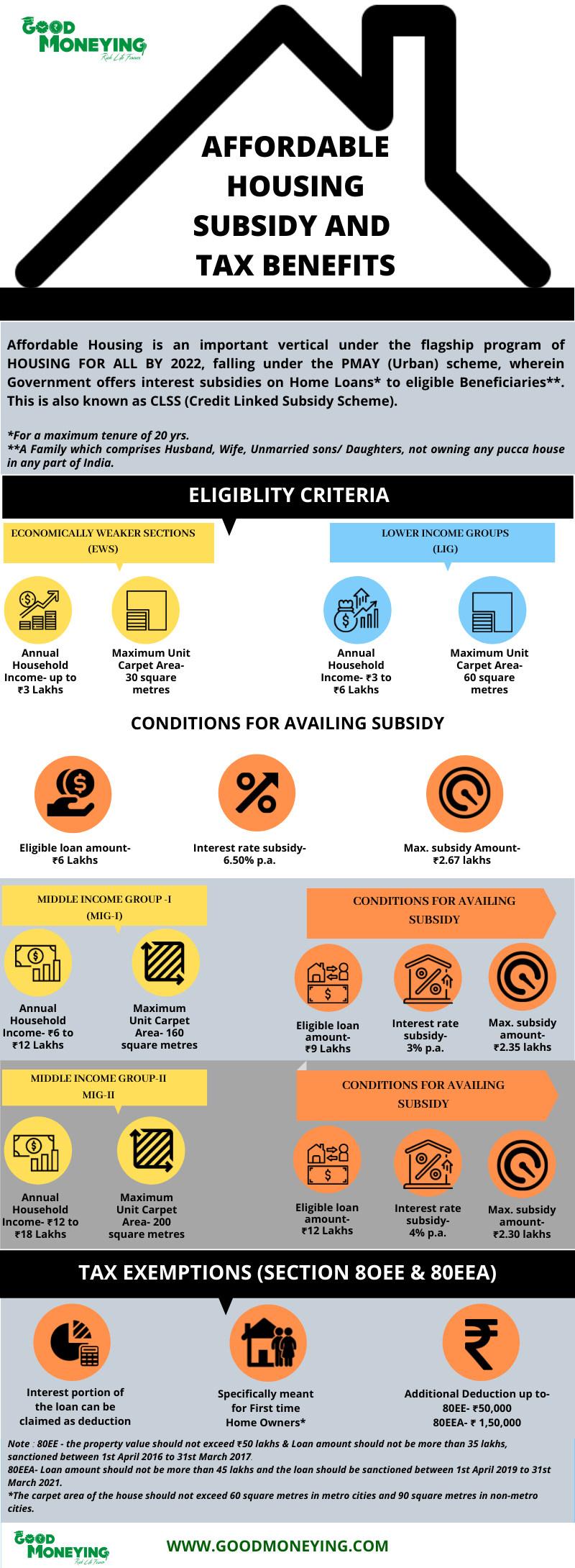

Affordable housing is an important vertical under PMAY (Pradhan Mantri Awas Yojana), wherein government offers interest subsidy to the eligible beneficiaries, for the purchase and construction of houses, falls under the conditions specified. It is also known as Credit Linked Subsidy Scheme (CLSS).

Apart from this, first time home buyers in affordable housing segment are also allowed additional tax exemptions under section 80EE & 80EEA on home loans, in addition to the previous ones u/s 80C and 24B, which are available for every home buyer.

(Also read: All you wanted to know about home loan tax benefits)

All this falls under the flagship program of Housing for all by 2022.

In the Union Budget 2020-21, the tax benefits under section 80EEA are extended for loan sanctioned up to 31st March 2021, which was previously up to 31st March 2020.

In Budget 2021-22, it is again extended till 31st March 2022.

The provisions relating to these sections are explained in this post infographics.

What is the Affordable housing scheme?

There is no specific definition of the affordable housing. However, as the name suggests it is meant to support the people who otherwise could not afford to buy their own house in this ever-rising property market.

So, along with providing benefits to builders to come up with affordable housing projects in their offerings, the Government also offers some incentives in the form of interest subsidy and tax benefits to the buyers.

Who are the Beneficiaries under the Affordable Housing Scheme?

An eligible beneficiary family to claim Interest subsidy, would comprise husband, wife, unmarried sons and/or daughters, not owning any pucca house either in his/her name or in the name of any member of his/her family in any part of India.

However, an adult earning member (irrespective of marital status) of any family can be treated as a separate household, if he doesn’t own any pucca house in any part of India.

Which means that major children/married couple staying in a house, owned by their parents or on rent can opt for PMAY provided they are earning and don’t own any other home.

But married couples will be eligible for a single house, bought by either of the spouses or both together in joint ownership.

Beneficiary families eligible for affordable housing benefits would be identified and selected using the Socio-Economic and Caste Census of 2011, mainly including the Economically Weaker Sections (EWS), Lower Income Groups (LIG) and Middle-Income Group (MIG).

While the annual income for EWS category beneficiaries is capped at Rs.3 lakh, the annual income of LIG and MIG beneficiaries can range between Rs.3-6 lakh and Rs.6-18 lakh respectively.

There are separate conditions to avail of the subsidy for each of these income groups, which is explained in the below infographics.

Note that, beneficiaries under the EWS & LIG are also eligible for subsidies on loans taken for incremental housing i.e. for new construction and addition of rooms, kitchen, toilet, etc. to existing dwellings.

(IMPORTANT Read: How Prepared are you for buying a house?)

Affordable housing scheme – Calculation and Adjustment of Loan Subsidy:

The interest subsidy would be calculated at 9% NPV over a maximum loan tenure of 20 years or the actual tenure, whichever is lesser.

For calculating the same, the loan amortization schedule would be required, as the interest portion of each EMI shall be considered for arriving at the subsidy amount.

The subsidy amount would be credited upfront to the loan account of the beneficiaries resulting in reduced effective housing loan and EMI as well.

For instance, on a loan amount of 12 lakh, the subsidy amount comes to Rs 2.30 lakhs. So, out of the loan amount of Rs 12 lakh, this amount will get deducted and the borrowers have to pay EMI on the balance i.e. Rs 9.7 lakh at a rate at which the lender is providing loans.

Housing loans above the specified limit (refer infographic) will be at non-subsidized rates.

To conclude:

Housing for all by 2022 is one of the most important campaign launched by PM Narendra Modi. Every year in the Union budget you will find some sort of announcement to promote this campaign and encourage the builders and buyers to go for it.

Affordable housing scheme would not only give a boost to the slowing real estate sector by encouraging common masses to spur the demand for housing but is also expected to address the rising prices and affordability of the buyer.

This post- Affordable Housing scheme -Subsidies and tax benefits is written by Varun Baid.

{kind=link}