Last few months have been quite eventful for Mutual Fund Industry. SEBI being a regulator keep on suggesting changes into the funds’ structure, but this time even Finance Ministry has not spared the sector.

There have been 5 important changes announced and even implemented in Mutual fund investments space. Some changes are structural, some have resulted in more transparency with more disclosures, and the major one is on taxation.

This article is to apprise you about those changes, to help you make informed decisions

Important changes in Mutual funds in 2018

-

Long-term capital gain taxation on Equity Mutual funds.

From April 1, 2018, Long-term capital gains on Equity investments be it mutual funds or Equity shares would be subject to 10% tax.

Equity Investments comes into long-term category after 1 year of holding. Before 1 year it is a Short-term investment and attract a short-term capital gain tax of 15%.

Since this is a big but recent change and that too on investments which used to be tax-free, so considered to be a big jolt to investors.

Thus, to console the Investors, Concept of Grandfathering on the value as on 01.02.2018 was introduced, which means the cost price to calculate LTCG on equity will be considered as the actual purchase price or the value as on 01.02.2018, whichever is higher.

-

Dividend distribution tax on Equity Mutual funds.

Not only Long-term capital gain, even the dividend declared by Equity Mutual funds will be subject to Dividend distribution tax w.e.f 01.04.2018.

This means that though dividend from Equity mutual funds will be tax free in the hands of the investor but will be subjected to 10% DDT, at the fund house level and investors will get 10% of dividend lesser than what they would have got if there was no dividend distribution tax.

This was done to ensure that fund house/ Investors should not misuse the dividend way to avoid long-term capital gains tax.

However, it is important to note that this DDT is only in case of Mutual funds. In Equity shares, there is no tax on dividends received till Rs 10 lakh in a financial year.

-

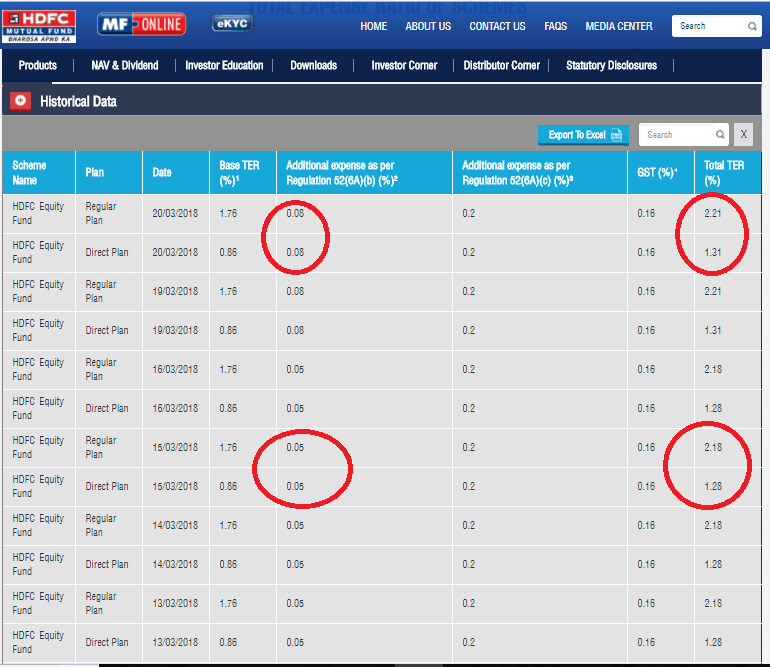

Disclosures on TER

Total Expense ratio or TER are recurring expenses charged to a Mutual fund scheme. It comprises of the asset management fee, distributors’ commission, registrar’s fee, trustee fee and other expenses allowed to be charged to a scheme. These are expressed as a percentage of assets managed.

This TER is a kind of the cost to the Investors for investing in Mutual funds.

Though these costs are under strict regulation of SEBI, and AMCs can charge a maximum of 3% on Equity Mutual funds, but still, there are times when AMCs play with these TERs to suit markets or their marketing, but within limits, as prescribed.

To help investors track the changes in TERs and to increase transparency in costs, SEBI has mandated AMCs to disclose the actual TERs on daily basis on their websites. (Ref: SEBI Circular number SEBI/HO/IMD/DF2/CIR/P/2018/18 Dt. Feb 05,2018)

Also, whenever there is a change in the TER, AMCs are required to inform the investors of the scheme through Email or SMS, at least 3 days prior to the change. This is applicable since March 1, 2018.

Below is the Table showing HDFC Equity TER for the past few days, in the format as prescribed by SEBI.

