")

Public Provident Fund or as it is popularly called PPF is one of the best debt investment instruments available in India. It suits every kind of investor for one’s debt portfolio.

The Tax-free return backed by government guarantees makes it more attractive for investors. Above all the investment in Public Provident Fund is eligible for tax saving u/s 80C. All these features have made the Public Provident Fund scheme a darling investment option.

Through this article, I will discuss with you, What the Public Provident Fund account is? the basic features of the Public Provident Fund scheme, the latest changes announced in the PPF Scheme 2019, and why or why not one should consider investing in this. I have also shared the PPF Interest rate History to understand how this product has changed in the past.

Basic Features of Public Provident Fund:

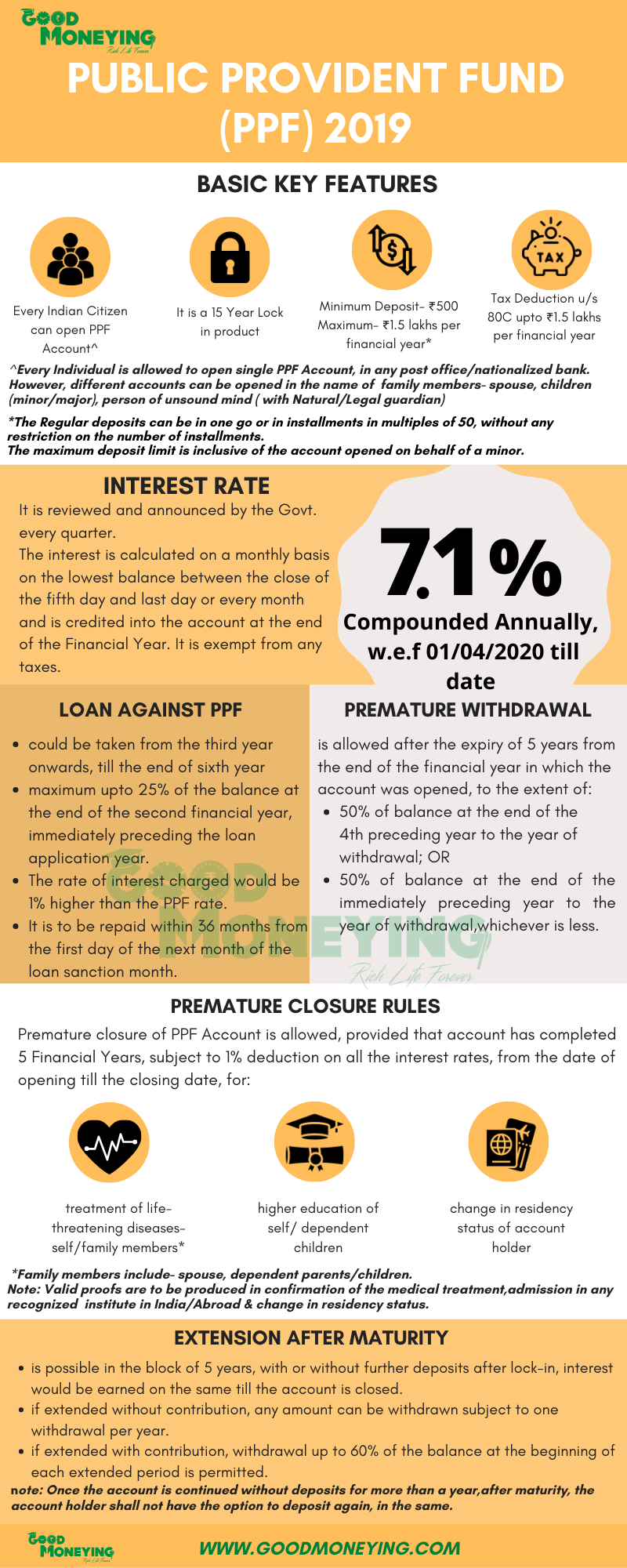

1. Tenure: It is a 15 years product with 16 years lock-in. The first year of investment is not counted for 15 years maturity. If you have opened the PPF a/c on 15 July’2000, then 15 years tenure will start from the end of FY 2000-2001 i.e. 31st March 2001. The maturity date, in this case, would be 31st March 2016.

2. Deposit Limits: Minimum investment per financial year in Public Provident Fund scheme is Rs 500/- and w.e.f 1.12.2011 the maximum limit has been raised to Rs 1.50 lakh which was earlier Rs 1,00,000/- The deposit can be in one go or in a number of flexible installments not exceeding 12 per financial year.

Please note that Public provident fund (PPF) account can be opened with an initial deposit of Rs 500/- only.

As per PPF Scheme 2019 rules, deposits are allowed in the multiples of Rs.50 and there is no upper limit on the number of deposits per financial year.

3. Interest rates: The interest earned in Public Provident Fund remains fixed for one quarter and is no longer guaranteed forever. It is actually benchmarked to the 10-year government bond yield and will be 0.25% higher than the average government bond yield. This rate will be declared every Quarter.

The Interest is computed for a calendar month on the basis of the lowest balance in an account between the close of the 5th day and the end of the month and the Interest is credited to the account of the account holder at the end of the year. Thus it is advisable to deposit money in this before 5th of any month.

With effect from 1st April 2020, the public provident fund interest rate would be 7.10% p.a. (compounded Annually).

4. Account Holders :

a) Public Provident Fund account can be opened in the name of Individual (salaried or self-employed). NO HUF or association of person is allowed to open PPF a/c.

b) PPF account can also be opened in the name of a minor, person of unsound mind through guardian who can be father or mother or a person appointed by the court (if the guardian is not there). Thus Grandfather or Grandmother are not allowed to open a/c in the name of Grandchildren

Only one account is permissible to one individual. Thus if the father has opened an account in the name of the child, the mother cannot open the Public Provident Fund Account in the name of the same child.

c) No Joint account can be opened.

d) Non-Resident Indian (NRI) cannot open a new Public provident fund account in India. Prior to 2003, NRIs were not even allowed to make contributions into existing PPF accounts, that is, accounts opened before they became NRIs. However, in 2003, a notification (MOF (DEA) No GSR 585 (E) dated 25.7.2003) was issued permitting NRIs to continue investing in existing PPF accounts till maturity.

Also read: W.e.f. 3rd October 2017, NRIs are not allowed to continue with their PPF accounts

5. Premature withdrawal: Many people avoid this investment just because of the lock-in period of 15 years. They are not aware of the premature withdrawal facility available in this. In PPF accounts you are allowed to make partial withdrawals in times of financial crises. You are allowed to withdraw seventh year onwards from the date of account opening i.e. after the expiry of 5 years from the end of the financial year in which the account was opened and that too once a year. Such withdrawal figure must not exceed 50% of the balance at the end of the fourth year, or 50% of the balance at the end of the immediately preceding year, whichever is less.

Let’s suppose your account was opened on 8th August 2013 i.e. in FY 2013-14.

First withdrawal date: Add 6 to the financial year-end => 2014 + 6 = 2020. It shows that the seventh financial year would be 2019-2020.

