Let’s start the new year by discussing the Most Popular Product of 2021 – The Cryptocurrency.

Cash, bank balances, financial assets (equity, deposits, and mutual fund units), real estate, and precious metals are common forms of money as we know it today. Cryptocurrency or simply crypto is a ‘something new’ that is gaining popularity fast.

‘Something New’ as in it is not an Investment Asset Class, Neither it is a legal tender so can not even call it Money.

There are three basic uses for any currency:

1) It is a means of exchange – the government of the country grants notes and coins the status of legal tender for use in buying and selling goods and services.

2) Currency acts as a store of value – it is not devalued with time (at least it isn’t expected to, but with inflation it does).

3) It is used to keep accounts – you keep track of how much money you own or owe to someone in terms of currency.

As in any other country, the government of India (GoI) defines which currency is legal and which is not. The Reserve Bank of India (RBI) manages the official currency.

Are cryptocurrencies compatible with these criteria? You must have seen some full-page ads and prime-time ads claim they are safe or lucrative but are they? Would we be silly not to ride the crypto wave?

These questions, as well as many more, may come to your mind when you need to invest for the future. Considering that their prices have risen exponentially over the last 2 years – there are currently over 8350 of them – the temptation to “invest” in them is obvious.

A Look at Cryptocurrencies’ Rise and Rise

There has been a huge profit in both dollar and rupee terms in cryptos. Since January 1, 2020, Bitcoin (BTC) has risen by over 555% (5.5x) and Ethereum (ETH) has grown by 290% (29x)!

In December 2021, your “investment” would have been worth close to Rs. 6 lakhs in Bitcoin and a whopping Rs. 31 lakhs in Ethereum if you had invested Rs. 1 lakh on January 1, 2020!

Within the same timeframe, the BSE Sensex rose from 41,306 to 57,011 (38%), while the NSE Nifty rose from 12,182 to 16,985 (39%). Consequently, in the broader Indian stock market, your investment of Rs. 1 lakh on January 1, 2020, would have grown to only about Rs. 1.38 or 1.39 lakhs.

The rise is only half of the story

So, where does that leave us even if we consider cryptocurrencies to be financial assets and not just an alternative to currency? Cryptocurrencies, like any other investment alternative like- equities, ETFs, bonds, etc. are subject to market risks. (Also Read: What is Equity- it is more than just stock market investment?)

A company’s stock represents the intrinsic value of the business’s earnings power and its assets, as well as the overall value of those two things together. In the worst-case scenario, if the company winds up its operations, the shareholders (of direct equity and via MFs) can salvage some money by liquidating the assets.

In Cryptos there is no backup of earnings or assets as a cushion. It’s all demand and supply and pure speculation.

With interest rates at their historic low, the money is coming to stock markets and helping them touch new highs every now and then. The same phenomenon of easy money is working for cryptocurrencies as well.

Cryptocurrencies are only used to park money and speculate, not as a serious investment. Even stable cryptocurrencies can fluctuate in value based on a single news report.

These examples illustrate the volatility of cryptocurrency prices:

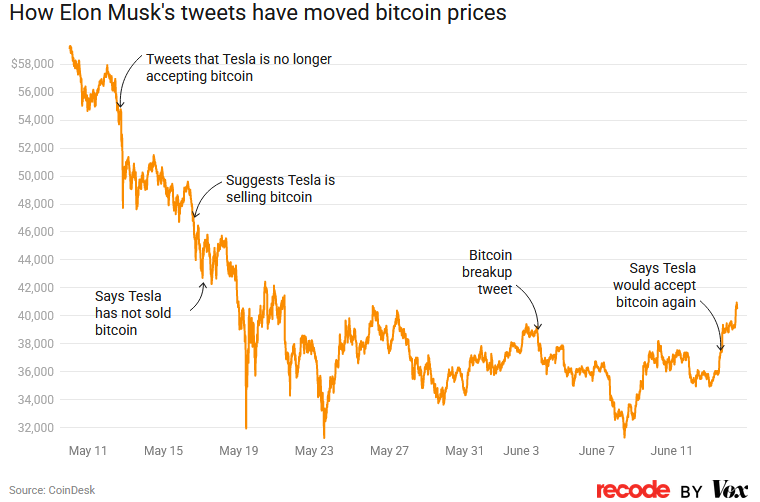

- Tesla Motors CEO Elon Musk tweeted in early 2021 that Tesla will accept BTC for selling its cars, which sparked a surge in interest and rate. VOX’s chart shows how one influencer can move the price since then.

