It felt like I was watching Sholay. The epic scene of Gabbar Singh killing -Kalia and 2 others. Actually, we have been expecting the announcement of Long-term capital gains tax on equity for the past 3 budgets i.e. Since 2015. But it was not announced.

So, 2015 bhi bach gya, 2016 bhi bach gya, 2017 was looking quite sure, that time I transacted in many clients’ investments to be prepared for such move, and thought Jaitley ji will say tera kya hoga Kalia, but who bhi bach gya

And in 2018, when chances are looking bleak, he announced not only LTCG tax on equity but also brought in the unexpected Dividend distribution tax in equity oriented mutual funds.

When budget 2018 was expected to be a populist budget, since elections are due next year, it proved to be the opposite of it. Though the measures announced may benefit the core Indian economy and country at large which constitutes of the agricultural and rural sector, economically less privileged and may benefit the country over a long period of time, but the slew of measures announced has impacted each and every strata of society in different ways.

(Download Finance Bill 2018)

Like they say different strokes for different folks.

Budget 2018 highlights – From Personal Finance point of view

The First major announcement which is going to impact all Taxpayers is the Replacement of Education and Higher education cess with Health and education cess. The new rate is 4%, 1% higher than the total of earlier two. So, brace yourself for high tax outgo

Other proposals in budget 2018 are:

- For Salaried Individuals –

A standard deduction of up to Rs 40000 or the amount of salary received whichever is less has been proposed to be allowed while calculating income from salaries. This is a welcome move.

But this deduction is proposed in lieu of Transport allowance of Rs 19200/-, and medical allowance of Rs 15000/-; and is on a reimbursement basis. So technically, if you could be able to claim the full deduction as you were claiming in the other two options, the nett benefit (deduction) you will get is of Rs 5800/- extra. And tax benefit will depend on the Income-tax slab you will be falling in.

- For Senior Citizens –

Senior citizens were given a due care in this budget 2018. A slew of measures was announced for their benefit.

- Section 80D – From AY 2019-20, the Tax payer who is a senior citizen can claim up to Rs 50000/- instead of Rs 30000 currently, for Health insurance premium as well as expenses towards preventive health check-up.

If the policy is bought for more than 1 year than the benefit can be claimed proportionately for every year.

2. Section 80DDB – For spending towards medical treatment of Specified Critical Illness, the limit of deduction has been increased from 60000/80000 for Senior citizens and Very senior citizens to Rs 100000/- for both the categories.

3. Section 80TTB – This is a new insertion in Income tax act, which is a sort of extension of section 80TTA where the Interest income from savings bank account up to Rs 10000 is exempted for all taxpayers.

But 80TTB is meant specifically for senior citizens where the Interest income from bank savings, Fixed deposits or post office savings and fixed deposits will be exempt up to Rs 50000 per financial year. Even section 194A to be amended to increase the threshold limit for deducting of TDS to be increased for senior citizens

4. Pradhan Mantri Vaya Vandana Yojana to be extended until March 2020. Also, the maximum limit in this scheme to be increased from 7.5 lakh to 15 lakhs. This is a pension scheme by LIC where 8% Return in guaranteed.

- For Investors –

As I mentioned in the title of the article, Budget 2018 is the budget which investors will remember for many years. Mainly due to the reason of Introduction of Long-term Capital gain tax on equity and Equity oriented investments.

This is not all, even the dividends from equity Mutual funds are to be taxed from now on.

Let’s understand the proposals announced in budget 2018 for investors:

- It has been made specific that the Government does not consider crypto-currencies as legal tender or coin and will take all measures to eliminate the use of these crypto-assets in financing illegitimate activities or as part of the payment system. (Also Read: Cryptocurrency- Is it worth riding the wave?)

All Cryptos Fans should know this.

2. The lock-in period of Section 54EC capital gain bonds will be changed from 3 years to 5 years from FY 2018-19. All new NHAI and REC bonds to be issued from 1st April 2018 will have 5 years lock-in period.

3. Long-term capital gain tax on Equity and Equity Oriented mutual funds has been introduced. W.e.f. 01.02.2018.

Any long-term capital gain exceeding Rs 1 lakh in equity instruments will be taxed at 10% without Indexation. However, all gains up to 31st January 2018 will be grandfathered.

Now to find out the Type of gain i.e. whether it is the long or short term, you just have to look at the period of holding of investments. But to calculate the Capital gain and tax, you have to have the cost of acquisition also.

So, government has specified the following formula to figure out the cost of acquisition of your investments

The cost of acquisitions in respect of the long-term capital asset acquired by the assessee before the 1st day of February 2018, shall be deemed to be the higher of –

- a) the actual cost of acquisition of such asset; and

- b) the lower of –

(I) the fair market value of such asset; and

(II) the full value of the consideration received or accruing as a result of the transfer of the capital asset.