Amount of first withdrawal: The 4th preceding year will be 2020 – 4 = 2016 (FY 2015-16) and the preceding year 2020 – 1 = 2019 (FY 2018-19). Amount withdrawable in the 7th year, FY 2019-2020 is 50% of the balance to the credit as on March 31, 2016, or March 31, 2019, whichever is lower.

6. Loan on PPF :

Loans could be taken from the third year onwards till the sixth year i.e. after the expiry of one year but before the expiry of five years from the end of the year in which the account was opened. Let’s suppose you opened your PPF account in December 2011 (in the FY 2011-12), you can avail a loan only in FY 2013-2014 (2012+2 = 2014) till FY 2016-2017 (2012+5=2017).

You can avail a loan amount of up to a maximum of 25% of the balance in your account at the end of the second year immediately preceding the year in which the loan is applied for.

If you apply for a loan in November 2013 (FY 2013-2014), you would get 25% of the amount that existed at the end of March 2012 (2014-2 = 2012).

Only one loan is allowed per individual per financial year. Second loan can be taken only after the first one is repaid in full.

As per PPF Scheme 2019 rules, the rate of interest charged on this loan would be 1% higher than the PPF rate. Previously this was 2%.

This loan is to be repaid by the account holder before the expiry of thirty-six months from the first day of the month following the month in which the loan is sanctioned.

For instance, if the loan was sanctioned on 25th January 2018, then the loan tenure of 36 months starts from the 1st of February, 2018. If the loan is not repaid within 36 months, interest would be charged @6% p.a. on the outstanding amount from the date of loan disbursal.

7. Discontinued accounts:

You need to deposit a minimum of Rs 500/- per Financial Year, failing which the account will be termed as a discontinued account. Interest would, however, continue to accrue. You could regularize the account again by paying the penalty fee of Rs 50/- for each year of default along with subscription arrears of Rs 500/- per Financial Year.

Also read: PPF Premature closure guidelines

8. Continuation after maturity: After 15 years of continuation i.e. on maturity, the PPF account holder has 2 options, either to take out the maturity amount and close the account or to further extend it for the block of 5 years for any number of periods with or without further subscriptions.

However, interest can be earned on the balance, till the account is closed. If extended without contribution, any amount can be withdrawn subject to one withdrawal per year.

If extended with contribution, withdrawal up to 60 per cent of the balance at the beginning of each extended period (block of five years) is permitted.

Please note that, as per PPF Scheme 2019 rules, if any contribution is not made for 1 year after maturity, the account holder would not be allowed to contribute anything to that account, thereafter.

9. Tax benefits: Public Provident Fund in India offers multiple tax benefits. It offers Tax saving on deposit u/s 80C up to a maximum limit of Rs 1.50 lakh; also the interest earned in PPF enjoys tax-free status.

PPF Scheme 2019- Infographics:

The below infographics explains the changes in PPF Scheme 2019:

Other Important features of Public Provident Fund Account:

- The Public Provident Fund scheme is operated by Post Office and Nationalized banks. PPF account can be opened either in Post Office or in a Bank. These days even Pvt Banks like ICICI bank offers this account.

- The account is easily transferable between post offices or banks, even between post offices and banks.

- The balance amount in the Public Provident Fund account is not subject to attachment under any order or decree of the court in respect of any debt or liability, but it can be attached by the Income Tax and Estate Duty authorities.

- Nomination facility is available.

PPF Interest Rates History:

| Period | Interest Rate |

|---|---|

| 1981-1986 | 9.50% |

| 1986-2000 | 12.00% |

| 2000-2001 | 11.00% |

| 2001-2002 | 9.50% |

| 2002-2003 | 9.00% |

| 2003-2004 | 8.00% |

| 2004-2011 | 8.00% |

| 2011-2012 | 8.60% |

| 2012-2013 | 8.80% |

| 2013-2015 | 8.70% |

| 2015-2016 (Q1) | 8.70% |

| 2015-2016 (Q2) | 8.70% |

| 2015-2016 (Q3) | 8.70% |

| 2015-2016 (Q4) | 8.70% |

| 2016-2017 (Q1) | 8.10% |

| 2016-2017 (Q2) | 8.10% |

| 2016-2017 (Q3) | 8.00% |

| 2016-2017 (Q4) | 8.00% |

| 2017-2018 (Q1) | 7.90% |

| 2017-2018 (Q2) | 7.80% |

| 2017-2018 (Q3) | 7.80% |

| 2017-2018 (Q4) | 7.60% |

| 2018-2019 (Q1) | 7.60% |

| 2018-2019 (Q2) | 7.60% |

| 2018-2019 (Q3) | 8.00% |

| 2018-2019 (Q4) | 8.00% |

| 2019-2020 (Q1) | 8.00% |

| 2019-2020 (Q2) | 7.90% |

| 2019-2020 (Q3) | 7.90% |

| 2019-2020 (Q4) | 7.90% |

| 2020-2021 (Q1) | 7.10% |

| 2020-2021 (Q2) | 7.10% |

| 2020-2021 (Q3) | 7.10% |

| 2020-2021 (Q4) | 7.10% |

| 2021-2022 (Q1-Q4) | 7.10% |

| 2022-2023 (Q1-Q4) | 7.10% |

| 2023-2024 (Q1) | 7.10% |

| 2023-2024 (Q2) | 7.10% |

Notes:

- The highest PPF interest rate was 12%, from 1986 to 2000.

- From 2016 onwards, the government started revising interest rates quarterly, as part of a broader initiative to align the rates with market conditions.

Should you invest in Public Provident Fund?

One thing is very clear that with the EEE (Exempt –Exempt – Exempt) nature of this product, this is a “Must have” investment account in one’s portfolio. Moreover the early you open this account, early you will get over with the lock-in period.

One should consider the following points before investing in this product.

- Taxation: Don’t look at tax-free interest only but also the income tax bracket you fall into. Some years back PPF rate was 8.6% and 10 years bank FD rate was 9.5%, so for the one who falls into 10% tax bracket, FD was looking more attractive option. But since it is a long-term investment and PPF assumed to remain tax-free option for quite a long time, so it looks good to invest for everyone. For other high-income bracket people, this investment is undoubtedly an all-time very good option.

- Asset Allocation: You have to consider the overall asset allocation, which has been designed for the achieving of your long and short-term goals. If you are already putting enough money in debt through compulsory EPF/GPF deductions, then you may not require PPF investment, but as I said earlier that this product should not be ignored also.

- Interest rates movement: If one is aware of how debt product actually performs with the interest rate cycle, then he/she can take advantage of the high rate by investing the portion in debt mutual funds, to take the benefit of fall of interest rates in future.

Conclusion:

With the linkage of PPF rates with G sec yields, this is very much clear that we may find these rates to go down some year. One can recall those years when the G sec rates were in the range of 5.5%-6%. If that scenario has to repeat in the next few years (which is not sure) than Investment in Debt mutual funds would be a wiser choice at present. (Read: bank deposits vs debt mutual funds)

PPF or Public provident fund is a very long-term and good instrument to invest in. One can map this with any of long-term goals. Earlier you can easily calculate the future value of investment in this product since the interest rates were fixed. But these days, when interest rates are linked to the Government securities rates, so the investor has also to be vigilant enough for his investments so that this volatility should not affect his achievement of goals.

