Many people equate the “right investment” with high returns when it comes to investing. They chase performance, jump from one trending asset to another, and rely heavily on past performance or star ratings to make decisions. But is that the right approach?

Rahul approached me two years ago when he had a few investments. He wasn’t aware of any Mutual funds, but seeing euphoria in the market, he wanted to have some exposure. He wanted to have a comfortable portfolio generating FD plus returns. He was quite risk averse when we did his Risk profiling. He got his plan prepared and decided to implement it on his own.

Last week he reached back, to get the portfolio reviewed, which was not the same as the one we recommended. He selected schemes based on the highest past performance, did not consider his risk profile at all, and went with all equity products, and is having almost 60-65% of small cap exposure. He had a few Mutual funds and more direct stocks as he saw on social media channels. Now he is finding himself in a fix, as he wanted to buy a house (which was nowhere in his goal list even when we prepared his plan) and his investment corpus is in losses, with no sign of recovering soon.

So what went wrong here? The quest for right investments, but entered into unsuitable ones, or having a wrong mix of products, or not having clear goals in mind with the right timeline.(Read: What is the Right Time to Start Financial Planning? )

Let’s discuss.

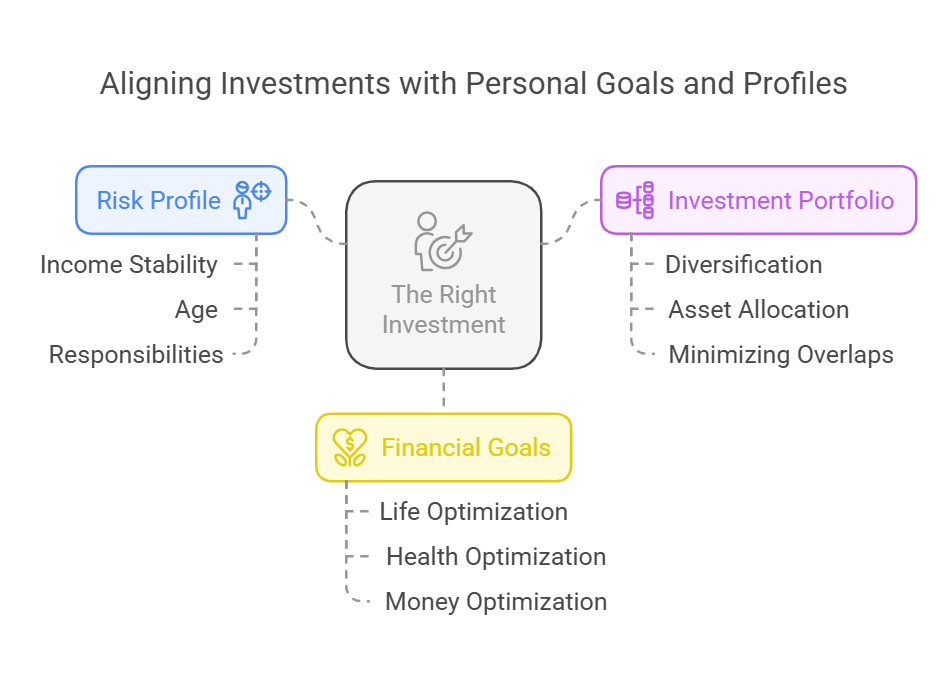

The Right Investment: What Suits You Best

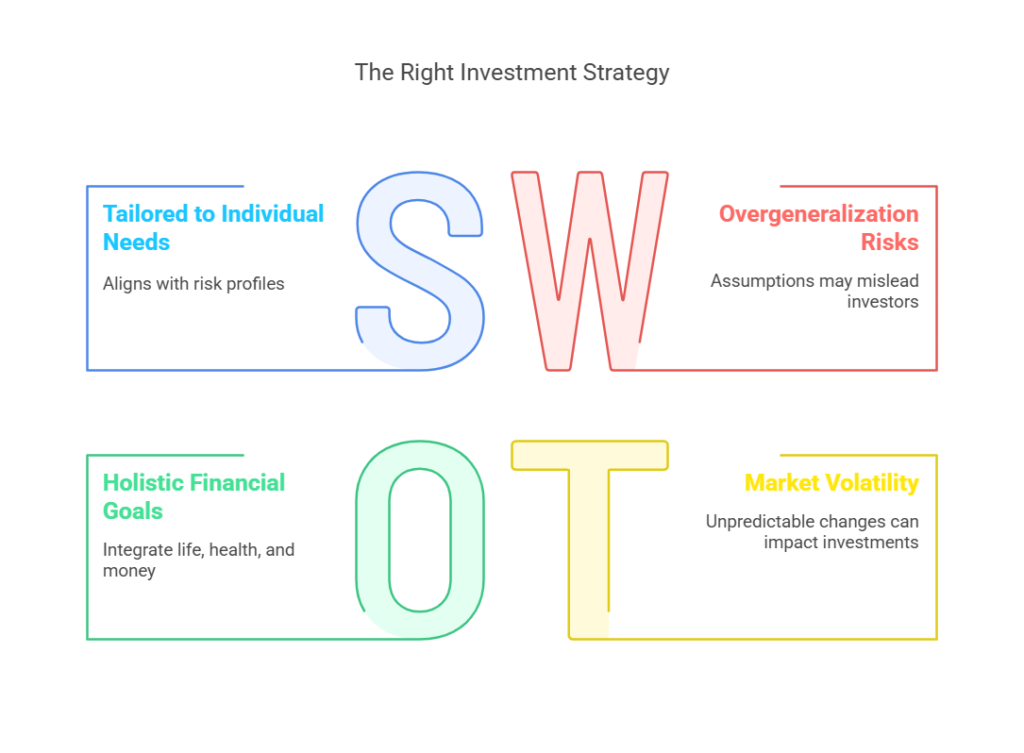

The right investment is not necessarily the one that generates the highest returns—it’s the one that aligns with your risk profile, financial situation, and life goals.

Your risk profile is influenced by various factors: your income stability, age, responsibilities, and overall financial security. A young professional may have a higher risk tolerance and can afford to invest in equity-heavy portfolios, while someone nearing retirement may need to focus on capital preservation.

However, this is a general understanding, which may not be true always. A young man with lots of responsibilities and a conservative upbringing may not have high risk tolerance, and wanted to skip equity products, and on the other side, a retired person may have multiple income sources, and having a stable financial life, and may like to have more equity exposure.

Investments should serve a purpose beyond just making money—they should provide financial security, liquidity, and growth in line with your aspirations. A conservative investor forcing themselves into aggressive investments just for higher returns is like wearing the wrong shoe size—it will eventually lead to discomfort and potential loss. Similarly, when you know nothing about investment management but start mistaking information for knowledge, you’ve essentially boarded a driverless bus.(Read: SIPs: Why Most Investors Fail to Continue ? Common Mistakes to Avoid..)

The Right Portfolio: Beyond Star Ratings

Many investors believe a “good portfolio” is simply a mix of top-rated funds. They look at the latest star ratings and assume that these will continue to perform well. But investing isn’t about picking winners; it’s about creating a strategy that works for you.