Explanation of the expense breakup:

4. Benchmarking with Total Return Index

Though most of the investors have a tendency to compare the Returns of Mutual funds with other schemes or past returns, AMCs and Trustees are required to have an appropriate benchmark aligned with Investment Objective of the scheme to compare the performance of the scheme and also put on the scheme related documents.

At present, most of the mutual fund schemes (other than debt schemes) are benchmarked to the Price Return variant of an Index (PRI).

PRI only captures capital gains of the index constituents and does not account for the dividend/interest that are generated from the basket of the constituents.

Whereas in their scheme portfolio they add up the dividend/Interest of the securities, due to which it looks as if Fund managers are generating Alpha or outperforming the benchmark.

So, now to increase the transparency in the performance of schemes, SEBI through its circular SEBI/HO/IMD/DF3/CIR/P/2018/04, dated Jan 4, 2018, mandated schemes to have a benchmark as TRI (Total Return Index).

Unlike PRI, Total Return variant of an Index (TRI) takes into account all dividends/ interest payments that are generated from the basket of constituents that make up the index in addition to the capital gains.

Hence, TRI is more appropriate as a benchmark to compare the performance of mutual fund schemes.

This circular is applicable to all schemes from Feb 1, 2018.

5. Rationalization and Categorization of Mutual funds schemes

This is one of the biggest change in Mutual fund space, which may directly impact your investments too as this may result in complete overhauling of the portfolio or merging of schemes.

SEBI wants investor of the Mutual fund to be able to evaluate the options available and make an informed decision before making any investment.

So, it is important to have a clearly distinct asset allocation, structure and Investment strategy in all the schemes.

One should be clearly able to identify the structure of the scheme, which should not be overlapped with any other scheme of the same fund house.

With this desire in mind, SEBI has decided to standardize the scheme categories and characteristics of each category. And Fund houses are required to make changes in their product portfolios and get them approved by SEBI.

SEBI has broadly classified schemes as –

Equity / Debt/ Hybrid / Solution-Oriented schemes / Other schemes.

In each category above, SEBI has suggested specific Type of schemes., with a specific structure

