Monthly Income Plans (MIPs) are meant to provide monthly income to the investor through regular dividends but you can also create a stream of income through Systematic withdrawal plan (SWPs). Dividends results in reduction of NAV and are subjected to Dividend distribution tax on the other side SWP leads to reduction of unit capital of investment as withdrawal happens from the existing units only. Now the question is which works better in Monthly Income Plans – Dividend payout or SWP. Some back testing results that Systematic withdrawals give better results than dividend payout.

Actually few days back one of the readers Ashish asked me that now when the dividend distribution tax in debt mutual funds is going to increase, so would it be wise to stay with the dividend payout option in Monthly Income plan or is there any other strategy to manage the situation better. So just to answer him, I did this calculation which I am sharing with you now.

Before going ahead, let me explain the product i.e Monthly Income Plan (MIP) and Facility/ option i.e Systematic withdrawal plan (SWP) in short.

What is a Monthly Income Plan?

Monthly Income Plan popularly known as MIP is a debt oriented hybrid mutual fund product. In MIP Equity is allocated in between 5% -25%, and the balance would be the debt allocation. The Investment objective of Monthly Income plans read as , “ To generate regular returns through investment primarily in Debt and Money Market Instruments , also to generate long-term capital appreciation by investing a portion of scheme’s assets in equity and equity related instruments”. Though the objective is to provide regular returns, but the regularity and quantum is not assured. Advisors/Planners do advise on MIP to supplement the goal of regular returns and also to provide some tax efficiency in client’s profile. MIPs also get advised in growth option if client portfolio and risk profile demands.

What is Systematic Withdrawal Plan?

Systematic withdrawal plan also known as SWP is a facility that allows an investor to withdraw money from existing mutual fund investments at specified intervals. SWP facility is used to create a regular flow of income from investments. You can do a Fixed SWP where you specify the amount you wish to withdraw or Appreciation SWP where you can withdraw the appreciated amount every month or quarter.

How Systematic withdrawal is beneficial in Monthly Income Plans?

Now you have understood that to generate regular income (not assured) from MIPs, you can either opt for Dividend payout option, which are irregular and also not certain or you may go with MIP growth option and opt for SWP. In the former case you have to bear with the dividend distribution tax and in latter you withdraw units out of your capital and appreciation (if any). Question is which would be better option.

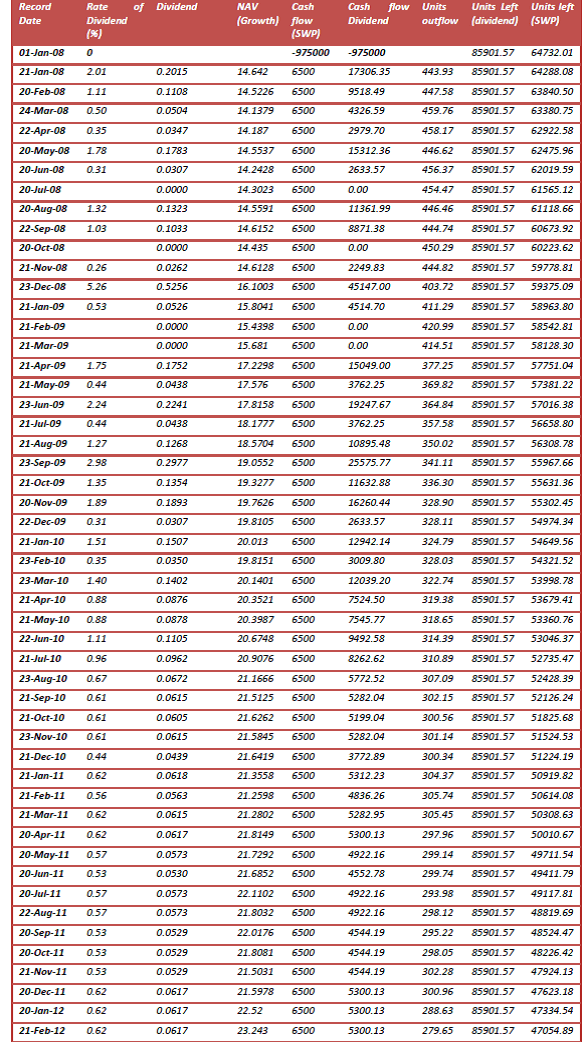

I did some back testing on a Monthly income plan of one popular AMC to figure out the answer.

