Every Union Budget has an impact on our money—sometimes directly, sometimes indirectly. The direct impact comes through changes in income tax rules, deductions, or new savings schemes. The indirect impact happens when Budget decisions affect industries, businesses, and stock markets, which, in turn, influence our investments and even daily expenses.

For example, if the government announces tax benefits on electric vehicles, buying one might become cheaper. If there’s a big push for infrastructure, stocks of cement or construction companies could go up, affecting your mutual fund returns. On the other hand, higher import duties on certain products could make some of your regular purchases more expensive.

Simply put, the Budget is more than just numbers—it shapes the way we earn, save, invest, and spend. Let’s look at the key personal finance takeaways from Budget 2025 and how they might impact your financial life.

Indirect benefits are harder to notice since they take time to play out and depend on many other economic factors. So, for immediate grasping of the announcements, let’s focus on the proposals that will directly impact you in some way or the other. (Read : 5 bad money habits impacting your wealth, and what to do about it?)

Union Budget 2025 – 7 proposals impacting your finances.

New income tax Slabs –

The government has announced new income tax slabs in the new tax regime. The old regime slabs were left unchanged.

| Total Income | Rate of Tax |

| Upto Rs 4 lakh | NIL |

| From Rs 4 lakh to Rs 8 lakh | 5% |

| From Rs 8 lakh to Rs 12 lakh | 10% |

| From Rs 12 lakh to Rs 16 lakh | 15% |

| From Rs 16 lakh to Rs 20 lakh | 20% |

| From Rs 20 lakh to Rs 24 lakh | 25% |

| Above Rs 24 lakh | 30% |

Of course, these new slabs have made the new regime much more attractive than the old rates and the old regime tax slabs, unless you are using all the exemptions available under sections 80C, 80D, 24B, etc.

The excitement of No tax on income up to Rs 12.75 lakh vanishes when your income is more than this amount. For higher-income people, the tax must be calculated per the new slabs (for FY 25-26). Though there definitely will be a tax reduction in comparison to the previous year, but its not ZERO at least.

87A Rebate:

If your total income is up to 12 lakh then the enhancement in the Section 87A Rebate will make your tax outgo to zero. The Rebate amount has been increased from Rs 25k to Rs 60k, which will make the total tax payable amount to NIL in case your income is below Rs 12 lakh

Insurance Policies in Gift City

This change applies to NRIs purchasing life insurance policies from insurance companies operating under the jurisdiction of IFSC. In simpler terms, it covers policies bought from life insurance companies registered in GIFT City.

A few years ago, the government introduced restrictions on tax-free maturity benefits for insurance policies. Under these rules, if the annual premium (or total premiums paid) exceeds ₹2.5 lakh for ULIPs or ₹5 lakh for traditional/endowment policies, the maturity proceeds become taxable. This restriction also applied to NRIs investing in Indian insurance policies.

However, to ensure parity between NRIs buying policies from GIFT City-based insurers and those purchasing from foreign jurisdictions, in union budget 2025 Section 10(10D) has been amended. Now, policy proceeds from GIFT City insurers will be fully tax-free, with no restrictions on the maximum premium paid.

(Also read : GIFT City in India: Unlocking Investment Opportunities for Global Investors)

ULIP Tax Clarity

As mentioned earlier, if a ULIP is purchased by an Indian resident or an NRI within the prescribed premium limits and with a minimum sum assured of 10 times the premium, the maturity proceeds remain tax-free. However, there was uncertainty regarding the tax treatment of ULIPs exceeding these premium limits.

The Union Budget 2025 has now clarified that ULIPs not eligible for tax exemption under Section 10(10D) will be treated as capital assets and classified under the definition of an equity-oriented fund.

As a result, the applicable tax rates will be:

- Long-Term Capital Gains (LTCG): 12.5%

- Short-Term Capital Gains (STCG): 20%

This clarification provides greater transparency on the taxation of high-premium ULIPs, aligning them with other investment-linked insurance products.