A well-constructed portfolio is:

- Diversified across asset classes (equity, debt, gold, etc.), reducing dependence on any single asset’s performance.

- Following an asset allocation strategy that aligns with your goals and risk tolerance.

- Minimizing overlaps, ensuring that you aren’t investing in multiple funds that hold the same stocks.

- Dynamic and reviewed regularly to adapt to changing market conditions and personal financial changes.

The goal should not be to chase returns but to create a portfolio that helps you stay invested with confidence through market cycles.

A simple way to check if your portfolio is well-designed is to see whether all your schemes are performing differently. If they all move up or down at the same pace, something is off.

Yes, I understand that you want all your investments to perform well, but it never happens or should not happen in the short term. Over a longer term, different styles, strategies play their role and your overall portfolio reaches a stage where all or most of the schemes have done well and all are in the same range of average return. (Read:5 ways to review mutual funds investment Portfolio )

The Right Goal: Life, Health, and Money Optimization

Often, the ultimate financial goal is perceived as “making lots of money.” While wealth creation is important, it should not come at the cost of an unbalanced life, stress, or poor health. The right financial goal should be about optimizing life, health, and money together.

- Life Optimization: Money should enable you to live better—not just accumulate wealth for the sake of it. Your investments should align with your aspirations, be it early retirement, world travel, or ensuring quality education for your children.

- Health Optimization: No amount of wealth can compensate for deteriorating health. Investing in health insurance, maintaining an emergency fund, and ensuring work-life balance are just as important as financial investments.

- Money Optimization: Money should be a tool that enhances your life, not something that dictates your every move. Smart financial planning ensures that you are free to pursue your passions, not bound by financial stress.

Sudden unplanned big goals are also very dangerous, which can derail your complete financial wellbeing. Like in the case of Rahul, he had no intention of buying a house 2 years ago, and must have come into mind after seeing a sudden jump in his investments. But by the time he could decide and finalize, the markets fell and the portfolio went into losses. If buying a house was so important, then the investment products selection should have been different. (Read: Financial Planning vs. Wealth Management )

Building Wealth the Right Way: The Right Approach

The right investment is not about chasing the highest returns. The right portfolio is not about picking the best-performing funds. And the right financial goal is not about simply amassing wealth. Instead, financial success comes from a well-thought-out strategy that aligns with your circumstances, aspirations, and long-term stability.

Invest wisely, plan holistically, and optimize for a fulfilling life—not just a bigger bank balance.(Read: )

{kind=link}