Alternative Investment Funds are another sought-after product after Portfolio Management Services. Actually, It has slowly become a general notion that Mutual Funds are commodities. Investors check out the star rating, past performance and just buy it. There is no advice needed on such instruments.

Plus, when markets are generating returns and all new investors who have made money in recent times have started believing that they can do better than the professionals.

All this has made them lookout for new exotic instruments where they find some role of professional management.

But the challenge is that where Mutual funds are meant for every kind of investor, the products like AIF and PMS are for specific high net worth individuals, who are assumed to have a high-risk appetite. (Read: How is PMS different from Mutual Funds?)

The start-up ecosystem in India is booming. India has the third-largest start-up ecosystem across the world and is expected to grow at around 12-15% annually. As per the Economic Survey 2021, more than 38 start-ups have earned unicorn status, i.e., They are valued at $1 Billion or more. As seen recently, some of them are now already publicly listed, others are in-line.

The digital outbreak happening especially after covid has paved the way for the rise of these startups. Since these businesses are technology-driven and as the adoption of digital infrastructure increases, they can show huge growth potential. Government Support has also played a significant role.

To reap the benefits of this growth story and create wealth, investors can use an Investment Vehicle called Alternative Investment Funds or AIFs. These are sophisticated financial instruments that predominantly invest in private or unlisted companies, and are slowly gaining popularity among a special class of investors.

However, Alternative Investment Funds are also into complex derivative strategies and provide investors exposure to unlisted equity and commodities through different complex structures. Complexities always attract investors, but complex does not always mean better and paying.

Let us understand this non-traditional asset class, how it works, taxation rules, and who should consider investing, in detail, in this article.

What are Alternative Investment Funds (AIFs)?

Alternative Investment Funds or AIFs are private investment vehicles that are different from conventional investments like- equities, or fixed-income securities. In this, funds are collected from a limited number of sophisticated investors to invest in private equity, venture capital, hedge funds, etc.

Residents, Non-Residents including PIOs and OCIs, as well as Foreign investors can invest in AIFs, but a single AIF scheme can have a maximum of 1000 investors (not applicable if the AIF is registered as a company). The minimum quantum required to invest is 1 crore per investor. For employees or directors in the AIF, it is 25 lakhs. Read a Detailed Post on OCI Status here

The Minimum Corpus value for each AIF scheme should be at least 20 crores, as specified by SEBI.

All AIFs have to be compulsorily registered with SEBI as a body corporate, trust, or an LLP. A separate set of regulations, known as SEBI AIF Regulations, 2012 governs the working mechanism of Alternative Investment Funds. A majority of the Alternate Investment Funds in India are registered with SEBI in the trust structure.

Other Related Article Links:

Alternative Investment Funds- 3 categories:

AIFs are classified into the following three broad categories, as specified by the market regulator, SEBI, which are further divided into subcategories, as explained below:

Category I AIFs:

These Alternative Investment Funds tend to invest in start-ups, early-stage ventures, social enterprises, small and medium-sized businesses, infrastructures, as well as sectors or areas that the government or regulators consider being socially or economically desirable. The government provides investors in these funds with some concessions or tax incentives.

Category I AIFs include:

- Venture Capital Funds: These funds primarily invest in startups and emerging businesses that have a high growth potential and are in shortage of funds. As per SEBI rules, these funds have to invest two-third of the investible surplus into the equity securities of these companies. The remaining one-third can be invested in debt securities or IPOs of unlisted companies, equity shares of any financially weak listed company (having accumulated losses equivalent to more than 50% of its net worth), etc.

- SME Funds: These funds, as the name suggests, invest in the Small & Medium Enterprises. These companies can be unlisted, listed or proposed to be on the SME stock exchange. As per SEBI rules, these funds have to invest at least 75% of the investible surplus in these companies.

- Social Venture Funds: These funds invest in those businesses which while earning profits, leave a positive social impact by solving various social and environmental problems. Some themes include- affordable healthcare, clean energy, financial inclusion, etc. As per SEBI norms, these funds have to invest at least 75% of their assets in them. (Also Read: What’s so special about the ESG Investing Strategy?)

- Infrastructure Funds: These funds invest in those firms which are into the business of infrastructure development, like- Rail, Road, Ports, Airports, Power, etc. As per SEBI norms, at least 75% of the assets of these funds are to be invested in unlisted firms and the remaining 25% can be invested in listed debt securities of companies in the business of developing, operating & holding infrastructure projects.

- Angel Funds: These funds are a special subcategory of Venture Capital Funds which also invests in startups or very early stage ventures in exchange of equity stake, providing them the required capital to boost or expand. But these funds can raise money only from Angel Investors. SEBI has defined Angel Investor as the one who satisfies any of the following conditions:

- Any individual person who has a net worth of 2 crore rupees, excluding his current home and has prior experience of investing in or promoting a start-up or is a senior management professional with at least ten years of experience.

- A company having a net worth of at least Rs. 10 Crores.

- An AIF registered under the SEBI AIF Regulations, 2012 or SEBI Venture Capital Funds Regulations (VCF),1996.

Some features of Angel Funds are different from other Alternative Investment Funds, these include:

- Minimum Investment per investor is 25 Lakhs for a period of 5 years. The maximum investment being 10 crores.

- Every Angel Fund should have a corpus of 5 crores.

- Maximum 200 investors can invest in an Angel Fund.

