Credit cards are Easy Money, and any easy money option tends to get exploited. But if used wisely this instrument is not that bad. It’s just we either fear them too much or don’t respect them enough, and misuse to the fullest. Today, I want to have a real conversation with you about what actually happens to your credit score when you start collecting those shiny pieces of plastic.

You see, I’ve sat across enough clients to know that nearly everyone has questions on Credit Cards. Those who don’t have cards, ask if they should get one? Or how to get one? Those who have, they ask “How many cards are too many?” “Will another card hurt my score?” “Why did my score drop when I got that new rewards card?” ( Read: Your Investments Reflect Your Life: Learn from Mistakes and Rebuild Smarter )

I will focus on the latter by cutting through the noise and talking straight about how multiple credit cards really affect your financial health.

First things first – your credit score isn’t some mysterious number that randomly goes up and down. It’s actually responding very logically to how you handle credit.

Think of it like a responsible friend who watches how you manage your money. Every time you get a new card, make a payment, or carry forward a balance, your score notices.

Here’s what you need to understand: more cards can actually help your score if you’re smart about it. I’ve seen clients strategically use multiple cards to build impressive credit profiles. But I’ve also seen people dig themselves into deep holes by misunderstanding how this works. The difference always comes down to knowing the rules of the game.

Let me share something personal from my practice. Just last month, a young professional came to me frustrated because her credit score dropped after getting a second card. She thought she was being responsible – always paying on time, never carrying balances.

What she didn’t realize was that by using 80% of her first card’s limit every month (even while paying it off), she was signaling to lenders that she might be overextended. We fixed this by spreading her spending across both cards and keeping each one below 30% usage. Three months later? Her score jumped 45 points.

This brings me to the most important point about multiple cards – it’s not about how many you have, but how you use them. I’ve got clients with five cards who have perfect 850 scores, and others with two cards who can’t get above 650. The difference always comes down to three things: paying on time every single month, keeping balances low, and not applying for too much new credit at once.

Now, I know what some of you are thinking – “But what about all those travel points and cash-back offers?” But remember no amount of airline miles is worth damaging your credit score. Better to check out your usage, and the benefits you will actually use which these cards are pitching you for.

If you’re considering another card, ask yourself these questions first: Can I remember all the payment due dates? Will I use this card enough to justify any fees? Does this fit with my overall financial picture? Because here’s something they don’t tell you in those flashy credit card commercials – every new card is another responsibility, another potential pitfall if you’re not careful. (Read: What is CIBIL Credit score?)

Let me break down exactly what happens to your credit score when you hold multiple cards and how to optimize your strategy.

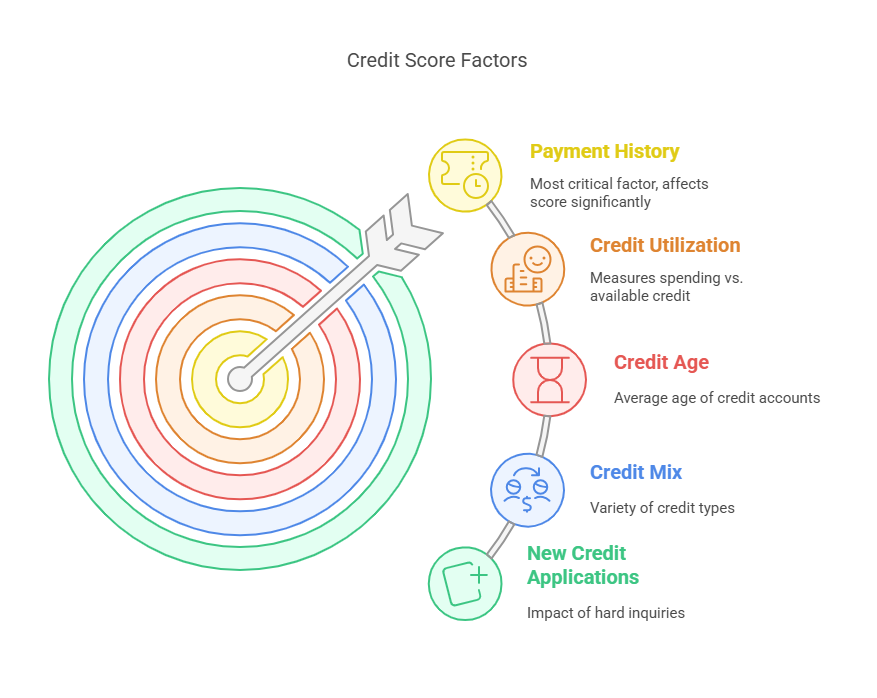

1. Payment History (35% of your score)

This is the most critical factor in your credit score. Every credit card you add creates another payment deadline you must meet.