Do you have any question on PPF (Public provident fund)? you may ask in the comments section below.

{kind=link}

thanks for the information shared.likewise share on gratuity.

Thanks. Will surely do a post on gratuity..sometime.

It is very useful information, Can you tabulate for premature withdrawal for rs 1 Lake considering

Hi,

Its a well written and very informative article. Though i hold a PPF account but was not aware about so many benefits attached to this investment option. Well done.

Regards

Simran Verma

Thanks Simran.

Good article. Some areas which you may want to add :-

1. Transfer of PPF acct from One Bank to another (Not branch). Eg SBI to Bank of Baroda.

2. Transfer of PPF acct from Public sector Bank to Pvt Sector bank

3. Linking PPF acct to your Savings account for Online Txfer of funds

4. Online contribution to PPF acct. SO you need not wait to goto Bank, stand in Q for Hrs to make the contribution & then Stand in another Q to get your PPF passbook update. I always dread to visit local SBI for PPF passbok update. I recently went & stood for 2 hrs just to submit my PPF acct extension form.

Regarding your 3rd and 4th points, I want to share my experience with SBI. I have got Netbanking facility from them and it is very much convenient to transfer funds from my SB a/c to PPF A/c and get an online receipt also. I rarely need to visit them for this work. Also a account extention form could be sent by Post as they told me. Further the passbooks they have issued is printed one and can be updated from any of their branches without any charges. Online statements can also be downloaded from online internet banking site.

Thanks Manoj, for sharing your experience.

Thanks Sanjay.

Though i tried to consolidate your first 2 points in one line “Account is easily transferable between post offices or banks, even between post office and banks”, but you have made it more specific. Thanks to you.

I understand the hardship or experience people have operating PPF accounts, so this online contribution is very helpful for them.

Yes, i missed mentioning this facility in the article. Thanks for sharing this with readers.

Hi, I am leaving my cuerrnt Private MNC and have no plans to join the other one for next 2 years. My Employee PF account is 2 years old. I heard if I will withdraw the amount now,30% tax will be charged. Can I open PPF account and transfer the full Company PF amount to this new PPF account. Is it possible? Will the tax be deducted while transferring from PF to PPF account. Also,I am having more than 70k in my Employee PF.Note: I dont have any PPF account as of now.Kindly Suggest..

I will suggest you to eetnxd your PPF account for another 5 years, provided you do have need this money for your child education or marriage during these 5 years. Earn guaranteed 8% on your PPF account for eetnxded next 5 years. And for higher returns invest your other money into equity mutual funds.

Yes venkat it is true that if you withdraw your PF amount before completion of 5 years of your Job it will be taxable.

But PF and PPF are 2 seperate instrument and shifting the amount into PPF will not solve your purpose. Even if you want to deposit money in PPF , your PF withdrawal will remain taxable. There can be one solution to it:

Don’t withdraw the PF balance right away and keep on enjoying the tax free returns getting accumulated in that. 2 years later wen you join new job, transfer the current PF balance to the new one. This way you can avoid taxation. But do note few points like, if you believe there could be operational issues later on with your existing employer then you may consider withdrawing the complete PF right away. Also don’t delay the process for more than 3 years , as after 3 years of non contribution in PF the PF a/c will be treated as inactive and you will stop earning interest on that.

Dear all,

I have a query. In my earlier organisation , I worked for 4 years and 8 months and resigned the service in April 12. They were depositing my PF in the company’s society.

Till now I have not withdrawn the PF amount. But till date , I have crossed the 5 years. I want to understand , if i withdrawn now, will my PF amount be taxed.

Whether 5 years is , years of experience or 5 years of PF account existence . Please guide

With Regards,

Maniraj P

mani, 5 years is the continued contribution requirement in a PF account. So in your case after working for 4 years and 8 months, you have continued your PF account with contribution for complete 5 years, so the withdrawal will be taxable.

With PPF Accounts offering such high interests and that too tax free, PPF Accounts provide a higher after-tax interest as compared to after-tax interest on FD’s

Very True, Karan

can i have ppf and epf account both

as i was having my ppf account and now my employer has started epf scheme

so can i hav both?

Yes Vivek, you can have both the accounts.

My PPF a/c got matured in 2011. Now the bank is asking me to withdraw the amount & close the PPF a/c.

How do i take 5 yrs extension to this a/c after 2 years from expiry.

MKM,

The choice to extend the PPF account with subscription has to be made within one year from the maturity of the account. If this is not done, then by default the account is deemed to have been extended without further contribution for a period of five years. The only thing that investors should be careful of is that once an account is continued without contribution for any year, the subscriber cannot change over to with-contributions extension.

But you can make it as with contribution after completion of this 5 year extension period.

I remember my father used to earn 16% in his PPF account in 1990 s, as inflation in 1990 s was around 15%. If the inflation does become 15% in next 15 years, the interest rate of PPF will also be 15%, it will not stay at current 8%. As PPF interest rate is decided and reset, if needed, by Government of India every year. So PPF WAS, IS and WILL be one of the EXCELLENT investment at any time

Dear Aloke,Good point. The withdrawal limit after 6th year is lower of the folilwong — 50% of your contribution till the end of the 4th year and- 50% of your contribution till the end of previous financial year

what about the inflation rate which is anurod 8-9% and wud be even higher in next 15 years ppf is a good investment for risk averse people but not a good one if compared to other investment options which can give 15%.

I HAD A PPF A/C FROM LAST 19 YEARS AFTER 1 YEAR MY A/C IS MATURED BUT I WANT TO CONTINUE INVEST IN PPF KINDLY LET ME KNOW THAT IN FEATURE I M ABLE TO INVEST IN PPF A/C OR NOT IF YES HOW?

THANKING YOU

You can continue with your exisiting PPF account by renewing it for 5 more years. Infact you can renew it any number of times but in the block of 5 years each time.

Thank you for the early reply!

Is their any flexibility of changing the PPF amount after opening the account??

The compulsion on contribution is only Rs 500/- minimum and Rs 1 lakh maximum. In between there’s complete flexibility . You may change the amount of deposit every year/every month etc.

[…] One can use this product for Child future planning also along with Retirement savings. If you use this product to the full and keeps on investing Rs 1 lakh every year, then at maturity you could be able to accumulate Rs 27.15 lakh (assuming return @8% p.a), and if you extend this for another 5 years with contribution , then your corpus would be Rs 45.76 lakh. So on and so forth. (Read: All about PPF) […]

[…] investment products include purchasing shares through demat accounts, buying NCDs, investing in Public Provident Fund, Endowment LIC policies, National savings certificate etc. and for short to medium term – […]

hi,

i want to invest 1000 rs per month in PPF, then how much amount will i get after 21 years from it.

i want calender that shows flow send it to my mail.

Rgds

Pankaj

[…] in other way you gets restricted due to the limit of investment in some instruments like as in PPF (Read : All about PPF) , then you may start with a 100% specific beneficiary Trust in the name of your child and invest […]

Hi..

I would like to know one thing. Is the return amount after the PPF maturity taxable? Some sites claim only that the interest is tax free but not the principal. I am not clear.