Category II AIFs:

Those AIFs which neither fulfill the features of Category I AIF nor Category III AIF, fall into this category. These funds invest in private, unlisted companies or units of another category I or category II AIF, as per the investment objective of the fund. Category II AIFs include:

- Private Equity Funds: These funds invest in private companies which have an established track record of being in business for some years and help these businesses grow. Private Equity funds enter when Venture Capital funds exit.

- Debt Funds: As the name suggests, these funds primarily invest in debt securities of the listed and unlisted companies but are not allowed to provide any loan to the companies.

- Fund of Funds: These funds invest in the units of other Alternative Investment Funds (category I & II) rather than directly holding the equity, debt or other securities.

(Also Read: What is Equity, it is not just stock market investment)

Category III AIFs:

These AIFs employ diverse or complex trading strategies through investment in listed or unlisted derivatives, structured products, etc. These funds can also use leverage, i.e. borrowing for investing strategy. In contrast, category I & category II AIFs are allowed to borrow only for meeting some operational requirements, that too in a very limited capacity (not exceeding 10% of the investable funds). However, SEBI has prescribed the maximum limit of borrowings for these funds as well. Currently, it is twice the value of the portfolio.

While category I & category II AIFs are closed-ended funds with a minimum tenure of three years, i.e. investors are allowed to enter the scheme only at the time of launch and funds would be locked-in for the tenure. These AIFs can be both closed-ended as well as open-ended, which means, new investors can enter and the existing investors can redeem their units in-between the tenure of the scheme. Hedge Funds are included in this category of Alternative Investment Funds.

Alternative Investment Funds- Taxation:

The taxation rules of AIFs are not that straightforward. These are different for different categories of AIFs:

Category I & Category II AIFs:

For taxation purposes, these AIFs are provided with the pass-through status, just like Mutual funds. This means any gains or losses made by the AIF, except any business income would be taxable in the hands of the investors of the fund as if the investments are done by the investor himself. The rate of tax would be the same as applicable to the Capital gains. (Read: Capital Gain Taxation Rules for Mutual Funds)

Investors can also claim losses, other than business losses (if any) after a holding period of 12 months or more. For Non-Resident Indians, any gains out of the Investments in AIFs are not taxable in India. However, they may get taxable in their Country of Residence. (Also Read: How are tax rules different for NRIs?)

Any Income/Loss in the nature of Business is taxable/allowed at the fund level itself according to the legal structure under which the AIF is registered and would be tax-exempt in the hands of the investor.

If the AIF is registered as a trust, the Maximum Marginal Rate of taxation is applicable on this income which is currently 42.74% (including surcharge & cess) and if it is formed as a company or LLP, respective tax rates will apply.

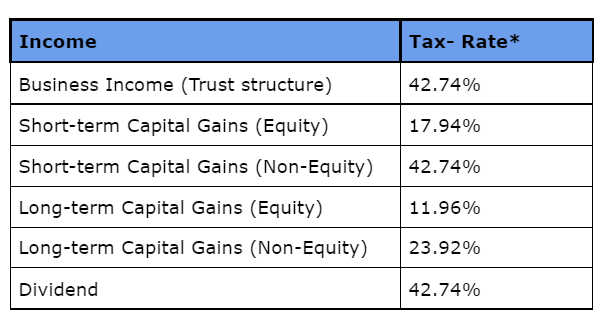

Category III AIFs:

These funds are not granted with the pass-through status. So, all incomes & gains of Category III AIF are taxable at the fund level itself and investors would receive the post-tax income from the fund. The tax rate for the same would be the Maximum Marginal Rate (MMR) which is different for different types of income. The below table explains the tax rates on different types of income earned by Category III AIFs (as per Finance Act 2020):

Should you go for Alternative Investment Funds (AIFs)?

As mentioned earlier, AIFs contribute to the economic development of our country by providing the required capital to start-ups with high growth potential, emerging businesses, and SMEs which may not get funding for any other conventional sources.

(Read: Financial Independence – How easy to achieve?)

The government is also encouraging various institutional investors and Ultra High Net worth individuals to invest in Alternative Investment Funds, by giving various concessions and tax incentives to some specific categories of funds.

AIF Investment has a number of advantages. Professional Fund Management, High-Performance Potential, Portfolio Diversification, and non-correlation with the conventional asset classes, which means that volatility in stock markets may not impact the performance of AIF Investment. (Also Read: 5 Best Things to do in Volatile Markets)

There are a number of downsides as well to the same. You should be aware that although not correlated with conventional investments, these funds are subject to higher volatility. How diversified the portfolio may be, it may happen that some ventures go completely bust, if the idea doesn’t work in the market.

In addition, the liquidity crisis is also another issue. Even after the lock-in is over, you may not be able to withdraw your investment completely. Significant credit defaults on debt papers are also a possibility. (Also Read: How to manage debt fund risks in an investment portfolio?)

The expense ratios are also very high in AIFs. High taxation rates, especially on the Category III AIFs may reduce the returns you actually receive from the fund. (Also Read: All About expense ratios in mutual funds)

So, all in all, if you are the investor with the required investment worth and has a very high-risk appetite and understand the nuances of how investing in startups work or have a family office managing your wealth, you may like to explore suitable AIFs and allocate a portion of your overall investment portfolio into Alternative Investment Funds.

{kind=link}