Employee Provident Fund (EPF) is generally the First Investment product that you encounter when you start your Financial journey. This is a compulsory saving where your Investment doubles the same month since the employer also contributes the same amount 🙂

As you can’t do much about it and its automatic deduction from your salary, most people do not care about this. It is only when you Shift the job, Retire or need some money for some big expense or the mandatory deduction starts bothering you, that you start looking for answers, and try to learn more about this product.

Rachit, one of my Client’s Son, who recently started his employment journey, came to me with the question on EPF. Thus I thought of writing a detailed article on this subject for all those who have questions about this.

This is the first article of a four-article series on the Employee Provident Fund (EPF) basics. This would help a new employee who had recently joined the workforce and wanted to understand how EPF works and the various rules and regulations governing it. Also, we will try to address some of the basic queries raised by the EPF investors.

Previously, we have also written a series of articles on other employer-provided retirement benefits like- the National Pension Scheme (NPS), Superannuation fund, etc. for a better understanding of these avenues. This time, we have come up with the EPF scheme, which is the most popular employer-provided benefit that a majority of the employees have in their investment portfolio. (Read: What is Superannuation Fund and how is it different from NPS?)

What is Employee Provident Fund (EPF)?

Employee Provident Fund (EPF) is a social security scheme allowing salaried individuals to save and invest for their retirement and other major milestones in life. It is managed by the Employee Provident Fund Organization (EPFO), in accordance with the Employee Provident Funds and Miscellaneous Provisions Act of 1952 (or simply the EPF Act).

The EPFO is a statutory but non-constitutional organization with the mandate to encourage employees of industries and the private sector to invest for their future, particularly retirement. With the backing of the Central Government, and tax sops available, EPF is quite popular.

Here are some stunning facts about the Employee Provident Fund that would help you understand its importance:

- It is one of the world’s largest social security schemes by the number of accounts at 24.77 crores (Annual Report 2019-20) and the number of transactions.

- The number of contributing members is close to 6.4 crores and more than 73-lakh pensioners were benefitting from it.

- More than 7 lakh organizations are contribution establishments with the EPFO.

- As India’s largest Non-Banking Financial organization, EPFO manages over Rs.16.6 trillion (~ USD 239 billion) as of March 2019 which was roughly 8.3% of the GDP.

- It is one of the few EEE [Exempt-Exempt-Exempt] schemes available in India.

- As the interest and final amount are both tax-free, EPF performs better than other debt instruments.

Over the years, its stellar performance and safety have encouraged employees to actively demand their organizations participate in the scheme.

Who Manages Employee Provident Fund?

There is a tri-partite central board called the Central Board of Trustees (CBT) that manages the Employee Provident Fund. It consists of the representatives from the Central Government, all State governments, employers, and employees through their unions.

The CBT manages three schemes under its umbrella with the help of a statutory body called the Employee Provident Fund Organization (EPFO). These schemes include a contributory provident fund (the EPF), a pension scheme (the EPS), and an insurance scheme (EDLIS) for the employees in the organized sector.

These schemes were started as a result of long-drawn deliberations, to accommodate the changing work environment and lifestyle needs of the subscribers. The monthly contributions that are deducted from the employees’ salaries, as well as the contributions from their employers, are deposited into:

- Employee Provident Fund Scheme started in 1952.

- Employee Deposit Linked Insurance Scheme started in 1976.

- Employee Pension Scheme started in 1995.

The EPF

The EPF includes contributions from both the employee and the employer. Sometimes, the Central Government may also contribute to the corpus to support either the employees, the employers, or both to tide over challenging times. The most recent example is when the government announced amid the COVID-19 lockdowns to contribute both employees’ as well as employers’ contributions towards EPF for three months.

Both employees and employers are required to contribute to this scheme every month. For the contributions made towards EPF, an employee can claim tax deductions while filing their Income Tax Return (ITR) u/s 80C of the Income Tax Act. While the employers can claim their part of the contribution as a deductible expense in the P&L account. (Read: Income tax Deductions List- Useful for your Tax Planning)

One of the biggest attractions of the EPF is that the employee can get a lump sum amount within two months of unemployment or upon retirement. It is completely up to the employee to invest it in an annuity or not.