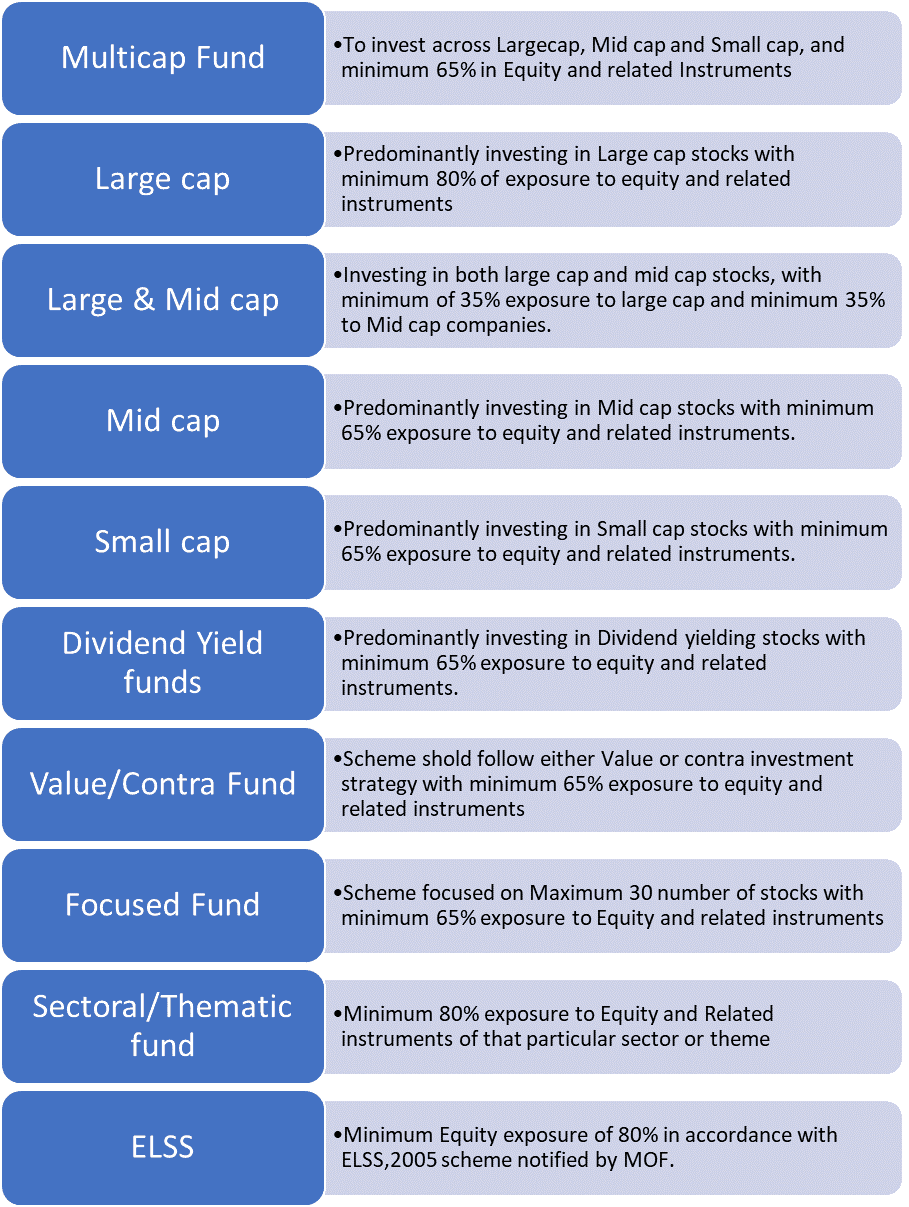

Categorization and Structure in Equity Funds

The Interesting point here is that Only one scheme per category would be permitted.

So, now fund houses cannot have 2 funds (with different names) having the same characteristics. Means one fund house cannot have 2 large caps, 2 Mid-caps and so on.

This is not all, to ensure uniformity in the investment universe, now SEBI has clearly defined the Large Cap, Midcap and Small cap stocks to be taken in a Mutual fund’s portfolio. As follows:

- Large Cap – the 1st-100th company in terms of full market capitalization

- Mid-cap – the 101st-250th company in terms of full market capitalization

- Small-cap – 251st company onwards in terms of full market capitalization

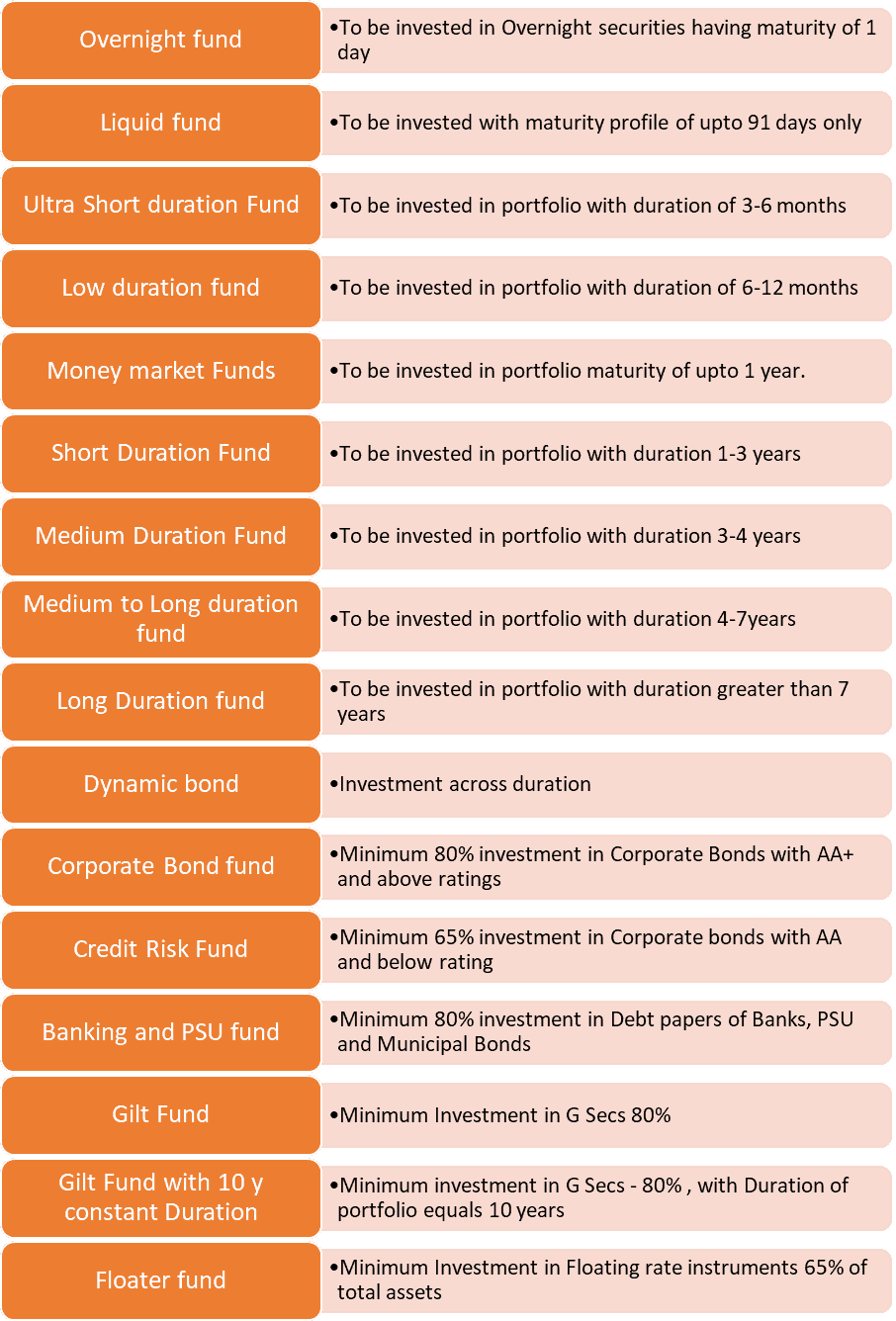

Categorization and Structure in Debt Funds

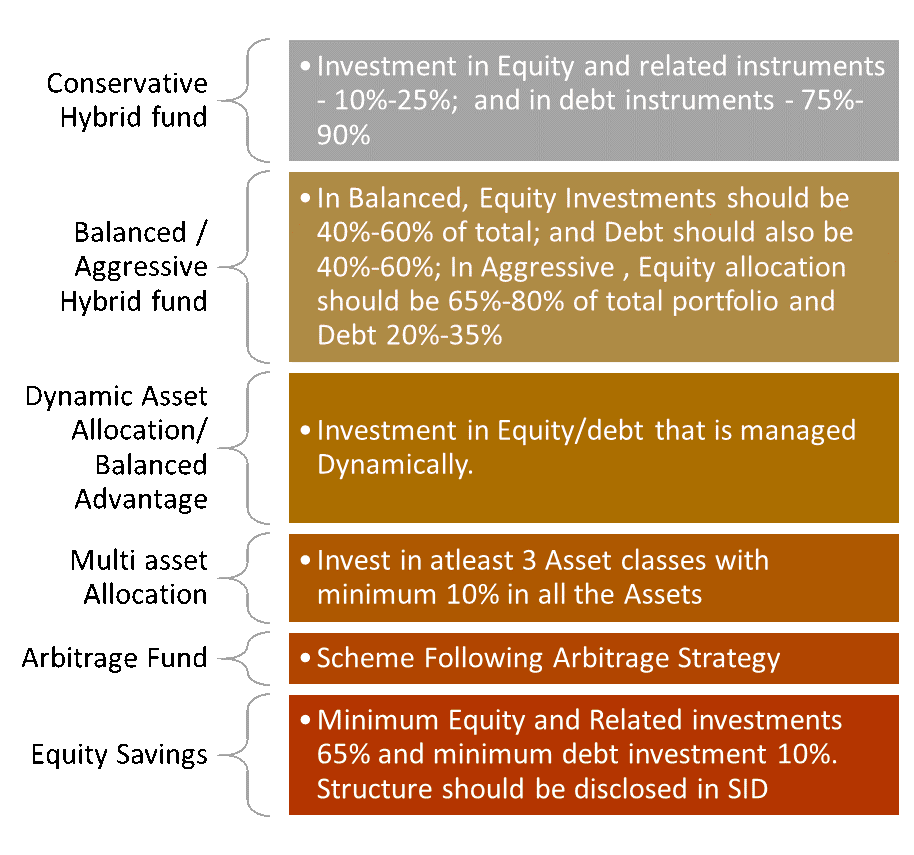

Categorization and Structure in Hybrid Funds

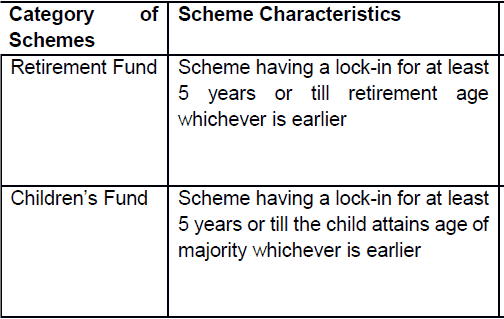

Categorization and Structure in Solution-Oriented Schemes

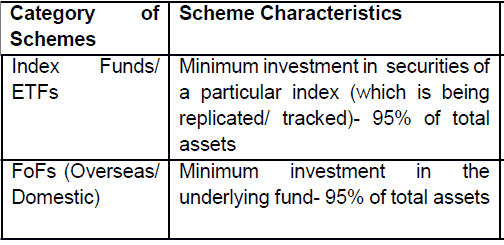

Categorization and Structure in Other schemes

SEBI has mandated all AMCs to submit their proposals by December 15, 2017.

