Debt investments for long term, no way. Long term means equity only. This is what the norm these days is, this is what is being told, and this is what is being preached as best, since only equity investments are expected to give best returns over longer period. Debt is meant for short term.

The above is the general view in the market. All novices and even expert investors are getting over board on equity investments, not because they understand equity very well, but they are seeing the stock markets performing quite well. Due to this even the short term Investors feel that 1-2 years is enough to be considered as long term.

People are betting on the economic reforms and giving all the credit to the government policies, which has become another reason to look up to equity markets. Money is coming from all the sources be it Retail Investors directly or through Mutual funds, EPFO, NPS and other domestic Institutions, and also through foreign fund flows.

Some credit goes to unexpectedly high domestic fund flows, which are the result of Increasing awareness among retail investors and also due to the demonetization impact, as people are left with little or no options to invest their money besides the financial markets. And equity markets with positive sentiments attracted all the flow.

Data from the Association of Mutual Funds in India (Amfi) shows monthly inflow of Rs 4,269 crore through SIPs in April 2017, as compared to just Rs980 crore per month in 2012, aptly reflecting the increased interest in recurring savings allocations.Mutual funds’ equity and equity-linked savings schemes (ELSS) witnessed an aggregate net inflow of Rs94 billion ($1.5 billion) in April 2017, which is more than twice the April 2016 inflows, and 61% higher than the past 12-month average. (Source: Livemint)

Why debt investments for long term – a Perspective

The reason of me having this view is that at the core, Investors are human being, and thus are Loss averse, which means that loss gives them more pain then the comfort coming from gains.

A sudden fall in the market can change the view point in minutes. And just like rise, fall is also a reality, and the major test of patience for all the so called aware and long term investors will be in the falling market. Even today while making their purchases, Investors do not forget to ask as if this is the right time to enter the market.

The direct investors are confused with the news flow of high market valuations, are not following set process, not sure how to have a right asset allocation mix.

In my practice and process, finding the risk tolerance level of the Investors is important to suggest them a suitable Asset allocation mix, and since the test requires them to answer few different questions, which also includes –

“How much average return they expect from their investments over next 10 years vis a vis bank fixed deposits?”, their reply comes as 2 times or 3 times. If I do not ask in comparison to bank deposits their reply comes as 15% – 20%.

Everyone wants to make money and in the rising markets as fast as possible, but when asked about losses, as to how much down they are fine seeing their portfolio, and the answer comes as 10-20 or 30% (Who has read somewhere that higher the risk higher the return). When I Translate this percentage in absolute terms that 30% means 30000 to 1 lakh, but 30 lakh to 1 crore then some of the higher loss (Risk) seeker Investors, falls in line and realize that they are not that aggressive investors.

Further the past data as researched by the risk tolerance software “Finametrica”, makes people realize that to have a good and stable portfolio they have to have a good mix of Equity with debt even for long term, else the portfolio will become so volatile which may start making them uncomfortable.

I am going to share with you some of the data from the same reports to let you understand why debt investments are important for long term too.

This data was computed using the following indices and is up to 31 Dec 2016:

Fixed Interest – India 10-year Government Bond Total Return Index

IND Stocks- MSCI India GR Index

International Shares- MSCI World Total Return Index

As per the analysis of 100% of Equity allocation, with spread as 90% in Indian Equities and 10% in International equities, in the last 10 year the portfolio has generated average return of 1.78 times of bank deposits. The average bank deposits rate were 7.6% during this phase, which means a return of 13.52% on CAGR basis. Sounds good?

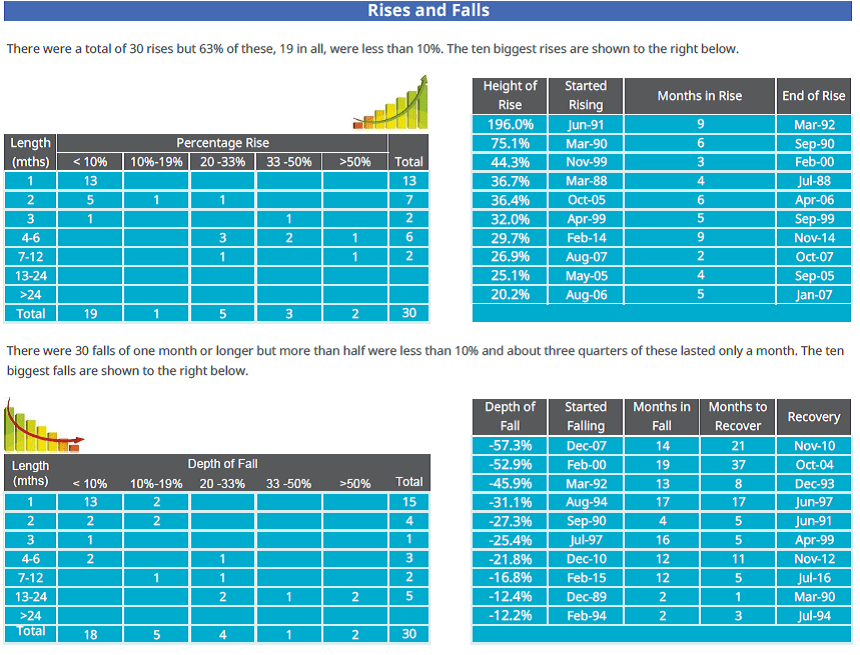

Now have a look at the past 28 years’ performance data of the same allocation in different time periods.