In this regard, EPF is different from the National Pension Scheme (NPS) in that in the latter, at least 40% part of the corpus received on retirement must be invested in a pension plan to get the regular income in the form of annuities. (Also Read: NPS withdrawal rules)

The EPS

The Employee Pension Scheme was started in the year 1995 as a defined-benefit pension scheme. It provides the members of the EPFO a retirement pension as well as offers survivorship coverage for their families.

A major part of the employer’s contribution, 8.33% out of their contribution of 12% of the basic salary (subject to an upper limit of Rs.15,000), goes towards the EPS. The Central Government also contributes 1.16% of the basic monthly salary to the EPS for the benefit of those employees whose basic salary is less than Rs.15,000.

The following formula is used to calculate a member’s pension under EPS:

A member is eligible to get a monthly pension under the following circumstances:

- Upon permanent disablement while in service.

- Retirement or superannuation.

- If the member dies the spouse and up to two children (up to 25 years of age) can receive the pension.

- In case the surviving spouse remarries or dies before the children attain the age of 25 years, they would still get the pension till that age.

- Disabled children are eligible to get a lifetime pension.

- In the absence of a family, a nominee would receive a pension.

- Dependent parent(s) would get the pension when there is no family and no nominee.

As you can see that the social security coverage of the EPS is quite wide.

Even in case, if you leave the service, after six months of joining but before 10 years of service, you can withdraw the EPS corpus.

The EDLIS

The Employee Deposit Linked Insurance Scheme is another social security program helping the beneficiaries of deceased members. As the awareness about having life insurance is abysmally low in India, and more so among the economically weaker sections, the EDLIS offers its members the security against any eventuality.

With the EDLIS, the government ensures that the dependents of a member of the EPFO are not left without any financial support after they pass away. Upon the death of the employee, this group term insurance plan pays a benefit of Rs.6,00,000 to the nominee.

The best part is that the cost of the insurance is borne by the employers over and above their 12% contributions towards the EPF and EPS. In many cases, if the employer offers a better group life insurance cover, then they may opt-out of the EDLIS.

Benefits of Employee Provident Fund

Like any social security scheme, the EPF also has many benefits. But the structure of this scheme makes it one of a kind in the world where employees belonging to the lowest economic strata can get maximum benefits from a little discipline.

1. Safe Returns

Being a debt instrument, it is not as volatile as an equity-backed scheme. Moreover, the sovereign backing of the Central Government makes it one of the safest investments in the country. (Also Read: Safe investment options in India- with Government backing)

2. Friendly Tax Treatment

The EPF falls into the category of an EEE or Exempt-Exempt-Exempt instrument.

The contributions are deductible u/s 80C, the interest accrued is tax-free, and the maturity proceeds are tax-free as well. Therefore, in the case of EPF, you get unhindered and a very long runway to let compounding work for you. (Also Read: Investments and Expenses eligible for deduction under section 80C)

3. High-Interest Rates

Recently on 3rd June 2022, the Central Government notified the 8.1% for the FY 2021-22. This is a reduction from the 8.5% from earlier and the lowest rate in over four decades. But, even after the rate cut, amidst the low-interest rate regime, it is the best among all debt instruments.

There are two reasons for that:

- These days, the fixed deposit in the SBI gives a maximum return of 5.5% p.a. Even when you compare these rates with PPF, another government-backed provident fund, they are at 7.1%.

- As the returns on EPF are tax-free, your comparison should be with post-tax returns from other instruments. These returns are dependent on your tax bracket and to earn a post-tax interest of 8.1% your nominal rate must be:

- At 10% tax slab you must get 9% pre-tax returns.

- At 20% tax slab you must get 10.12% pre-tax returns.

- At 30% tax slab you must get 11.57% pre-tax returns.

4. Allows Partial Withdrawals

Unlike, other provident fund schemes, EPF allows partial and pre-mature withdrawals (check out the section on Withdrawals from EPF). You can also take out a loan at nominal rates with your EPF as collateral.