For eg. Suppose I invest Rs 24000/- every year for 15 years. At 8% average rate of interest, the maturity amount will be Rs 7,03, 782/-. I would have paid Rs 3.6 Lakhs. So the total compound interest earned will be Rs 3,43,782/-. So is this amount tax free and I need to pay the tax on principal which is 3.6Lakhs ??

Please advise me. Thanks in advance..

Regards,

Karthik VR

Karthik the complete maturity amount including principal will be tax free.

Hello Mani..

Thanks a ton for the reply. Good day ahead..

Dear Sir/Madam

I have opened PPF Account in Jan-2000. Advise the year when 15 years will be completed & I will get my money.

Regards

You have opeed your account in FY 1999-2000. so the 15 year gets completed in fy 2014-2015. So the maturity date in your case would be 31st march 2015.

HI,

I HAVE LEFT MY COMPANY IN FEB 2010 AND I HAVE NOT TRANSFERRED/WITHDRAWN MY PF AMOUNT. CAN I TRANSFER THIS AMOUNT TO PPF ACCOUNT OR WITHDRAW IT NOW. I HAD WORKED IN THAT COMPANY FROM JUN 09 TO FEB 10.

REGARDS,

JAIDEEP

Jaideep, PF and PPF are 2 different non related product. So you cannot transfer the PF balance to PPF. But yes you can withdraw the amount and then deposit the same into your PPF account. Also pl note that the your withdrawal of PF will be taxable as it has not completed 5 years tenure.

hi manikaran .. thanks, i want to know one more thing.. if i apply for withdraw of my PF amount directly to PF office. i have to apply the same office where my account is registers or i can apply in any of the office throughout the country.

thanks.

Jaideep , you will have to approach the office where your account is registered.

I have one PPF A/c in my Name and another in my sons same who is a minor with me as natural guardian.

Can I deposit 1 lac individually in my account and another 1 Lac in my sons account and i will take care to claim only 1 lac ( and not 2 lacs) for IT purpose.

No Nik. You cannot deposit 1 lac individually in each account. The total contribution should not be more than 1 lakh (combining 2 accounts)

I would like to close and withdraw the full amount from my PPF account. I left the service upon retirement in 1997 and obtained permanent residency status in US during 1998. The Bank wants to see a copy of document that shows the date of becoming NRI. What will be the legal significance of that document/date?

Bank just want to see the documents so that if they have paid interest after renewing it automatically though without contribution that can be reversed.There’s no legal consequence of the same. NRIs are not allowed to open fresh PPF but they are allowed to continue the existing account till maturity of the same. they are also not allowed for furthur extension.

Thanks for your quick reply. What kind of document will adequately meet the requirements of establishing date of becoming NRI? Utility bill, bank statement? Please suggest a variety of documents as I may not have some at my disposal. Best regards.

Vivek, frankly i don’t have any idea on that. Moreover bank should be having some document list which they approve as a correct document for this purpose. I think a CA certificate or your passport entries will suffice the purpose.

I have following 2 question :

Q 1 : I have a PPF account .

So as a gurdian , can I open a new one in the name of my minor child ?

If yes , shall I contribute 1 lakh in each of the acoount . (ie, total 2 lakh)

say , from 1st account (which is in my name) i take 8Oc benfit but from 2nd account I do not want 80c benefit .

But after maturity of “2nd account” (which is in the name of my child) ,

will we get principal + interested accumulated till maturity ?

Q2 . can A person open a PPF account who is 58 years old ?

Appreciate your early reply.

Thanks,

Atanu

Yes you can open a new account for your kid as a guardian. But you can’t deposit Rs 1 lakh every year in each account. The total deposit limit is of Rs 1 lakh individually and collectively (self +as a guardian)

I think that you are wrong on this. Each PPF account has a limit of max Rs 1 Lac deposit in a financial year. If Minor is a tax payer he can also claim 80c benefit , But if Minor is not a tax payer then the Guardian can only claim 1 lac Individually and not for Rs 2 lacs. The PPF account will accept deposit of Rs1 LAC for each account irrespective of whether it is in name of Individual or Minor with same individual as guardian.

i think you can deposit up to 1 lakh in each account , but you will get tax benefit for 1 account only. if other account holder wants to get the tax benefit then they have to claim themselves.

Yes rajvi, you are right that each PPF account has a limit of Rs 1 lakh in a single financial year and if Minor is a tax payer he can also claim tax benefit u/s 80C but this is possible only where Minor is depositing out of his own taxable income.

If Minor is not a taxpayer and there are 2 ppf a/c one in the name of self and other as a guardian of minor then The PPF account will accept deposit of Rs 1 lakh for each account every year but will pay the maturity proceeds without any interest on the second account.

So to summarize the PPF rule :

CAn some one please confirm my assumption.

1 . A person can open a PPF

a. can deposit 1 lakh in a single financial year

b . get 80 c benefit

c. On maturity he will get pricipal + compound interest accumulate till the account’s life and which is tax free

2. same person can open a 2nd PPF for his minor child (who is not tax prayer )

a . In 2nd Account he can deposit upto additioan 1 lakh(on top of 1 lakh over 1st account)

b . He (gurdian) can not claim 8o c benefit

c. On maturity he(gurdian) will get pricipal + compound interest accumulate till the account’s life

and which is tax free ( irrespective minor will become adult /not at the time of maturity)

Thanks & Regards,

Atanu

Atanu…your assumption as per point no. 1 is correct. but in point no. 2 , yes you can open a seperate account for minor but your contribution in that being a guardian should not exceed rs 1 lakh taken collectively with your account. Thus whatever you deposit will be counted in your 80C savings (as the total limit of 80C is also Rs 1 lakh) and you will also get tax free maturity.

There’s no age limit on opening of PPF account.

Sir;

My son has open a PPF account in the name of Satyam in the year 2010 at State Bank Of India, Bokaro Steel City. Due to inevitable reason he has added his surname with his name. Now he is Satyam singh. All the investment has considered him and on his request after submission of proof of change of his name , his new name has been accepted. Only The State Bank Of India is not accepting his request for adding his surname with his name in his PPF account.

Please advise me ! What should I do for changing my son’s name from Satyam to Satyam Singh in his PPF account to avoid future poblem on maturity .

Thanking You;

S.K.Singh

hi,

for PPF ,

1. can i deposit my savings in any post office or in that branch only where it is opened.?

2. can we submit online in post office

regards,

jaideep

Hi Jaideep.

Post offices are not yet connected fully online. So regarding your queries

1. You have to deposit in the branch where your account is.

2. You can not transfer money online in any PPF in Post office. But yes, you can transfer your account to SBI or some other bank whcih maintains PPF deposits and then you can do online deposits in that.

Hello sir,

I want to know can i open ppf acc. & deposit 1 lakh at a one time

in jan 2013 before 5 day of the month.

Is there any rule for opening acc and deposition of money.

Thanks

Regards

Pradeep

Yes pradeep you can deposit Rs 1 lakh lump sum in single shot

Could any one please let me know whether I have to deposit money to PPF account every month or Is it ok to deposit before 5th March of financial year to get the interest. Whether the interest rate calculation starts only after 5th Match or it starts every month’s after 5th?