Fair market value has been defined to mean –

a) in a case where the capital asset is listed on any recognized stock exchange, the highest price of the capital asset quoted on such exchange on the 31st day of January 2018. However, where there is no trading in such asset on such exchange on the 31st day of January 2018, the highest price of such asset on such exchange on a date immediately preceding the 31st day of January 2018 when such asset was traded on such exchange shall be the fair market value;

and

b) in a case where the capital asset is a unit and is not listed on a recognized stock exchange, the net asset value of such asset as on the 31st day of January 2018.

Let’s understand this with an example:

You bought 100 units of XYZ Mutual fund on 01.01.2017 at NAV of Rs 100. On 31st January 2018, the closing NAV of the same fund was Rs 140. You have plans to sell all units by 31st March 2018. Assuming the NAV on-sale date would be 150. So, what would be the Capital gain and tax on it?

Solution: As units holding period have crossed 1 year by the time you sell it, so it would be termed as Long-term capital gain.

The cost of acquisition of units will be considered higher of actual cost of acquisition or NAV as on 31.01.2018, thus, in this case, cost price to be considered will be Rs 140

Gain will be Rs 150-140 = Rs 10 Multiplied by 100 units = Rs 1000.

Long-term capital gain Tax will be Rs 100 (10% on Rs 1000)

Now if the actual sale price on 31.03.2018 goes lesser than 140 then you will book long-term capital loss. Though in reality, you are in gain.

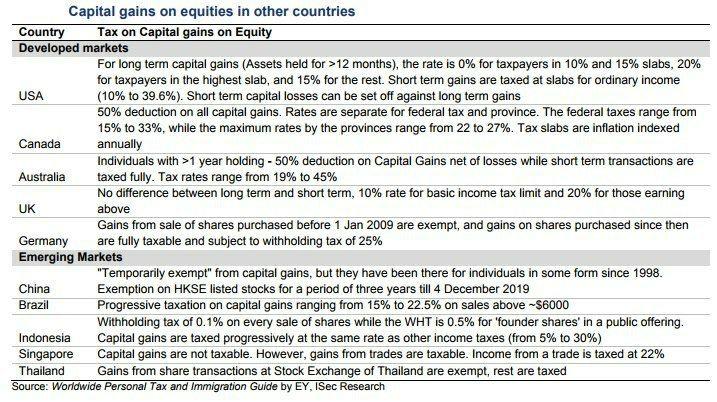

However, this is important for you to know that we in India had been living in the Luxury of No tax on equity. Check out the other countries capital gains tax status

To have details on the tax rates of different countries, you may refer Wikipedia

4. Dividend Distribution Tax on equity Mutual funds has been introduced at 10% of Income distributed. This practically means that all dividends to be paid from equity or equity-oriented balanced funds will be reduced by 10% when received in the hands of investors due to this dividend distribution tax.

Conclusion:

Time to Replan, Review and Rebalance your finances to manage the impact of Budget 2018. Equity has no doubt enjoyed tax-free status for many years and it is difficult for investors to accept this change, but this is also true that even post taxes you will not find equity-like returns in any other asset class. So rather than Panicking, decide wisely.

By the way, besides all this there was the interesting announcement of launching National Health protection scheme which will cover 10 crore poor families (Approximately 50 crore beneficiaries), providing covers of Rs 5 lakh per family per year. This is termed as World’s largest Government funded health care programme.

It will be interesting to see, how government manage the show.

{kind=link}

Well explained Sir. You are always quick and very clear. My take on LTCG is it will give Huge tax collection advantage to the Government. Infact, if Goverment uses this funds wisely during next 5 years we can become DEVELOPED ECONOMY. (we need to move from developing to developed). LTCG tax collection will definitely help to improve our GDP. I also personally feel, it will give more stability and improves fundamentals of stock market which in turn can add 1 to 1.5% extra growth to equity portfolio over long term (7+ years). Bottom line is best use of tax funds and it depends on the Government.

I like your positive attitude Andrew. I concur your thoughts. It’s just the “If” part of the usage of Funds that worries me. One thing is for sure, We are a big and well-connected country and will keep on growing either in a planned way or otherwise 🙂

Investors have been investing in various equity schemes and were accruing better returns keeping the money for longer periods giving less concern of liquidity to the fund managers. Now, I have to pay 10% tax on long term gains. I may hesitate to invest. Will it not affect the capital flow in the market and ultimately scuttle the developmental projects for the paucity of funds.

Thanks for the very nicely explaining the various effects of the budget.

Who will loose in long run if you don’t invest?

Equity is one of the investment asset class. Investors money will move where the growth is. In my view, post-tax long-term return in equities will still remain better than other instruments.