5. Minimum Pension

The meagre contributions towards the EPS sometimes created weird situations where a retired member got a pension of only a few hundred rupees. To overcome this, the EPFO mandated giving a minimum pension of Rs.1,000 per month.

In 2022, even this sum is being revised and it is proposed to increase the minimum pension to Rs.2,000 per month. This would benefit at least 40 lakh members with the central government bearing an annual additional cost of around Rs.1,000 crores.

Also Check- Online & Offline Process to transfer EPF account from old company to new company

Historic Rate of Interests for Employee Provident Fund

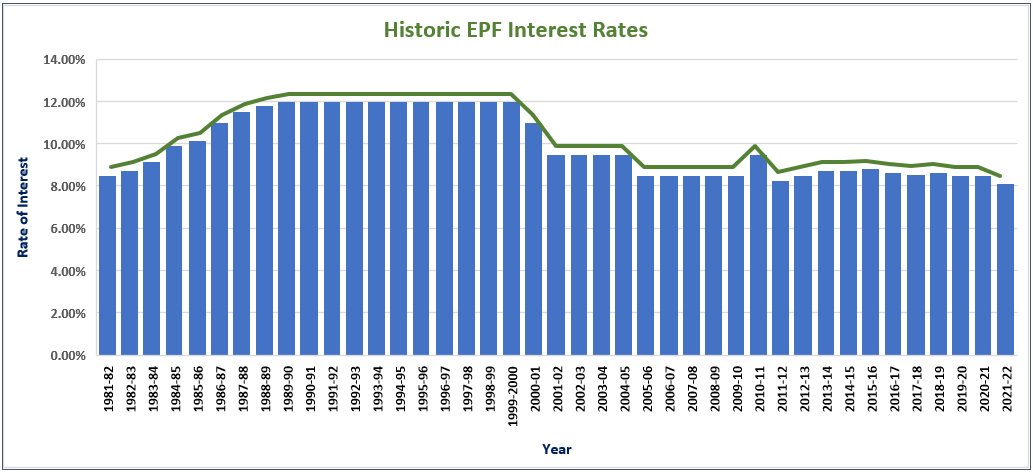

Historically, the interest rates on EPF have moved in tandem with the overall scenario of inflation and benchmark rates. The following chart shows this perfectly:

You can see that in the late Eighties when the inflation was high, the rate of interest was also high going up to 12% p.a., and since then it has gradually come down to the present at 8.1%. The Ministry of Labour proposes a rate of interest for each financial year, in March/April each year. The Ministry of Finance then approves it for being ratified by the cabinet and adopted by the EPFO.

Who Can Join Provident Fund?

The EPF being a regulated and state-sponsored scheme is not open to everyone. According to the EPFO, only an employer can make its employees a member by opening an EPF account on their behalf. Unlike NPS, it cannot be opened and operated in an individual capacity. (Also Read: All you wanted to know about NPS)

Any employer with 20 or more permanent employees, at any level, department, or even location, in more than 180 industries, must mandatorily register with the EPFO. Such employers are mandated to open the EPF accounts of their employees and make regular contributions towards their EPF, EPS, and EDLIS accounts as well as bear some administrative charges.

There are certain categories of employers, who are exempted from opening the mandatory EPF accounts for their permanent employees. But they can also opt-in this facility for employee motivation and benefits.

The most important point here is a broad definition of the term “employee” by the EPF act. It states that:

An “employee” means any person who is employed for wages in any kind of work, manual or otherwise, in or in connection with the work of an establishment, and who gets his wages directly or indirectly from the employer, and includes any person employed by or through a contractor in or in connection with the work of the establishment. It also includes persons engaged as an apprentice, but not under the Apprentices Act of 1961.

How are Monthly Contributions Calculated and Invested?

When an employee is registered in the EPF scheme by their employers, they are automatically enrolled in the linked EPS and EDLIS schemes.