Thanks

Ravi

Its your choice…you can deposit money every month or in the last month of financial year, The Interest is computed for a calendar month on the basis of the lowest balance in an account between the close of the 5th day and the end of the month and the Interest is credited to the account of the account holder at the end of the year. Thus it is advisable to deposit money in this before 5th of any month. Interest will be paid as per your holding period .Means if you deposit in march then you will be paid interest for the month of march , and if you deposit in April than you will be paid interest for the whole year on that deposit

sir

i am a school teacher my employer says that my provident fund has gone into a pension plan sir can that happen if yes please give me some detain regarding that

Vishal, Some portion of employers contribution in EPF goes into EPS (employee pension scheme). out of 12% of basic that employer contributes..8.33% goes into EPF and rest 3.67 goes into EPS. So it would be wrong to say that your total balance has gone into EPS.

Please confirm me the Rate of Interest on PPF A/c from 1999 to 2012

Hi,

I opened ppf account in sbi and linked it with my sbi salary account to avail easy internet facility.

Now I have changed my job and have salasry account in another bank.I transferred my ppf account to my hometown.

the process of transffering ppf bank has closed my ppf account (stating matured account)and open a new account at my home town (without any deduction).For this I dont have passbook of new ppf account.

Can I deposite online account statement as ppf prove for Income tax proof submission?

Shruti, while transferring bank cannot close the account until the tenure of 15 years has been completed. After completing 15 years it can be termed as “matured account”.

I guess yes, online deposit statement would suffice the income tax proof.

Dear Manikaran,

Can I deposit in Post Office PPF Account from anywhere in India from any post office. please suggest anyone…

realy awesome nd nice wrk done by mr manikam . keep rockng.

am sory I mistated da name. its mr manikaran.

What is higher age limit for PPF account?

Can a Sr Citizen nominate his grandson as a nominee to his account?

There’s no higher age limit in PPF account. Also you may appoint your grandson as nominee but if he’s a minor than you have to appoint an appointee along with him.

Hi, I have 1 question.. I opened a PPF acount in the month of December 2012. As understood from the article, the 15 years calculation will start from end of FY 2012-2013 i.e 31st March, 2013. I deposited 2 times payment ( 10th december: 25,000 and 3rd Jan; 25,000) . I plan to deposit the maximum of 1 lakh before 31st march, 2013 (making sure that i deposit every month before 5th). Will it be taken in for the interest calculation ? Kindly help.

Yes, indranil. The amount deposited by you will be counted in for interest calculation.

Can I deposit more than Rs 1 lac in my childrens account. I’m not worried about the Tax Benefit

No , you cannot deposit more than 1 lakh in any of PPFs account.

PPF interest rate 8.8 % fixed or it can be reduced over the years?If increse thn no issue

Mandvi, the answer is yes. PPF rates can now be reduced and its not fixed. The rate is now linked to 10 year governemnt of bonds yield. If the govt bond yields gets reduced…it would give same impact PPF rates.

To avail the tax exemption for the current financial year via Public provident fund what are the details that one has to consider.

Like I was informed that only the current deposit amount in that financial year will be taken and not the total amount that is there in the account till date.

Earlier I use to give the updated Xerox copy of my passbook for my account. But now they have asked me to only provide the deposit slip for the current year and the previous deposits will not be taken into consideration.

Yes Harita…whatever you deposit in the current financial year upto Rs 1 lakh will only be considered for your tax saving. Neither the interest earning in that particular year will be counted for tax saving…this feature is with NSC.

hi,

a very good article. it solved a lot of my doubts. One still remains though; can i change the pattern of making the payments every year?? like make two 50,000 deposits one year and four 25,000 deposits the next year?

Yes, Anurabh you can do that.

Very interesting and informative discussion thank you. There is a point I would like to make however. Though it is true that you can deposit 100000 in a single installment, you have to be careful, because it says that to avail of the benefits the money deposited in the PPF …. IT HAS TO be out of the income of the relevant year itself. I know it sounds ridiculous but there are RIDICULOUS people sitting in government offices . Bottom line don’t put 1 lakh early in the financial year (Eg. April /May/ June) if you HAVENT AS YET EARNED that 1 lakh upto the time you have deposited the ammount in the PPF

Regards

I am going to open a PPF account. Is it OK if deposit 1 lakh before 5th march of 2014 to get the interest as well or do I need to deposite every month?

Regards

If you deposit 1 lakh before 5th march 2014, you will be paid interest for the month of march only.

It is really a very good and useful article regarding PPF account .. You have cleared my confusion ..

Thanks alot dear

Its my pleasure dewendra. I am happy that you are happy.

How bank will get to know whether the person is depositing 2 lac every year 1 lac on his name and other on his child name?

Because no one stops you while opening the account for child and no one is mapping child account with parent/gaurdian account, so how will they track?

Thanks

Thanks for the information. 2 questions : I have read that one can withdraw from PPF after 5 years . While you have mentioned its 7 years. Pls clarify

2) in case of EPF in case Ihave worked for one employer for 2.5 years and I transfer it another employer where I work for another3 years would the withdrawal be tax free

Thanks in anticaption of quick reply

You are allowed to withdraw seventh year onwards and that too once a year. Such withdrawal figure must not exceed 50% of the balance at the end of the fourth year, or 50% of the balance at the end of the immediate preceding year, whichever is less.

and in case of EPF…your account remains operative for atleast 5 years than the withdrawal will be tax free

Sir, My dad had opened a PPF a/c in 1998. He expired recently in August 2012, so now how can we process with the a/c, my brother is nominee in that a/c – can he continue to deposit the amount on my dad’s behalf so does he need to close the a/c – please advise

Sujata, your brother has to make application through form G to the respective officer along with the death certficate and other documents as required by the bank/post office where the account is. the balance standing in the credit of your dad’s account after making the adjustments of loan or withdrawal if any will be paid to your brother. He cannot continue with the account.

Sir,

My question is – My PPF account was opened in 1993. In 2004 I became NRI but continued depositing money in the account. For how long I can continue depositin gmoney in it? Also what documents are required to withdraw the total amount?

Shripad, yur account must have beenn matured by now. As you have become NRI is 2004, so ideally yo had to inform your Bank/Post office regarding your tax status. Now it seems that you have extended your account without contribution for a block of 5 years…which legally you should not.

You have to close your account now. NRIs are not allowed to extend/open PPF account.

can father’s HUF invest money in son’s PPF A/c Whether it is allowed deduction U/s 80C

I don’t think so. HUF is no longer allowed to open a PPF account and thus HUF cannot claim tax benefit on PPF deposit also. So i don’t think in your query HUF can deposit and claim the benefit.

Thanks for the clarification. However, is it possible for HUF to deposit amount in the name of Child in the PPF account and not claim exemption. i.e. The individual will deposit Rs.1 lakh in his / her PPF account while the HUF will deposit Rs.1 Lakh in the Child’s PPF account. Kindly clarify.

what will be the maturity amoount if i deposit one lakh every year for 15 years in ppf account.

Though now this cannot be predicted as PPF rate is no longer a fixed rate. It will keep on changing every year. But still from calculation point of view if i assume a fixed rate of 8% then after 15 years you can expect the maturity value of around 29 lakh

Manikaran

The write up is succint and explains clearly the common doubts faced.

