Pension space in India is changing very fast. With NPS getting popular day by day, and people getting sensitize towards retirement savings, Insurance companies are sensing opportunities.

Not only Insurance companies even Mutual fund space has different product offerings, directed towards retirement.

Retirement is not only about accumulation of corpus, but also about pension /annuity or generating monthly income.

When pension has to come from Government, no one is concerned about safety, low interest. Even the taxation does not bother, but when it comes to selecting the pension product on your own, that is the time when retirees prefer to get into some guaranteed kind of flow to feel more secure.

And when the word Guaranteed is attached to the product, it’s natural to gain attention.

HDFC life insurance has come up with such a product with name HDFC Life Pension Guaranteed Plan.

On the face of it, this is a normal Immediate annuity and deferred annuity plan but the word “guarantee” calls to review this plan.

(Read: Retirement Plan or Pension Plan, What to chose?)

HDFC Life Pension Guaranteed Plan – In Brief

HDFC Life Pension Guaranteed Plan is a single premium immediate annuity plan which can be bought on single or joint life and with or without the return of purchase price.

It has a deferred annuity variant also, where one may invest the money today and start receiving pension or annuity after the deferment period which can go a maximum of up to 10 years.

In HDFC life pension guaranteed plan, the guarantee comes in the annuity rates. The annuity rates i.e. the rate at which one will get the fixed pension is predefined and guaranteed by the insurer. This applies even to the deferred annuity variant.

In the case of immediate annuity products, this is normal to have a fixed and guaranteed rate, but in the case of deferred annuity products, this is the first of its kind product which is giving a guarantee in advance at the time of Investment.

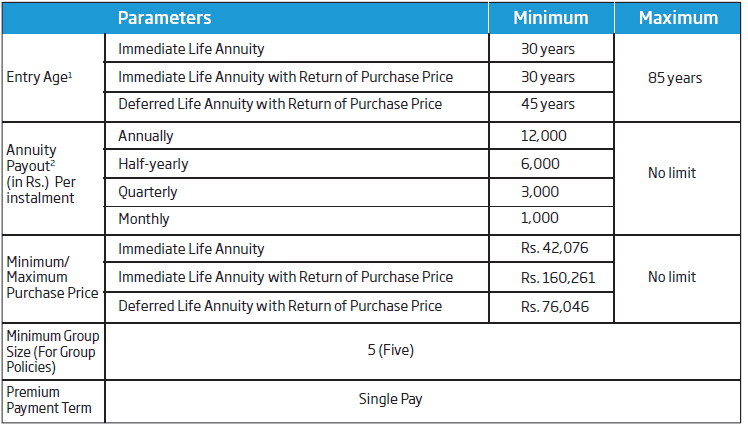

HDFC Life Pension Guaranteed Plan – Eligibility features

HDFC Life Pension Guaranteed Plan – How it works?

Immediate annuity (Single Life)

You invest the money and will start receiving the pension/annuity as per the frequency is chosen while investing. The frequency of receiving a pension can be Monthly/quarterly/half Yearly or Yearly. This will continue as long as the annuitant is alive.

Immediate annuity (Joint Life)

In a Joint Life annuity, the secondary annuitant can be the spouse/child/parent/parent-in-law or sibling of the primary annuitant. Other relationships may be considered as long as there is an insurable interest between the annuitants.

In the case of an immediate annuity in Joint life, you invest the money and keep receiving the annuity till you are alive after you, the second annuitant will receive the annuity till he/she is alive.

In both the above options, the invested price will not be returned

Immediate Annuity with Return of Purchase price (Single Life)

You invest the money and start receiving the pension as per the frequency is chosen. After your death, the invested money (Purchase Price) will be returned to the nominee and the policy terminates.

Immediate Annuity with Return of Purchase price (Joint Life)

You invest the money and start getting the pension, after you, the second annuitant will keep getting the pension. And post death of both the annuitants the purchase price (Invested money) will be returned to the Nominee and policy terminates

Deferred Annuity with Return of Purchase Price (Single Life)

You invest the money and choose the deferment period. It is the period after which you want to start with the pension. The pension rates are Guaranteed at the time of investments.

The deferment period may be between 1 to 10 years

After the deferment period, the annuitant will start receiving the pension till he/she is alive and after that, the Purchase price will be returned to the nominee.

Deferred Annuity with Return of Purchase Price (Joint Life)

You invest the money and choose the deferment period. Once the deferment period is over, the pension will start as per the frequency is chosen, post the first annuitant demise the second annuitant will keep receiving the pension. After the death of both the annuitants, the purchase price will be paid back to the nominee

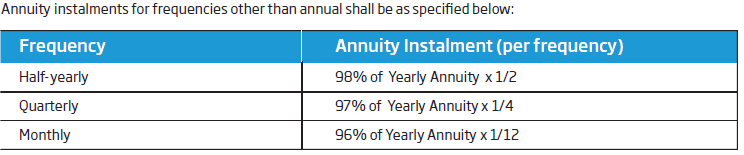

How the annuity will be calculated?