The monthly employee share of provident fund contributions and that of their employer towards EPF, EPS, and EDLIS are calculated on the sum of the following:

- Basic Salary

- Dearness Allowance (DA) (including the cash value of any food concessions to employees)

- Retaining Allowance (RA), if applicable

The total of these forms the basis for computing the contribution value. The employee share of contributions to provident fund is 12% of the total of the salary components mentioned above. The employer matches this contribution and bears the administrative and other charges. In addition, the central government also contributes 1.16% of the sum towards the EPS for those employees whose basic salary is up to Rs.15,000.

The contributions of the employee and the employers are split differently and go towards the designated scheme in a pre-defined ratio.

The breakdown is as follows:

- The entire 12% contribution from the employee goes towards the EPF.

- The employer’s contribution is divided into the following heads:

- 3.67% of salary into EPF.

- 8.33% of salary into EPS, subject to a ceiling of Rs.15,000/month salary or Rs.1,250.

- 0.5% of salary into EDLIS.

- 0.85% for EPF administrative charges

- 0.01% for EDLIS administrative charges

If the monthly salary of an employee exceeds Rs.15,000, then the division of employer’s contribution is divided as follows:

- 8.33% of Rs. 15,000 or Rs. 1,250 goes to the EPS account.

- The balance amount – 8.33% *(Salary – 15,000) – goes to the EPF account.

This distribution helps the employees to amass as much corpus as possible while their immediate insurance needs and long-term pension needs are met by the employer as well as the government.

If the salary of the employee exceeds Rs 15,000, then the employer can opt for one of the two methods for contribution:

- They can restrict their contribution to 12% of the basic salary and DA; or

- They can match the contribution of the employee.

In case both the employers and employees are willing to contribute at a higher rate than the minimum mandatory (12% of Rs.15,000/month salary), then they must submit a joint proposal to the EPFO. The responsibility of paying the administrative charges for the higher contribution must be borne by the employers.

Also Check- How to Download and Read the EPF e-passbook?

Taxation Rules on EPF Contributions above Rs.2.50 Lakhs

From Financial Year 2021-22, if the employee’s annual contribution to EPF exceeds Rs.2.50 lakhs for the non-government employees and Rs.5 Lakhs for the government employees, the interest on the extra amount would be fully taxable. However, all contributions made by the employer or employee up to 31st March 2021 would continue to remain tax-exempt.

From 1st April 2021, if your contribution exceeds the aforesaid limits, it would be divided into two parts- non-taxable contribution and taxable contribution and interest would be computed separately on both these components to gauge the tax liability.

The interest on the taxable portion of your contribution would be added to your total income and taxed as per the income-tax slab rates applicable. (Also Read: old or new income tax slab rates- what to choose?)

For instance, if your annual contribution to EPF for FY 2021-22 is Rs.5.50 Lakhs and you are a non-government employee, interest on the excess contribution above Rs.2.50 Lakhs, i.e., Rs.3 Lakhs would be taxable and the balance would be tax-free.

If you are a government employee, interest on the excess contribution above Rs.5 Lakhs, i.e., Rs.50,000 would be taxable and the balance would be tax-free.

Further, a TDS of 10% is applicable on the taxable portion of the interest on the date of credit to the same. In the absence of PAN, the TDS rate would be 20%, and for NRIs, it would be 30%, subject to the provisions of DTAA. It is also applicable on the final settlement (from the taxable portion) even in the case of the death of the employee. This is clarified in detail in this EPFO Circular.

The Universal Account Number

Since October 1, 2014, the Universal Account Number or the UAN is allotted to each member who becomes a subscriber of the EPFO. This is a 12-digit unique number and does not change even if the member changes jobs.

The UAN acts as an umbrella ID mapping multiple member IDs that are allotted by different organizations where an individual may work over their lifetime. It also helps the member to check their balance and transactions across all member IDs, update passbooks (online/offline), make claims, apply for withdrawals, and even complete the KYC requirements.

Starting 2016-17, to popularize the use and adoption of UAN, the EPFO also announced the refund of and=ministrative charges.

Any member can generate their UAN on the EPFO website simply by logging in. As soon as the details like mobile number and email ID are mapped against the UAN, you will receive details such as EPF balance via SMS on the registered mobile number.