Your comment on 9Dec2012 in reply to Atanu’s question

“The PPF account will accept deposit of Rs 1 lakh for each account every year but will pay the maturity proceeds without any interest on the second account”

If your above statement is true then why would a person deposit 1L/yr in his minors account for 15years only to realize that he will not receive any interest on the minors account . It would only suggest that govt is preventing risk averse people like myself from investing for my retirement AND my child’s future using PPF as the vehicle. Does this not fly in the face of what PPF should stand for.

Please confirm (again, as I still cannot believe it) whether the proceed after 15yrs for the minors account will be paid WITHOUT the interest . Or will it be paid with interest but we need to pay tax on it?

I am confused

Guardian. First of all i thank you for liking my article.

Pls find my response as below:

You have to read my answer in connection with the chain of question that was asked earlier. Actually the point is that there’s no restriction on opening 2 accounts in PPF – one as self and other as guardian of your minor child…but the total amount that you can deposit in one financial year is Rs 1 lakh only (collectively in 2 accounts). Now if by chance or by smartness you deposit Rs 1 lakh in each account with a view of getting tax free return and this smartness get caught then the authorities will return your money back without paying any interest on that extra amount.

Hi Mr. Manikaran,

Thanks for all your suggestions and advices. I have one query, I have a ppf account with SBI and It was operational about a year ago. But over a period of time due to some uncertainity i discontinued it… can i continue the same account by start depositing the way i was doing it before….??

Regards,

Abuu

9886089950

Yes, you can continue with the account by paying the minimum contribution which yo u were supposed to every year plus some penal charges.

Hi,

PPF account in private sector like ICICI is ok or SBI is the best option?

PPF is a government backed savings. ICICI/SBI act just as government agents. So just look at operational comfort for yourself and open with any bank you like.

What will happen if I deposit more than 1 lac in a financial year? Will the excess amount attract interest? Or the system will not accept anything more than 1 lac against the account? Or the excess amount will be lying without gaining any interst?

Can somebody clarify?

I don’t know about system…but you cannot deposit more than 1 lakh. If at all you open 2 PPf accounts and deposit rs 1 lakh in each without disclosing to the authorities. You will be paid your money back without interest.

Hi,

I have a question. I am 27 years old and opening a PPF account effective April’2013. This means that 15 years complete in 2029 and I will be 42-43 years old in 2029. Lets say I withdraw all the funds from the account IN 2029, that should mean that my account is closed. So, considering that 41-42 years old will be pretty early and I want to invest more for retirement, say another 15 years. can I open it again ?. Note: I know about the 5 year block option

You cannot extend your account for 15 years. But yes…as you know the block of 5 years option…then you have to do it for 3 times :). I would not advise you to close and open a new one. Though you can do it also.

Hello,

I have a query regarding the government GPF account.

My father has been working for the past 33 years in Government of Rajasthan and having his GPF account since then. Being a government job he has been transferred to various locations within Rajasthan state to various offices. So, my father is having various GPF accounts (with same account number but records at different places, I suppose) with these locations. Now, he wants to collect all these scattered records at one office location so that he doesn’t face much problem at the time of his retirement. He has been visiting the GPF office for quite long to get the records at the current office but no result (being a government office). Can you please tell me the exact procedure to follow for this situation?

Thanks and Regards.

Sorry, I have no idea on this.

I have opened ppf a/c on 17.01.1998. Pl let me know when will be the maturity due date.

31st march 2013 🙂

Hello Sir,

Want to become PPF Agent please let me know how it is possible and what are the term

Hello Sir,

How can we get maximum interest on our subscription. Either monthly option or yearly. could we get the same interest on monthly subscription (as installment) and yearly subscription.

Please reply.

The Interest is computed for a calendar month on the basis of the lowest balance in an account between the close of the 5th day and the end of the month and the Interest is credited to the account of the account holder at the end of the year. Thus it is advisable to deposit money in this before 5th of any month.

Hi, I am going to open a PPF account. Please tell me is there any benefit if I open now with respect to interest calculation or can I open an account next month?

Regards

Whether online payment for PPF payment made on 6th of the month would be eligible to get full month interest

No Mr Taneja. Fund should be there in account on or before 5th of each month.

Dear Sir,

I have started my PPF account in 13 feb 1988.

Now it is 24 yrs. I want withdraw some amount and continue the account. How much (%age) I can withdraw now and how long I can continue this account ?

If extended without contribution, any amount can be withdrawn subject to one withdrawal per year.

If extended with contribution, withdrawal up to 60 per cent of the balance at the beginning of each extended period (block of five years) is permitted.

You can continue till the time you want but can extend only for the period in the block of 5 years. This extension can be for any number of times.

Dear Manikaran,

If the maximum limit to invest in ppf is 1 lakhs( incl. minor account), Can I get a ppf account for my wife and she can also invest 1 lakh?

She as an indivual can open the ppf and invest on it with the same limit , right ??

If yes then it solves the problem for a family who wants to invest more than 1 lakh.

Pls advice…

Yes. You are very much right. If your wife is a tax payer, she can claim benefit u/s 80C. If she’s not and you want to deposit in her account from your own resources than the income out of PPF will be clubbed in your income. But since the interest is tax free , so you will not be burdened with more taxes.

Dear sir,

I am totally confused between Kotak Capital Multiplier plan and PPF account, my purpose to invest for long term and good returns. Investment amt Rs 30,000 per annum for 25 years. Plzz suggest me what would be a good option with the returns. Plzz reply

What if by way of ignorance there are two PPF a/cs opened in your name. Once you realise this, what should you do? Should you close your newly opened PPF a/c or let it be inoperative for the lock in period and continue depositing in the old PPF a/c? What is the procedure for closure of PPF a/c before the expiry of the lock in period? It would be very helpful if you could throw some light on this aspect too.

Shilpa, you just need to inform the concerned authorities (bankers or post office people) about this mistake and they will let you know the exact procedure to close the second account.

Its better to close the second account rather than making it inoperative, otherwise you will have to bear the inoperative charges also.

I have opened a PPF account on 07.03.1988 in SBI. I want to check the interest calculation by bank because those days it was manual.There seems to be error in the calculation. Can you mail me interest rate since March 1988 & formula for calculation of interest & principal amount till 31.03.2013.Also please let me know whether my below calculation is correct:

FROM TO PRINCIPAL ROI % MONTH INTEREST TOTAL AMOUNT

14.01.2000 31.03.2000 3000 11 2 55 3055

31.03.2000 31.03.2000 57000 11 0 0 57000

PRINCIPAL & INTEREST AS ON 31.03.2000 55 60055

04.04.2000 28.02.2001 60055 11 11 6055.55 66110.55

01.03.2001 31.03.2001 66110.55 9.5 1 523.38 66633.92

03.04.2000 28.02.2001 40000.00 11 11 4033.33 44033.33

01.03.2001 31.03.2001 44033.33 9.5 1 348.60 44381.93

PRINCIPAL & INTEREST AS ON 31.03.2001 10960.85 111015.85

01.04.01 28.02.02 111015.85 9.5 11 9667.63 120683.48

01.03.02 31.03.02 120683.48 9 1 905.13 121588.61

22.03.02 31.03.02 100.00 9 0 0 100.00

PRINCIPAL & INTEREST AS ON 31.03.2002 10572.76 121688.61

01.04.02 28.02.03 121688.61 9 11 10039.31 131727.92

01.03.03 31.03.03 131727.92 8 1 878.19 132606.10

10.03.03 31.03.03 500.00 8 0 0.00 500.00

PRINCIPAL & INTEREST AS ON 31.03.2003 10917.50 133106.10

01.04.03 31.03.04 133106.10 8 12 10648.49 143754.59

24.11.03 31.03.04 500.00 8 4 13.33 513.33

PRINCIPAL & INTEREST AS ON 31.03.2004 10661.82 144267.93

I have a PPF A/c opened in Dec 1998. As per above information, it matures on 31.03.2014. Can I not make any credits into the account in the current financial year 2013-14? Bank has advised that it cannot be done. If I intend to extend with subscription, then should I do it now itself, to be eligible to deposit amounts into the PPF in the current financial year?