Annuity payments = Applicable Annuity rates* Purchase Price

Now, in the case of an immediate annuity, it is very clear that annuity rates are the rates which you are getting on your Investment (Purchase Price). This will be the rate which you may want to compare with other available instruments to decide on the suitability of the scheme.

For e.g. In FD you are getting 6.75%; in POMIS at 7.5%

Some may want to compare it with other high-end products like Perpetual bonds

But in the case of a deferred annuity, the working is bit different. The rate of annuity is guaranteed at the time of investment and pension will start after the deferment period which may be 1 to 10 years. What about the Interest during the deferment period? Here is the catch. You will not earn anything during this deferment period.

Let’s understand this with an example:

Assuming you are 50 years of age and want to invest in HDFC life Pension Guaranteed Plan. Since you want to secure your retirement years which is due after 10 years so you chose the deferred annuity plan, looking at the attractive annuity rates @ 11.98%

(Download the annuity rates of HDFC Life pension guaranteed plan)

You invest Rs 10 lakh in this plan and after 10 years you will start getting Rs 119800/- per annum as an annuity for your lifetime. But this is after 10 years.

The catch here is that you will not earn anything during this deferment period.

Whereas if you Invest Rs 10 lakh in a suitable product, for e.g. a balanced mutual fund which is expected to generate at least 8% p.a. on a post-tax basis, then these 10 lakhs would become Rs 21.58 lakh, and getting Rs 119800 on Rs 21.58 lakh means 5.55% rate of return.

Falling into the guarantee trap you will lose the Opportunity cost of your investment.

Now, if you look at the annuity rates in the age of 60 for Immediate annuity options then these are 6.36% for the return of purchase price option and 7.90% for No return of purchase price.

(Also Read: How to manage Post Retirement Income flow – Bucketing strategy)

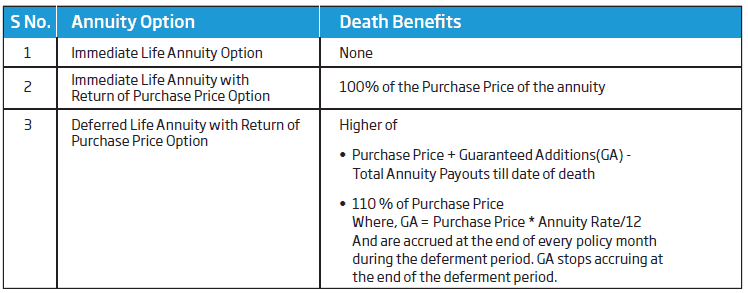

HDFC life pension Guaranteed plan – Death benefits

If the annuitant dies during the continuity of the plan, then this is how the death benefit will be paid to the nominee

HDFC Life Pension Guaranteed Plan – Should you Invest?

The main advantage of Immediate annuity products is that they guarantee the rate of Interest for a lifetime, which will ensure the continuity of a specific and fixed cash flow after Retirement.

Also, these products are not to be ignored for New Pension Scheme Investors, as they have to compulsorily put their NPS maturity money into such plans and opt for a lifetime pension. (Also Read: LIC Jeevan Akshay VI – Worth Considering)

The only thing that you may compare in immediate annuity insurance plans is the rate of interest, and that too only at the time of investment as these rates also keep varying with time.

In the HDFC Life Pension Guaranteed plan, the immediate annuity product is simple and comparable, but the deferred annuity with guaranteed high rates is looking like a kind of trap to me.

The rates are looking high on the face of it, but the zero interest in the deferment period takes away all the attraction from this as in the end, you may be at par with the immediate annuity investors.

Even the Immediate annuity thing in today’s scenario is not looking that attractive as we are in the rising interest rates scenario. Thus, we may see better rates in bank FDs, Post office schemes, and other fixed-income securities, in the next 2-3 years. All are taxable instruments just like an Immediate Annuity. So, locking money for long-term in a rising rate scenario does not look sense to me.

Yes, when in the future if we find ourselves at some better rates, they may like to block some of the corpus into the high yielding instruments, but not now.

{kind=link}

I am looking for best pension plans right now

There is nothing called Best, the product which suits you is best for you and to know which products would suit you a holistic look at your finances is required, preparing a financial plan considering your risk profile, financial goals, present investments, etc.

Also, our advice would be- rather than going for pension plans, you should focus on good Retirement Planning. You may consult a Financial Planner for the same.