100% equity allocation has fallen by 57.3% in December 2007, the fall was spread in 14 months and 21 months to recover from there, thus it took almost 3 years to recover back to the same level. Though you may also see comparative rises too, as during Oct 05 to April 06, in just 6 months markets raised by 36% and also by 27% in just 2 months of Aug 07 – Oct 07.

When the markets are going through a euphoric phase, every fall looks like an opportunity to buy, and this slow fall is enough to attract or I should say trap new investors.

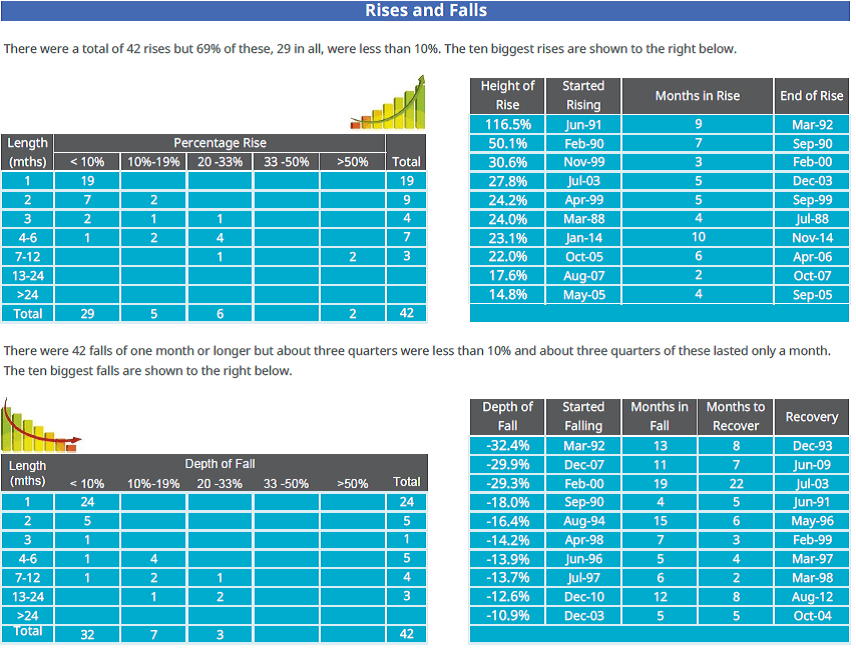

Now, let me show you some other data of 60% growth and 40% defensive. This portfolio has generated return of 1.67 times of bank deposits, which translated to 12.69% of CAGR returns. This is around 0.82% lesser than 100% equity (Growth) portfolio.

Just compare the depth of falls with 100% equity. By reducing 40% exposure from direct equity, you have compromised the returns of 0.82%, but also have considerably brought down the volatility of your portfolio.

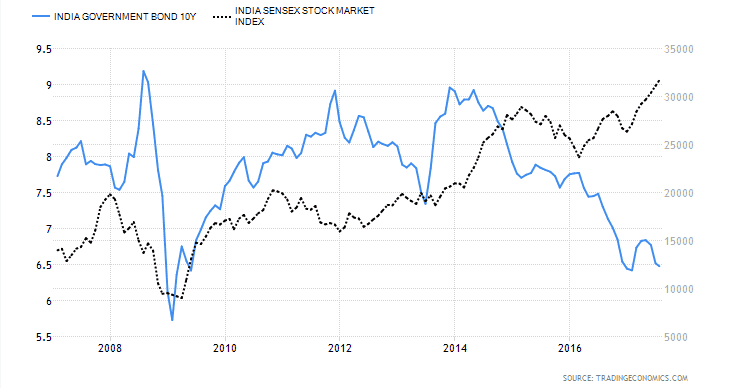

Please understand that debt is not a no earner in the portfolio. Where debt brings balance in your portfolio’s volatility, it also brings potential of earning good returns too, especially in falling interest rate scenario. In the high interest scenario, it provides the accrual gains. below is the performance chart of last 10 years, which clearly reflects the importance of debt investments for long term.

It is only in the rising interest scenario that you may find comparatively lesser returns in long term debt funds, but that gets managed by keeping lower average duration. Below chart shows how 10 years governemnt bonds and sensex have moved in last 10 years.

Conclusion:

In layman terms, Falling interest rates means government wants to give push to the economic activities, that becomes a good sign for equity too, and sometimes rising interest rates means RBI wants to curb money flow into the economy to control Inflation, which also means that markets are now in bullish phase, but its better to be cautious.

However this is also true that you may predict a long term trend of interest rates, but short term scenario will always be unpredictable and thus will always remain a traders’ space to gamble.

If you are a serious long term investor then look at the things from fundamental point of view and have a suitably allocated portfolio into Equity and debt both.

{kind=link}