I think bank has advised you right. You cannot make any contribution in the last financial year, as you have completed 15 years tenure on March 13. For extension of account , you have to inform your banker on or after March 14 but before March 15.

my ppf a/c is very old, open in 1994., when i went to state bank midc ahmednagar for appointment of nominee, your system can not taken my nominee. only they wrote in my passbook of ppf a/c.

reply of s b i office is due to old a/c there is no provision for nominee.

please reply,

sikchi s m

It should not happen. You better talk to the Branch Manager. else get something in writing on there letterhead.

i opened the PPF a/c in 2008-09 and deposit the amount continuously for 4 year…but forget to deposit last year i.e. 2012-13.

i read that there is a penalty of Rs 50/- for that but how i mention it in deposit slip i.e. how i mentioned that amount is for 2012-13 and not for 2013-14.

kindly help

Hi,

If my father is investing in PPF, but the money is given by Me, then in that case can i claim that as my 80C savings ? My Father PPF account is in his name only.

No brijesh. I don’t think so, that you can get 80C benefit in depositing money in your father’s PPF.

Hi

What is the tax liability, if i withdraw some amount from PPF after 8 years. As after 7 years, amount can be withdrawn with some limit. Whether this amount will be taxable under income tax act.

No tax liability. Withdrawal will be completely tax free.

Keeping note that any withdrawal after 5 years will be clubbed with your income for that year. So, basically whatever amount you withdraw from PPF, is taxable if you withdraw it before maturity (i.e. before 15 years of account opening).

My daughter is 3 yrs old. I want to open a PPF a/c in her name. My question is : Can she continue this PPF Account when she gets a job (say by 22 yrs)? OR Can she open another PPF account after getting job? Please clarify

I have a PPF account in SBI Mumbai branch, which becomes dormant because of non depositing of minimum subscription for years 2011 to 13. Now i have been transferred to kolkata. My question is ; will i have to visit the sbi mumbai branch for reactivation of my ppf account ? or i simply transfer online minimum subscription charges plus penalty charges through sbi internet banking for reactivation of the same.

Nameesh, I believe you have to visit branch once. You may also get your PPF account transferred to Kolkata if you want.

Hi

I am a NRI since 2005 but me and my wife had opened ppf a/c in the yr of 2001. now it is discontinued from 2005. So my wife wants to continue again now so pls advise the procedure .

Please contact the bank branch where your PPF account is deposit the last 8 years minimum contribution along with penal charges and your account will be activated again. But do note that you won’t be able to renew it after completion of 15 years.

I have a query I opened a PPF account this year only on 03rd of april 2013.When will it mature???

31st march 2029

If I open a PPF aCCOUNT IN SOMEBODY ELSE’S NAME ,BUT I DEPOSIT THE AMOUNT EVERYYEAR FROM MY BANK ACCOUNT.WHO WILL BE RECEIVING DEDUCTION U/S 80 C.ME OR THE ACCOUNT HOLDER???

If you open PPF in the name of your child, then whatever you deposit in that account can be claimed by u under section 80C upto Rs 1 lakh.

For any other person, firstly no deposit will be accepted (through cheque) from your account. but if at all due to ignorance they accept it, then the tax benefit will not be available to you.

hi,

thanks for the info., can i have a method to check whether my interest amount which i got was anything less than my entitlement or not. i have almost completed 15 years, i have got 14 interest entries. i want a formula or an excel sheet where i can calculate my interest.

thanks,

nagaraaja

Hi Mani,

Firstly, thanks for providing such type of great information.I want to know that ,

How can i opened my PPF account online with SBI branch?Is it mandatory to submit all relevant documents to Nearest SBI branch office or Online process?

Please guide.

Thanks,

Sah A

Sah, you have to submit the relevant documents at SBI.

Hi,

My husband has a PPF account with SBI opened in 1997 which matures this year,

I had been to the bank to submit the form H to extend it with subscription but they told me

its already extended and did not take the form.

I have read that it you don’t submit the form by default it will be extended without subscription and no deposits can be made.

Please guide what should be done.

Thanks.

Dear sir, I opened PPF account in 1990.The account had been extended twice (2007 and 2012) for block period of 5 yrs each, with subscription. I had resident status while opening account, however self status was non resident during year 2007 and 2012, as self was working in merchant navy ,the status sometimes becomes non-resident depending upon ship trading routes. Presently my status is resident and will remain the same, as self no longer working in merchant navy. Kindly advise

a)Can I continue my PPF account, as my status will remain resident for rest of my life.

b)Can I further extend my PPF account, on completion of its maturity

Siddharth, your PPF account has been continuing under resident status since the opening of account. What you did in 2007 and 2012 was wrong, but right now you are resident and as you said you will remain resident now onwards. So i believe that you can continue with the account. But still it would be better to inform and consult the branch manager of the concerned bank or post office where you have your PPF account.

A person opens a PPF account at the age of 20 yrs and closes the account on maturity aftet 15 yrs. Can the person open a new PPF account again at the age of 40 yrs?

Yes, a person can open a new account at any age, but after getting the earlier account closed (on maturity). Its always better to continue with the earlier account as the lock in period reduces to 5 years. If some one needs liquidity then he/she can make partial withdrawal or take a loan as explained in the article above.

Would like to know whether the amount received by the nominee on the death of PPF subscriber, is TAXABLE or not

Its completely tax free even if recieved by nominee

Thanks for the information. Regds Ashok

If a grand father deposits some amount in his minor grand-child’s PPF account, who can claim tax benefit under section 80C ?

No one can claim the tax benefit in this case, neither grandfather nor parents of child

Sir,

You have provided a lot of information on PPF. Thanks for the same.

Plaese intimate the interest rate on PPF w.e.f. FY 1998-1999 to till date (seprate for each FY and specific dates on which Interest rate either reduced or increased)

Thanks & Regards

Mr Singal…you will get your answer on this link http://en.wikipedia.org/wiki/Public_Provident_Fund_(India)

Firstly, thanks for providing such type of great information.

I have extended my PPF account on 01.04.2011 for firther 5 years.

