Every parent dreams of giving their child the best opportunities in life, especially regarding education. With this goal in mind, they often go to great lengths to secure their child’s future. However, financial decisions can become impulsive when emotions take over, leading to costly mistakes.

Planning for a child’s education requires a rational and practical approach. Not all life goals can be achieved simultaneously, and sometimes, trade-offs are necessary. Prioritizing what truly matters can help parents make better financial choices.

A few months ago, Ramesh, a 38-year-old IT professional, reached out with a concern that many parents share: “My daughter is eight, and I want to ensure that when the time comes for her higher education, finances are not a hurdle. With rising education costs, I feel overwhelmed. What are my best options?” Ramesh aspired to fund her foreign education, estimating a need of $60,000 per year for four years.

Given his income, the goal seemed achievable. But investments aren’t just about income—they depend on how much you can save and invest. Expenses shape lifestyle choices, which, in turn, influence long-term financial security, including retirement. Other major financial commitments, like buying a house, can also impact savings. Striking the right balance requires a well-structured financial plan. (Read | Financial Planning through life stages- How to approach?)

This article explores various investment options for securing a child’s future. While not exhaustive, it provides insights into how different products work and how they can be strategically used. As financial planners, we know that a well-thought-out mix of investments is key to ensuring financial preparedness for parents like Ramesh. Let’s dive into the best options for child education planning.

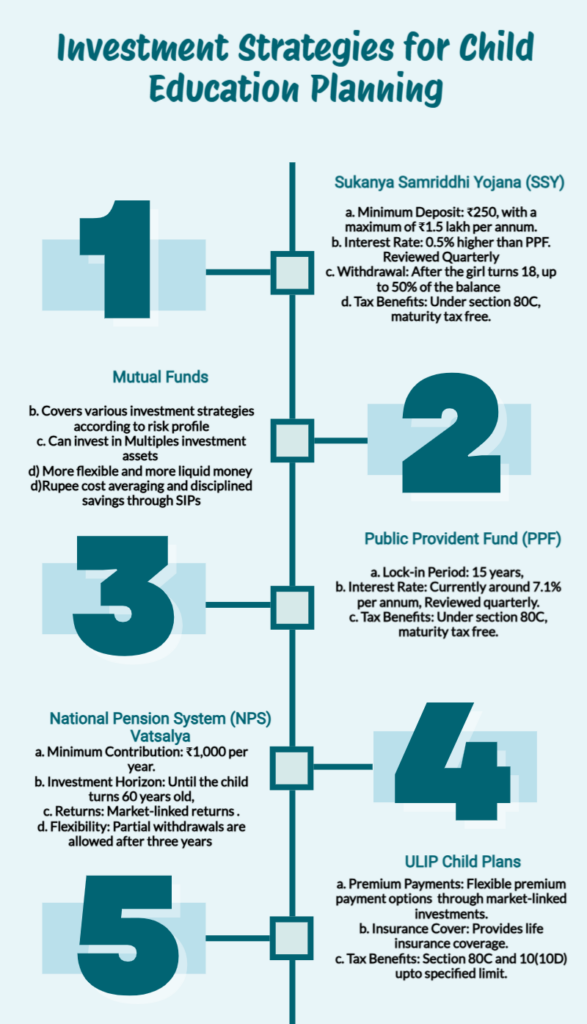

5 Investment options to save for Children Future

- Sukanya Samriddhi Yojana:

This government-guaranteed scheme is meant for Girl Children below 10 years of age. It provides a Fixed interest rate, which is 0.5% higher than the PPF rate, but like other small savings products, the rate also gets reviewed and announced every financial quarter.

The safe, fixed, and guaranteed return makes this a darling instrument among risk-averse investors. And its tax-free nature makes it attractive for all taxpayers.

Our detailed article here will guide you on the product features.

- Public provident fund:

This is the most popular small-saving product for regular investors. Any resident individual can open this for themselves and their children. The tax-free returns with tax benefit u/s 80C made it attractive. So a Girl child can open both Sukanya and PPF. But for Boys, only PPF is available among these two.

You may get to know more about this product from this article.

The drawbacks in the above 2 products are – Long lock-in and low return. However, the tax-free nature of returns makes them a better instrument vis a vis Bonds or Fixed deposits, which have similar kinds of returns but are taxable.

So, for debt allocation of long-term investments, we may consider investing the required money into these instruments.

- Mutual Funds:

For Longer term investments, 7y+ Equity Mutual funds are best instruments, which provide the necessary growth push to the total investments. If you are saving for children’s education, then do remember that the inflation rate in education is quite high which needs your investments to generate higher returns. High returns are not possible in the safe instruments, and generally fixed return instruments are taxable, which reduces the overall return of the investment.

Mutual funds come in different strategies to suit different risk profiles. You may look at the past returns but this is not the right approach to invest. Longer the time frame, you may be required to participate in different volatile periods which will test your patience. So to make the most of your investments, and to be in a disciplined process, it is important to work with a financial plan in place and a professional financial planner to guide you through.

We have multiple articles written on Mutual funds. You may check them here. This will equip you to ask better questions to your planner.

- Children Insurance Plans (ULIPS/Traditional):

Insurance ULIPs provide a fixed structure, where you keep investing up to a certain age and take withdrawal later on in lump sum or spread across various years depending on the requirements. Parents are generally provided with insurance cover, so if something happens to the investor, the savings don’t get hit and the child will get the maturity proceeds as and when they get due.

Child plans are designed to manage the indiscipline that you may show in other open structures. There is a lock-in period before which you are not allowed to redeem. When you are investing in children’s name you are emotionally connected to the product, and never stop investing and neither try to withdraw before the completion of tenure.

The drawback is the same, in a fixed, illiquid structure, you generally get blocked and nothing can be done in case of underperformance. The high associated costs like allocation, management, and administration, with Mortality charges which otherwise you were paying through your term plan, impact further your investment returns. Also, a premium higher than Rs 2.50 lakh per annum, makes your returns taxable.

If you want to get into a fixed return, guaranteed endowment kind of product then keep in mind that the guarantee always returns less than required to beat inflation.

(Also Read: How to safeguard Children’s Future through Proper Financial Planning?)

- NPS Vatsalya:

NPS Vatsalya was announced by the Finance Minister in Budget 2024 and is now very much operational. You can open your Minor Child NPS account under the NPS Vatsalya scheme. To let parents initiate the savings towards kid retirement, they can open NPS Vatsalya and take benefit of low-cost investing managed by the Best fund managers in the industry at a very low cost. It works similarly to NPS. However since it is meant for minor children, 25% of the contribution is allowed for withdrawal for their education or medical needs.

Do remember that this is a very long lock-in (up to 60 years) of age. So Invest only if you are generating enough cash flow surplus after providing savings for your retirement.

Conclusion:

The above-mentioned options are available to all investors, with no minimum investment criteria. You can invest in lumpsum or through monthly mode. You can also do ad-hoc purchases as and when you have a surplus available.

It’s all about making the right investments and keeping children’s education goals as a part of the overall family’s financial plan.

(Explore | Child Future Planning- A Complete and Useful Guide)

{kind=link}