What you need to know:

Missing just one payment on any card – even if you’re perfect with others – can drop your score by 50-100 points

Late payments stay on your report for 7 years, though their impact lessens over time

Lenders view payment history as the best predictor of future behavior

Pro Tip: Set up auto-pay for at least the minimum payment on all cards as a safety net. Better yet, pay the full balance to avoid interest charges, and further damage to your Credit score.

2. Credit Utilization (30% of your score)

This measures how much of your available credit you’re using.

Key insights:

More cards increase your total credit limit, which can help utilization

However, maxing out even one card hurts you – lenders look at both overall and per-card utilization

The ideal range: Below 30% on individual cards and below 15% overall

Example: If you have 3 cards with ₹1 lakh limits each (₹3L total):

Spending ₹90K (30% of total) is okay

But spending ₹90K on just one card (90% utilization) is bad, even if others are unused

3. New Credit Applications (10% of your score)

Each application triggers a hard inquiry that temporarily hits your score.

Important details:

Hard inquiries typically cause a 5–10-point drop and stay for 2 years

Multiple applications in a short period signal risk to lenders

Some issuers will deny applications if you’ve opened too many accounts recently

Strategy: Space out applications by at least 6 months, and only apply when you genuinely need the card. (Read :5 Financial Skills Every Woman Must Master for a Secure Future)

4. Credit Age (15% of your score)

This considers the average age of all your accounts.

What matters most:

Older accounts improve your average credit age

New cards lower your average age immediately

Closing your oldest card can significantly reduce your credit history

Smart move: Keep your first credit card open forever, even if you rarely use it.

5. Credit Mix (10% of your score)

Lenders like to see different types of credit.

The reality:

Credit cards alone don’t provide much mix benefit

Having 2-3 cards plus an installment loan (like a personal or auto loan) is ideal

Don’t take loans just for credit mix – only borrow when you truly need to

The Right Number of Cards for You

| Credit Profile | Ideal | Why |

| Building credit | 1 secured card | Establishes history with minimal risk |

| Average user | 2 cards | Provides backup + rewards optimization |

| Frequent traveler | 3 cards | Allows category spending (airline, hotel, daily) |

| Rewards optimizer (if you are a high user) | 3-4 cards | Maximizes cashback/points across categories |

5 Golden Rules for Multiple Cards

Never miss a payment

Set phone reminders for due dates, though lenders also do their job of reminding.

(Somewhere I also read that some apps encourage card users to use their platforms to manage all credit cards at a single place, but I am wary of this, as their idea is to keep pitching you the ways to use the card through their platform, by offering discounts, vouchers etc. and with all this you may end up going overboard your cards)

Watch individual card utilization

If one card’s balance creeps up, redistribute spending

Consider prepaying before the statement date

Keep accounts active

Make small purchases every 3 months to avoid inactivity closures

Set up recurring subscriptions on rarely-used cards

Avoid fee traps

Calculate if rewards outweigh annual fees. Some cards encourage you to convert your purchase to EMIs and you get some 2x-3x rewards points. Whereas every reward point equals 0.25 paise worth, and the interest you pay for this EMI may be higher than the rewards worth.

Downgrade premium cards to no-fee versions if not in use

Monitor reports regularly

Check all 4 bureaus (CIBIL, Experian, Equifax, CRIF). It is mandate on each agency to provide one FREE report per person every year.

Dispute errors immediately – they can take months to resolve

The Bottom Line

Having Multiple credit cards do impact your credit score, but how it impacts depend on your Usage. Following guidelines as mentioned above, and restricting the total usage by paying the bills timely will help in improving your score then damaging it. (Read : Peer to Peer Lending – A New age way to Borrow or Invest? Should you?)

But let me be clear – I’m not saying multiple cards are bad. In fact, when used right, they can be powerful tools. I have one client who uses three cards strategically: one for all her business expenses, one for personal purchases, and one just for recurring bills. This system keeps her organized, her utilization low, and her credit score in the 800s.

The bottom line? Multiple credit cards are like power tools – incredibly useful in the right hands, but dangerous if you don’t know what you’re doing. Your credit score will respond based on how wisely you manage them. Pay everything on time, keep those balances low, and don’t go applying for every card with a good sign-up bonus. Do that, and you’ll find that having multiple cards can actually work in your favor.

Remember, in the world of credit, slow and steady wins the race. It’s not about how many cards you can get, but how well you can manage the ones you have. That’s the real secret to building and maintaining great credit. (Read : Should NRIs Keep or Close Their Indian Bank Accounts and Investments?)

{kind=link}