Rahul Mishra, an IT professional in the USA, requested his father to send him some money to help him buy a house. His father told him that the money to be transferred would be taxable and the bank will deduct some TCS (Tax collected at source) from it.

It was news to Rahul, and he was shocked to hear that how come transactions between Father-Son be taxable.

The 3 letter word always creates fear in the mind of people. Even if you do not have any income, you may be scared of this. Yes, I am talking about “TAX”.

Rahul, called me to confirm the same and I clarified that TCS does not make the transaction taxable. The Indian Government last year announced TCS on all foreign remittances under the Liberalised Remittance Scheme (LRS).

This way the government just wants to ensure tax compliance and keep track of foreign remittances.

You may claim the refund by filing ITR if you don’t have taxable income in India. This TCS is applicable on the amount over and above Rs 7 lakh.

Now TCS, like TDS is something which again many would like to avoid, as they are not sure when they will get the refund, moreover would like to avoid the operational hassles.

So I suggested a way around that he may tell his father to transfer money in his NRO account and he can then transfer it to NRE and repatriate the money. (Read: Bank accounts for NRIs)

In this case, too, he has to submit forms 15ca and 15cb to the Bank and confirm that the money you are about to repatriate is tax paid. So the Transaction has to be genuine and has to be Post-tax. Also advised him to keep his CA Informed on what they are doing and why.

Once again the Tax fear got over his mind and he felt that by filling any such form he kind of would be in a soup and Income tax guys may bother him in the future.

So, now I have to elaborate on Rahul on form 15ca and 15cb, to dispel that scare.

When a resident individual makes any payment to a non-resident, he has to follow certain compliances. Section 195 of the Income Tax Act mandates that the deduction of the applicable income tax (TDS) by the resident individual himself, on any payment made to a non-resident Indian (NRI) or a foreign company. (Read: TDS on NRI Investments)

For this, he needs to furnish an undertaking in form 15ca, containing various details about the payment made. In certain high-value transactions, a certificate issued by a Chartered Accountant is also required.

Form 15ca and 15cb are also required to be submitted to the bank when an NRI repatriates the money to the resident country from the NRO account or even when he/she transfers money from NRO to the NRE account. (Also Read: Taxation of NRE FD for returning NRIs)

Since NRO money is taxable in India, coming from taxable sources, this process will ensure that the taxes have been paid on the money to be transferred.

What is Form 15ca and 15cb?

Form 15ca:

Form 15ca is a declaration made by the Resident Individual while making any payment to a non-resident wherein it is stated that he has deducted applicable tax at source from the foreign remittance so made. (Read: Who is an NRI?)

The basic idea is to make sure that the tax is deducted on time, at the source itself which may not be possible after the payment is made to the non-resident. Also, it can serve as a tool for the income tax department to track foreign transactions.

The resident individual can e-file form 15ca and can submit it online.

Sections of Form 15ca:

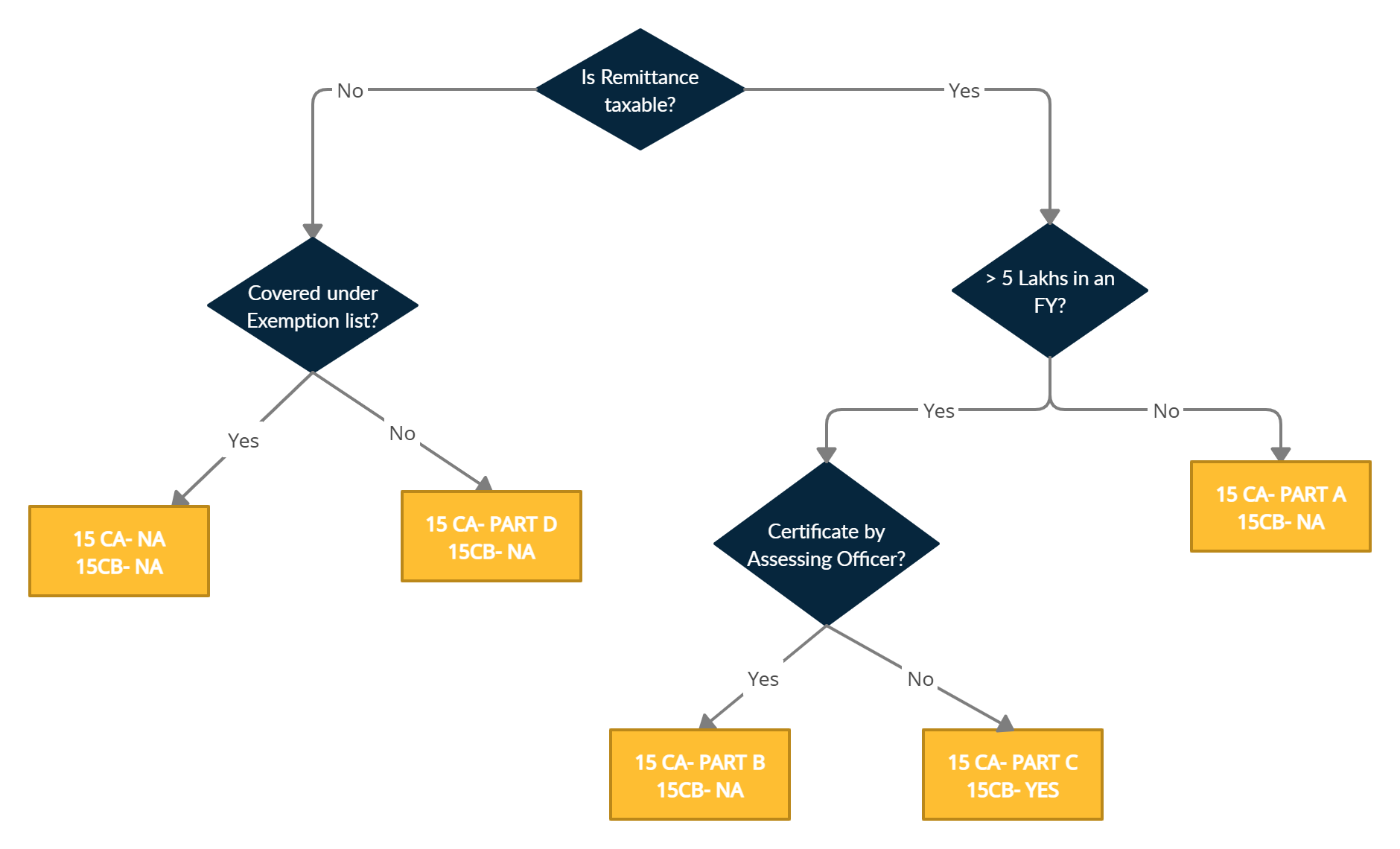

Form 15ca consists of the following four parts, applicable in different situations for payment made to non-resident individuals or a foreign company :

- PART-A: When the remittance (or aggregate of remittances) does not exceed Rs. 5 Lakhs and is chargeable to tax, during a particular Financial Year.

- PART-B: When the remittance exceeds Rs. 5 lakhs, but an order/certificate is obtained by the Assessing Officer to deduct no TDS or at a lower rate.

- PART-C: When the remittance (or aggregate of remittances) is taxable and exceeds Rs. 5 Lakhs, during a particular Financial Year.

- PART-D: Where the remittance is not chargeable to tax as per the provisions of Income-tax Act, other than those mentioned in rule 37BB (As explained in the further sections of this article)

You may download the latest version of Form 15ca from here.

Form 15cb:

Form 15cb is a certificate issued by a Chartered Accountant after examining that all the provisions of the Income Tax Act and Double Tax Avoidance Agreement (DTAA) are duly complied with if the value of the transaction(s) incurred during an FY is more than Rs. 5 Lakhs. (Read about DTAA in detail in this article)

The CA certifies that the TDS deduction and the rate at which TDS is deducted is as per section 195 of the income tax act and the nature and purpose of remittance are legitimate. It is mandatory to upload form 15cb before filling Part C of form 15ca.