2. The Chinese government banned any activities involving cryptocurrencies – mining, trading, or storing- in 2017. However, a crackdown only began in earnest in July 2021. BTC prices fell by over 8.5 percent after it reiterated its position on September 22, 2021, and other cryptocurrencies took a similar hit. Chinese actions and BTC’s price movement are discussed in this article from Fortune magazine.

To mitigate emotional reactions, equity and bond markets have circuit breakers on either side, contrary to cryptocurrency exchanges. As there are no circuit breakers or regulations for cryptocurrencies, investors have to fend for themselves.

Cryptocurrencies are extremely volatile and offer both the opportunity to make you millions as well as wipe out your entire money.

Cryptocurrencies: The Future of Legal Currencies?

Can Cryptos gain Legal currency status? There is no chance of that happening. At least not anytime soon. Sovereignty gives a country the right to print its own currency and control its monetary supply. A central bank (like the RBI) is responsible for this. The control of the money supply gives a government the ability to tax, penalize, and give benefits to its citizens.

If decentralized and unregulated cryptocurrencies become legal tender, governments would lose their ability to tax and subsidize people. This is something no government ever wants.

Cryptocurrencies have another aspect, namely their so-called untraceability, similar to cash, and speed of transactions, which is similar to electronic money. These two characteristics make cryptocurrencies the principal source of funding for terrorism and drug trafficking. Such activities and their funding would be forbidden by any government, resulting in the use of cryptocurrencies being controlled or regulated.

Furthermore, even if cryptocurrencies become acceptable as money, then their use as investments would diminish and the valuations would plummet. For a better understanding of the phenomenon, consider keeping INR or USD in cash in your locker in the hope that its value will rise over time. This is simply not plausible, since the currency is only one of the ways to do so, and it is not an efficient one either.

Are all Cryptocurrencies the same?

All cryptocurrencies – around 8300+ of them – seem to be similar, safe, and secure, but are they? No, they are not.

Credibility

Cryptocurrencies issued by well-known organizations, such as Facebook’s (now Meta) Diem or Libra, may be considered relatively secure and safer. It is also true that an established currency such as Bitcoin or Ethereum is a better investment than an ICO (initial coin offering) – just like a company with years of public history is a better investment than an IPO.

Market Volatility and Stability

Stablecoins (which reduce volatile price movements by holding physical assets) are somewhat stable cryptocurrencies. Third-party custodians maintain the physical asset with full audits and disclosures. The reserve asset of a stablecoin may be fiat currency (such as USD or EUR), or gold.

Hacking and Theft

Many crypto exchanges and wallet apps have been hacked. Recently, BitMart was hacked and $150 million worth of cryptocurrency was stolen. In the year 2021 alone, investors lost at least $10 million in hacking and digital theft incidents. Comparatively, bank robbers in the USA in 2020 netted just $5,000 per physical bank robbery!

Risks Also Arise From Offline Storage

You might consider storing your Crypto assets in an offline cold wallet, protected with a password and everything. This, too, poses some issues. The CEO of a foreign crypto exchange died in Jaipur, India in 2019, leaving behind close to Rs. 1,000 crores in crypto-assets that were “safe” in his cold wallet. The money is lost forever due to the encryption.

What is the Intrinsic Value of Cryptocurrency?

Throughout human history, any currency has had one of three intrinsic values:

- It had intrinsic value, just like gold or silver, and even if the government officially prohibited its use as currency, it could still be used in other ways.

- It was backed by the reserves of a precious metal whose intrinsic value was quite high – the gold standard.

- There was government backing for it as legal tender – for a few days even after the Rs. 500 and Rs. 1,000 notes were demonetized, the old notes could be exchanged at banks and used to pay for essential goods and services.

Cryptocurrencies do not possess these values, and they will not either (with the exception of a few stablecoins). Cryptocurrencies were created specifically as a currency that would not be affected by inflation. The investor frenzy has rendered that theory obsolete.

Payment technology or investment alternative?

Cryptocurrencies were born from blockchain technology, which provides a mechanism for constructing the currency as well as a platform for transactions. So, should you look at it as an investment alternative or as a transactional platform?

Competition

The primary reason for the popularity of Bitcoin was its finite supply, ensuring long-term stability, and its complex mining algorithms. Now, the intense competition makes it unviable as an investment as well as a currency.

Since it is becoming increasingly affordable to create a new cryptocurrency, there is no limit to how many can be produced. Even though an individual currency may have limited supply, if there are many of them, then the logic gets reversed.

Technology Obsolescence

Today, blockchain is seen as a panacea for all FinTech problems, and everyone wants a piece of this pie. With new technology arriving every couple of years, it is impossible to predict which new technology might disrupt blockchain. Quantum computing is the most promising of them all, and when it gets here the need for blockchains will disappear altogether!