Below are the details.

Investment amount : Rs 975000/-

Date of Investment : 1 Jan 2008

Date of redemption: 1 Jan 2013

Product and Units alloted :

Reliance MIP (Monthly dividend payout): Units allotted 85901.57 (@ NAV – 11.3502)

Reliance MIP Growth : Units allotted 64732.01 (@ NAV – 15.0621)

SWP rate : @ 8% p.a payable monthly

Dividend dates/rates : As per actual

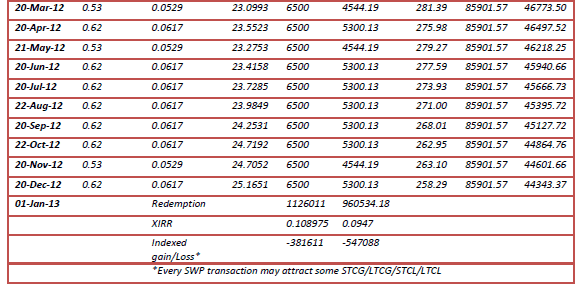

The above calculation clearly shows that in the last 5 years, Systematic withdrawal plan @8% p.a payable monthly would have been a better option than Monthly dividend pay out . The reason might be the dividend distribution tax, and if actually that was the reason than the returns will go down in future as the DDT has been increased from next financial year. Systematic withdrawal Plan in MIP has also shown better returns than the Post Office monthly income scheme where the returns are fixed but are 100% taxable. On the other side debt mutual funds has always been a tax efficient investment option. (Read – Bank deposits Vs debt funds)

How SWP was beneficial?

– SWP option has returned more as is visible through XIRR.

– SWP has reduced the taxation, as unlike Dividend option where DDT gets deducted, this leads to some Short/Long term capital gain/loss. Though it is not shown in the calculation above, but I am sure that it would surely be less than the DDT. Hope you agree with me.

– SWP has resulted in continuous and fixed cash flow stream and thus adequately supported the regular income criteria as required by Client.

Conclusion:

Well back testing clearly shows that Systematic withdrawal plan works better for Monthly Income plans to get regular income. But as per the standard disclaimer that “Mutual funds are subjected to market risk….”,future can’t be predicted. Moreover this calculation has been done on one of the top performing fund of the category, this may not result the same in other funds too. Overall, the bottom line is that looking at the increase in dividend distribution tax in debt schemes, systematic withdrawal plans should also be considered when the goal is to get monthly income in MIP funds.

What are your views? Do you agree with me in considering SWP in MIP?

{kind=link}

Very nice article. Good job done.

I have Rs 10 Lacs in SBI Dynamic Bond Fund ( Growth). They are with me for more than one year. Will it be a prudent decision if I start monthly SWP so that I get regular income ? or it works better only on MIPs ?

Request clarify.

Thanks,

Dr MCS

Thank you Dr Chandrashekhar.

See, we can’t compare a pure debt fund with MIP as MIP has some portion in equity too, to take care of growth aspect. Frankly, it is very difficult to say that whether SWP in SBI Dynamic will work the same way as is shown in the above calculation. I believe that your product selection should be as per your goal .When the goal is to get regular income, the product selection should also be the one which is meant to generate regular income. In MIPs the investment objective matches your requirement. Though we can use it in some other way as discussed above.

Thanks a lot. Got your point.

Dr MCS

Coming back to the same issue of SWP thru MIPs. I plan to go either for Reliance MIP or HDFC MIP.

After one year, I propose to have STP. Would that be fine ?

Funds are fine. and after 1 year every withdrawal will come under long term and thus will attract indexation…this also looks good from tax efficiency point. But where are you planning to start STP in?