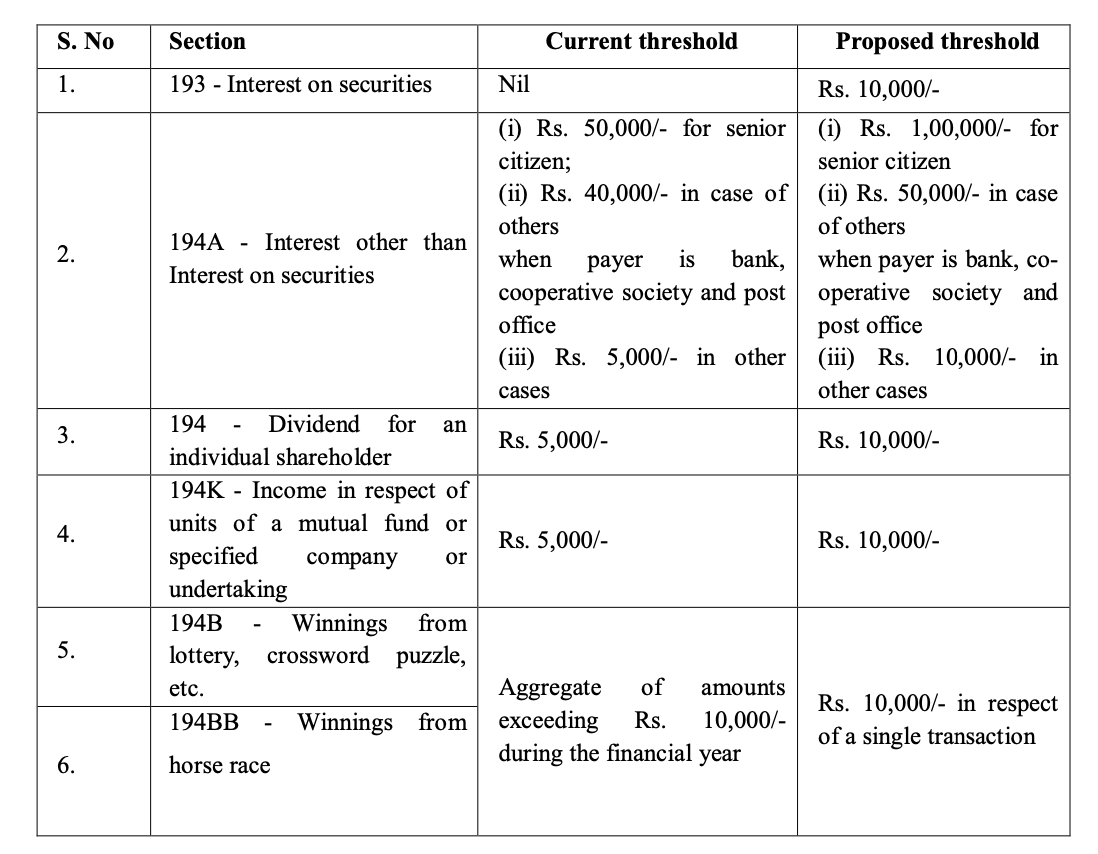

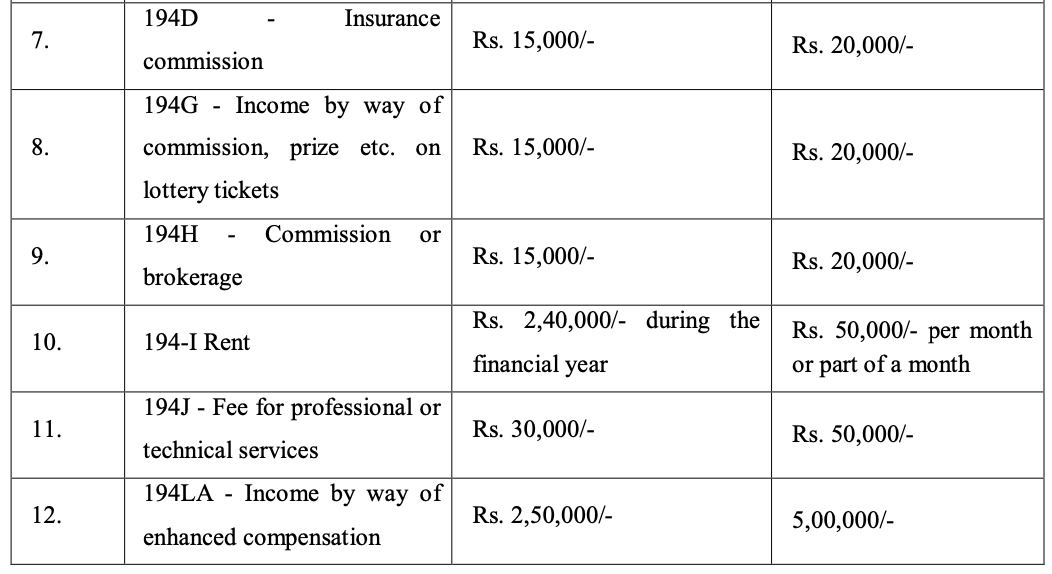

TDS & TCS Rates

The TCS threshold for foreign remittances under the LRS mechanism has been increased from ₹7 lakh to ₹10 lakh in union budget 2025. Additionally, if the remittance is for education purposes and funded through an education loan from an authorized bank, no TCS will be deducted.

Apart from TCS, there have also been revisions in TDS thresholds:

- For senior citizens’ bank deposits, the TDS threshold has been raised from ₹50,000 to ₹1 lakh.

- For dividends paid to shareholders, the threshold has been increased from ₹5,000 to ₹10,000.

These changes provide greater relief to taxpayers by reducing the upfront deduction of tax on their earnings and investments.

(Here’s an interesting read for you : Risky Roads to Higher Returns- A Reality Check for F&O Traders)

The complete list is shared below

NPS Vatsalya

The NPS Vatsalya Scheme, officially launched on September 18, 2024, allows parents and guardians to open a National Pension System (NPS) account for their children. This savings-cum-pension scheme is designed specifically for minors and will be managed by the guardian until the child reaches adulthood.

Once the minor turns 18, the account will continue under their name, carrying forward the accumulated corpus. It will then be converted into an NPS-Tier 1 Account (All Citizen Model) or transferred to another non-NPS scheme account, as per the regulations.

To encourage savings under this scheme, tax benefits under Section 80CCD are proposed for the guardian, with the exemption capped at ₹50,000 in aggregate.

Additionally, the scheme allows partial withdrawals to meet specific financial needs, such as education, treatment of specified illnesses, or severe disability (above 75%) of the minor. To ensure tax efficiency, a new Clause (12BA) in Section 10 of the Act is proposed. This clause states that any income from partial withdrawals will not be included in the total income of the parent/guardian, provided it does not exceed 25% of the contributions made by them, subject to the scheme’s terms and conditions. (Read : NRI Retiring in India – Important Points to Consider)