You may download the latest form 15cb from here

Applicability of Form 15ca and Form 15cb:

The below flowchart describes the applicability of Form 15ca & 15cb under different circumstances:

Please note that in the case of NRO to NRE transfer there is no such limit of Rs. 5 lakh. NRI has to file form 15CA and CB both to their bank while making any transfer of any amount.

Non-requirement to File Form 15ca and Form 15cb:

In the following situations, the resident individual is not required to furnish forms 15ca & 15cb:

- The payment is made by an individual and it doesn’t require any prior approval from RBI under the Liberalised Remittance Scheme.

- The payments of specified nature listed in Rule 37BB, listed below:

- Investments abroad in:

- Equity Shares

- Debt Securities

- Real Estate

- Branches and wholly- owned Subsidiary companies

- Subsidiary or Associate companies

- Loans extended to Non-Residents

- Advance Payments/ settlement of invoice against imports

- Imports for diplomatic missions

- Imports below Rs. 5 lakhs (for use by ECD offices)

- Intermediary trade

- Payment for Operating Expenses of Indian Shipping Companies & Airlines operating abroad.

- Booking of passages abroad -Airlines companies

- Remittance towards Business Travel

- Travel under Basic Travel Quota

- Travel for- pilgrimage, medical treatment, or education (including fees, hostel expenses)

- Postal Services

- Construction of projects abroad by Indian companies including import of goods at project site

- Freight insurance – relating to import and export of goods

- Payments for maintenance of offices abroad

- Remittances by foreign embassies in India

- Remittance by non-residents towards family maintenance and savings

- Remittance towards personal gifts and donations

- Remittance towards donations to religious and charitable institutions, other Governments & Government charitable institutions abroad

- Contributions or donations by the Government to international institutions

- Remittance towards payment or refund of taxes

- Refunds or rebates or reduction in invoice value on account of exports

- Payments by residents for international bidding.

In most of the cases above, TCS has become applicable, on an amount above Rs 7 lakh.

How to file form 15ca online?

To e-file form 15ca you need to login to the income tax e-filing portal with the PAN and Password (if you are already registered on the portal), if not then you have to first register yourself by clicking on the ‘Register’ button and providing all the details asked.

Next, you have to click on the e-file option, from the drop-down select the “Prepare and submit the online form (other than ITR)” option and then select Form 15ca from the subsequent dropdown.

Fill and Submit the same with details required in the relevant fields upon selecting the appropriate part of the form as per the nature of the payment to be made. (you may refer to the section above on Form 15ca parts.)

Also Check: Common Financial Planning mistakes by NRIs and how to rectify those?

What are the consequences of not filing form 15ca / cb, if required?

If you are required to submit form 15ca, or form 15ca and form 15cb, as the case may be and fail to furnish the same, or submit it with incorrect or inadequate information, then you might be held liable under section 271-I of the Income-tax Act and the assessing officer may impose a penalty of Rs. 1 Lakh.

Can a filled form 15ca & form 15cb be cancelled or withdrawn?

Yes, a filled form 15ca and form 15cb can be withdrawn within 7 days of submission. In case there are some changes or updations you want to make in the form, you have to withdraw the previous form and submit a new one with the updated information. But after 7 days, you would not be allowed to withdraw the submitted form 15ca or 15cb.

In the end:

Catching NRIs for tax evasion is a difficult task. So, NRIs are subject to TDS in all their earnings in India. And deduction of TDS is something which the payer has to comply with.

NRO account receives Indian originated incomes like Interest, dividend, rent, etc., and most of the Incomes these days are taxable in nature.

Most of the Incomes paid to NRIs are already tax deducted, but still to be doubly sure on the part of NRIs too, confirming their self-assessment and before the money gets repatriated government ask for Form 15ca and 15cb both from them while transferring any money from NRO to NRE account.

Form 15ca is a declaration made by the payer and 15cb is the authentication by CA of that Payment.

This article on Form 15CA and 15CB is written by Mr. Varun Baid, CFP

{kind=link}