The process of registering/generating UAN is as follows:

- Activate your UAN-based registration.

- Enter your UAN, mobile number, and member ID(s).

- Get a one-time PIN and submit.

- UAN credentials are then verified.

- Create a strong password.

The UAN becomes your user ID for logging into the portal for subsequent usage.

Also Check- 5 important EPF Rules you should know

Withdrawals from EPF

The Employee Provident Fund is meant to be a retirement vehicle. To become eligible for a pension, a subscriber needs to contribute continuously to his PF account for at least 10 years, but if the account is closed prematurely, the subscriber may no longer get that benefit.

If too much flexibility is given during the accumulation phase, it will be abused. This will hurt the individual’s retirement phase. However, under the following circumstances, one can apply for withdrawal from their EPF account:

- Medical Treatment

Medical treatment of self, spouse, children, and dependent parents. There is no mandatory lock-in period or minimum service period for it. But you can withdraw up to 6 times your basic salary for the treatment of specified diseases. (Also Read: Would your financial plan survive critical illness?)

- Home Loan Repayment

For repayment of outstanding home loans, the member can withdraw up to 36 months’ basic salary. One must have at least 10 years of complete service, before such withdrawal. This facility can be availed only once. (Also Read: When should you foreclose your home loan?)

- Marriage

After at least 7 years of service, one can withdraw up to 50% of the corpus for their own, sibling’s, or children’s marriage. This can be done only three times in the lifetime of the member. You must submit the relevant proof.

- Home reconstruction and Renovation

For reconstructing or renovating a house, one can withdraw up to 12 times their monthly salary if they have completed at least 5 years of total service. You can avail of this benefit only once.

- Home Constructions or Purchase

For once in a lifetime, a member can apply for withdrawal of their EPF corpus up to 36 times their monthly basic salary for constructing or purchasing a house. They must have completed at least 5 years of total service. If they are only purchasing a plot, then the sum is capped at 24 times their monthly salary.

In a special scheme, if the employee is a member of a registered housing society having at least 10 members, he/she can withdraw up to 90% of the accumulated EPF corpus for the purpose of down-payment of a house and pay EMIs as well. (How prepared are you for a new home purchase?)

- Unemployment

Finally, in case of unemployment for over one month, a member can withdraw up to 75% of their funds. While, in case of being unemployed for more than two months, they can withdraw the balance of 25% too.

In cases of female members resigning from the establishment to get married, the two-month waiting period will not apply.

- Retirement

Upon retirement, the member can withdraw up to 90% of the EPF balance.

It is important to keep in mind that EPF withdrawal before 5 years is completely taxable and all previously availed tax benefits on the same shall be reversed. It is also subject to a TDS of 10% if the amount withdrawn is more than Rs.50,000. In the absence of PAN, the TDS rate is 30%.

(Read a detailed article of EPF Withdrawal rules here)

Conclusion

In most cases, Employee Provident Fund, or EPF is the first investment someone does after joining the workforce. It’s a mandatory savings plan that generates a safe and fixed return. The Exempt-Exempt-Exempt (EEE) structure makes it even more attractive.

It is one of the best instruments out there for planning your long-term goals, especially retirement. (Also Read: Why Retirement Planning should be your most important financial goal?)

Although it comes with a lock-in but the flexibility to withdraw funds for certain specified purposes provides the necessary liquidity. However, it doesn’t mean that whenever you require money, you would dip into your EPF corpus. It is one of the very big financial blunders you can make which you may have to regret later.

You should do proper planning for all the financial goals and allocate different instruments for the same, like- home purchase, marriage, education, etc. and keep sufficient emergency funds and insurances in place to tackle any unforeseen events in life, like- critical illness, job loss, etc. You should consider premature EPF withdrawal as a last resort only in case of emergencies when you cannot figure out any other way to arrange for it.

In the next article in the EPF basics series, we would be answering some of the basic queries on EPF “How-tos” for the EPF investors, especially the new entrants. Keep watching this space. Click Here to Read this article.

is the first investment done by employees. Safety, fixed return, EEE structure makes it attractive. Tax Rules.){kind=link}