Self Occupied property

Under the current rules, if you own two house properties, you can declare one as self-occupied, with its annual value considered NIL for tax purposes. However, the second property, even if vacant, is treated as “deemed let out”, and you are required to pay tax on its notional rental income.

In Budget 2025, this rule has been amended, allowing taxpayers to claim the self-occupied benefit (NIL annual value) for up to two houses. This provides relief to homeowners who own multiple properties for personal use. (Read: How to calculate taxes on House property?)

Beyond these above changes, several other announcements could have a long-term impact, such as the development of structured pension payout products and the launch of a revamped Central Know Your Customer (KYC) Registry. While these may not grab headlines, they aim to simplify financial transactions and enhance ease of living in the future.

Every Union budget brings something new and gives us a chance to review our personal finances and make changes in our personal financial budget accordingly. This time the biggest announcement was of the tax reduction on income up to 12 lakh per annum, which leaves you with decent savings. Now whether you spend it or save it for your future, is up to you.

As always, the key to making the most of these announcements is to align them with your financial goals. Whether it’s optimizing tax benefits, adjusting your investment strategy, or planning for future expenses, staying informed and proactive will help you navigate these changes wisely.

Financial planning is not just about reacting to Budget announcements but about maintaining a well-thought-out approach to wealth creation and security. So, take stock of the updates, assess their impact on your personal finances, and make decisions that keep you on the path to financial well-being. (you may also be interested in: Annual Health Checkup of Finances)

Image source :Mint

{kind=link}