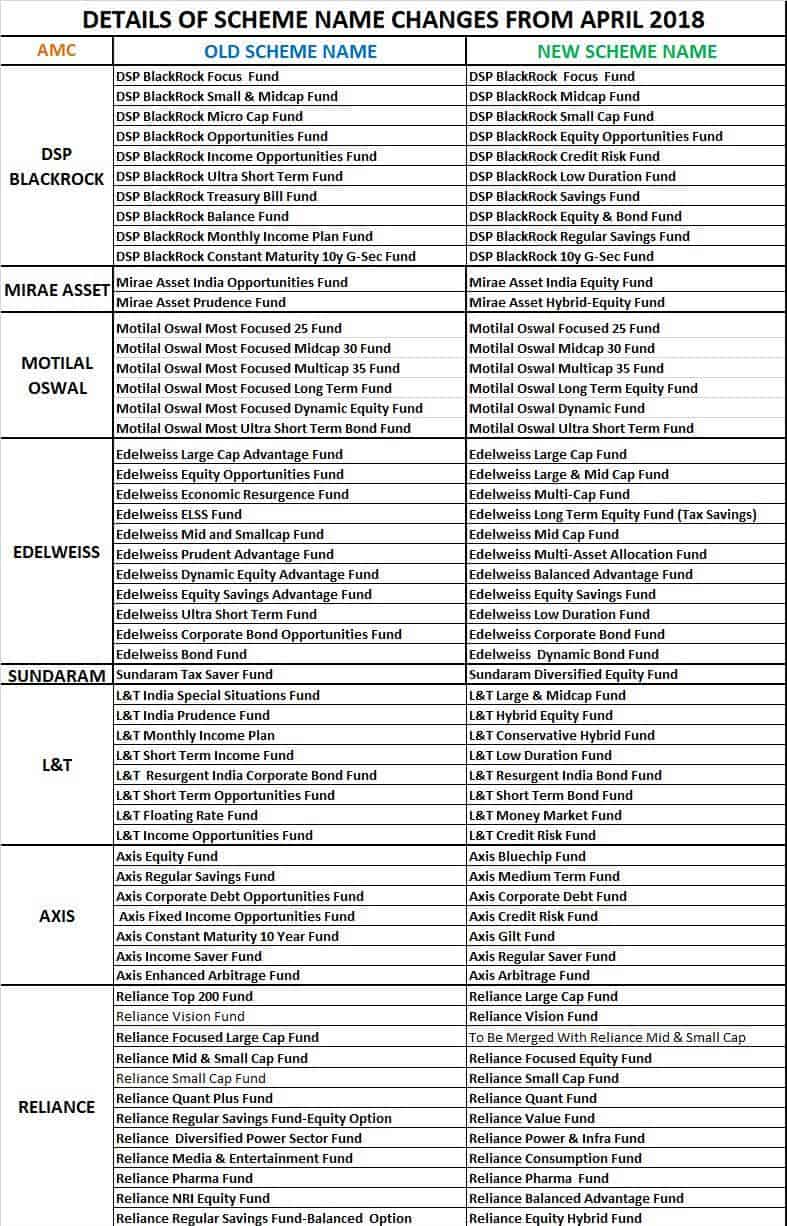

Some of the mutual fund schemes have already got the approval and changed their names with required strategies. Check out the list below

Conclusion:

Changes in mutual fund disclosure norms with TER and Benchmarking against TRI index are a welcome move as this will increase the Transparency of the products.

The categorization of the schemes is also a good move for the investors as they will be in a better position to compare and understand the feature of the scheme. However, it may limit the Fund managers stock selection beyond a set category and may impact the funds’ performance for a short time frame.

Investors should keep a watch on the developments and the changes and take an informed decision.

You will find many such changes in the coming days in many funds, and if there is a fundamental attribute change, then you will be given adequate time to redeem your holdings without exit load. But in case you redeem, then do keep in mind the taxation issue.

Also, at the time of the Investments review do check the category and structure of the fund before and after these changes.

{kind=link}