Popular Adoption

Anything that is widely used for trading goods and services by the general public gains acceptance as a currency. Even though El Salvador has recognized Bitcoin as legal tender since September 2021, and many other countries are in the same situation, cryptocurrencies are not widely adopted by the general public.

Cryptocurrency is far more complex to transact than cash or new-age solutions like UPI. Most parts of the world are lacking reliable connections and internet access, as well as financial infrastructure to support them. While crypto-exchanges and giants like PayPal have made it easier to trade in them, most people are still just trading in a speculative asset.

India’s Stand on Cryptocurrency:

An RBI advisory issued in early 2013 warned people against trading in cryptocurrencies, and in 2018, the RBI banned any platform from accessing formal financial channels to invest or trade in cryptocurrencies. As a result, all crypto assets were frozen and their prices plummeted.

Eventually, the Indian Supreme Court lifted the ban in March 2020, just in time for the governments to fight the demand shock caused by lockdowns with easy money policies. Crypto exchanges that had lain dormant took advantage of the opportunity and rode the tidal wave.

“Banning of Cryptocurrencies & Regulation of Official Digital Currency Bill, 2019” is a new draft bill on cryptocurrencies that have been submitted to the parliament for debate and approval. India’s government and regulators are preparing to take the China-way – to outlaw private cryptocurrencies and create an official cryptocurrency backed by rupees.

In the draft bill, the ban is proposed based on a risk assessment, including:

- It could be used to launder money and evade taxes.

- Possibly used in terror/insurgency funding, drug/human trafficking, and other illegal trades.

- Volatility and cybercrime pose risks to investors and consumers.

- Technical infrastructure and expertise are insufficient to cope with rapidly changing technologies due to inadequacies in disclosures.

- A threat to the country’s financial stability and sovereignty.

In the bill, it is proposed to:

- Within Indian jurisdiction, any private cryptocurrency shall not be mined, held, sold, traded, issued, disposed of, or used.

- All of the above activities are punishable by fines and imprisonment of up to 10 years.

- Set up a formal financial structure to minimize the risk of instability.

- To permit the use of the technology for the purpose of teaching, research, and experimentation.

- Consider cryptocurrencies as commodities, with SEBI in charge of regulating them.

- Introduce a legal tender cryptocurrency, which is governed by the Reserve Bank of India.

- Notifying an officially issued cryptocurrency of another country that it is eligible for forex trading with the official cryptocurrency of India.

As soon as the bill becomes law, anyone holding cryptocurrencies must declare and dispose of all of them within 90 days.

Even when the RBI launches an official cryptocurrency it will be safe to use as a medium of exchange rather than as an asset class.

What next?

The most obvious question that comes to mind is: Are there better investments than cryptocurrencies?

Yes, if you consider cryptocurrencies as investments at all.

Despite the fact that history does not repeat itself, it certainly rhymes. The Dutch were crazy about a perishable commodity in the 17th century – the tulip bulbs. In the aftermath of the tulip mania, the price of tulips skyrocketed, and their popularity exploded overnight. Tulip bulbs were neither an asset class nor a form of currency for the masses to invest in. Yet people went crazy over them.

Despite the low-interest rates, and most fixed-income instruments are returning negative returns in real terms, central banks are raising or about to raise their base rates as inflation concerns heat up. Lenders in India, led by the SBI, have already begun raising their deposit rates. It’s possible that you’ll get inflation-adjusted returns sooner than later. (Also Read: What is inflation and how it impacts your financial plan?)

Savings schemes such as NPS, PPF, and other long-term fixed-income instruments still have advantages due to tax savings and almost three times the interest rate of savings accounts. (Also Read: All you wanted to know about New Pension Scheme.)

Investment in the stocks of great companies for the long term is one of the best ways to compound your wealth over time. With mutual funds, you can still be a part of India and the global growth story even if you’re not a great stock picker like Buffet or Jhunjhunwala. Participating in stocks through SIPs is still the best way to compensate for periodic booms and busts. (Read: All you wanted to know about SIP in mutual funds)

In the End…

We do not recommend that you disturb your financial plan in order to enjoy the “thrill” of betting on cryptocurrencies. You should use only a small part of the money you would spend on a vacation or a party to try your “luck” in cryptocurrencies. It’s all about luck, not your skills. (Read: Luck or Skill- what matters in your success?)

Consider hiring a financial planner who can help you chart your financial goals, their importance, and most importantly, your ability to cover any risks involved. Don’t put your hard-earned money at risk by investing in something as volatile as spirit.

{kind=link}