As on 01.04.2013, the blanace at credit was Rs.4,28,000/-. I wanted to make a withdrwal of Rs.2,50,000/- in Oct., 2013 but Postal department allowed an anmount of Rs.6,000/- only taking the plea of PPF rules.

Any how, I forgot to make any contribution during FY 2013-2014 and this fact has come to my knowledge on today only. what will be consequences:

Whether i will be allowed to make contribution for FY 2013-2014 on 07.04.2014 with some penalty amount as in case of LIC.

YES/ NO

if Yes, plaese intimate the amount of penalty. However, i want to contribute only Rs,1000/- in above PPF Account.

if No, whether i will get interest for FY 2013-14 on my amount in PPF account as on

(i) from 01.04.2013 to 24.10.2013 = 4,28,000

(ii) from 24.10.2013 to 31.03.2014 = Rs.4,22,000

Please guide.

Thanks,

You seem to have extended your PPF a/c with contribution, but in that case you are eligible for withdrawal of 60% of the amount standing at credit at the beginning of financial year in which a/c was extended which in your case was 1.4.2011.What i don’t understand is that when you wanted to withdraw 2.50 lakh, how did you settle at mere Rs 6000/-?

Regarding your second question. See as per PPF rules, you will be charged with penalty fee of Rs 50/- for each year of default along with subscription arrears of Rs 500/- per Financial Year. As you want to contribute only Rs 1000/- , So you can pay Rs 1050/- to regularise your PPF a/c.

Interest would however continue to accrue.

Hi Manikaran,

First of all many many thanks for this amazing article regarding PPF. I have studied it thoroughly and all the queries and comments as well. I have no doubts but need some advice, and if you guide me then it might actually help a lot of people of my age to plan well for the long term.

– I am a 26 years old software engineer. I am planning to open a PPF account with ICICI bank(since I already have a savings account with them) and would like to invest 2000-5000 every month at least for the next couple of years and increase it slowly based upon the income I earn every year. I plan to invest in such a way for the whole of 15 years I can get tax exemption and also accumulate substantial corpus so as to meet future expenses which of course will be hard to meet. Hence, please answer a few below questions and I would like to thank you for your guidance and patience-

1. I am not very keen to take high risks by getting into Mutual funds(at least for now), hence is the current PPF interest rate of 8.7 good enough and how is it expected to behave in the coming years?

2. I am planning to open a PPF account from May, 2014. How much time in days will it take to activate an account(say in ICICI bank) once I submit the required documents. Will It be active on the same day I visit the bank? Or else, if it takes a few days to get activated, I will go ahead now itself before May arrives.

3. Finally, considering my age and profession, what others options do you suggest me to invest on in the coming year apart from PPF (with the same investment of say 2000-3000 per month) with a little risk profile so that I can get good returns in 5-15 yrs time?

Thanks in advance once again.

Thanks a lot for your appreciation Rajshekar. I am glad that youngsters like you read, like and act on the advises given on my blog. And also are concerned about there future and financial planning. I am happy to answer your queries:

1. I totally understand your apprehensions on risky investments like equity mutual funds. take your time, learn about these more and then only invest. You cannot ignore equity if you really are looking for wealth generation. Regarding PPF interest rates, see it is already on higher side. I was expecting it to come down last year, but i guess because of doing away with the agents commission in PPF, the rate was increased a bit. This Financial year also it doesnot seem to come down, but yes going forward you will see the downward movement may be from next year onwards. as G sec rates are bound to come down and government is raising money at very high rates so with some more RBI steps, infaltion should come down and so would interest rates.

2. It takes few days time.

3. As you are not interested in getting into equity which i feel would have been much suited to your requirement, i would advise you to go with long term debt funds. These funds may not give you good returns in short time frame, but when you find PPF interest rates going down you will find good returns in these funds . So these will balance out your portfolio.

Hope i was of help. And yes, if you like my articles then do share it among your friends and like us on facebook too

Well. Manikaran, thanks for your expert comments once again. Based upon your replies to my above questions, now I would like to inquire about a couple of more things-

1. First, let me explain my situation to you. I have been working for the last 3.5 yrs in IT industry and I had changed my job in December last year. And instead of transferring my PF from my old employer to my current employer, I had withdrawn my entire PF to meet an urgent expense. So, literally speaking I have no savings in PF till now which is why I want to open a PPF account along with my current EPF so that I can make up for the lost savings(till now) as soon as possible. However, considering your reply- “but yes going forward you will see the downward movement may be from next year onwards. as G sec rates are bound to come down and government is raising money at very high rates so with some more RBI steps, infaltion should come down and so would interest rates”..Is my plan of opening PPF the right step to accumulate some savings over the long term(inspite of knowing the fact that interest rates will go down)?? Please advise.

2. I am a keen follower of equity funds and yes, but I am apprehensive about them because I am not too sure exactly which fund I should invest in since my current financial situation is not so great where I can take undue risks(at least as of now). I want to gain sufficient knowledge before jumping into this boat. Would appreciate your effort if you could guide me in this respect. Should I wait for about a year before getting into equity or can I start off slowly now itself(by investing small amounts, saying Rs. 2000 every month)? If yes, please let me know the best equity funds for me?

I hope you would have got a better understanding about where I stand right now and advise me on 2 kinds investments I should start now. I am sure you will give good advise on this so that I can maintain a balanced portfolio and meet my long term goals.

Thanks in advance once again.

1. See , as PPF is no longer a fixed return investment so the rates will keep on changing Year on year. But this should not stop anyone from opening PPF a/c. This is a good instrument to generate long term returns and that too tax free. So do go for it.

To manage the impact of interest rate s going down on your overall portfolio i suggested debt funds which will generate more returns in falling interest rate scenario.

2. You need to be sure about equity before getting into any equity fund. Though i can advise you few funds but you have to be very disciplined in continuing with it. You have to make it a part of your total portfolio and not just look at it a separate equity (risky, market linked) investment. You have to promise with yourself that you will stop watching stock market just to make sure that your investment is doing right. And all this is actually a difficult behavioral change which i am asking for.

So better to start with a balanced ( mix of equity and debt ) product like HDFC Balanced. But be sure that it is also not devoid of volatility. Be patient and give time to your investments to grow.

How do I change my name in ppf account, I am a male.

pls explain in detail

How do I change my name in ppf account I am a male? .

I have changed my name legally,now I want my ppf account on my new name what is the procedure,

Thanks

Then you must have got your name changed in all other important documents like passport, Pan card…just take these documents along with . Though i don’t know the exact procedure but i guess they will ask for an affidavit and indemnity also along with these documents.

You should confirm this from the post office/bank where you have your PPF account at

Hiiiiiii……….

I have a query Regarding the Minimum and Maximum Deposit limit……

Can i deposit Rs.200000/- per month in one PPF a/c ???????

Rahul , the maximum deposit limit in PPF has recently been raised to Rs 1.50 lakh per annum. You cannot deposit Rs 2 lakh p.m

Sir, I am govt. servent and i am having GPF contribution and investing 1 lakh per annum. Recentely I open the PPF account in Joint name of My son and me and start investing another 1 Lakh per annum in PPF account also. My question is that can interest recieved from Both GPF and PPF account is tax free? can both the interest recieved from the GPF and PPF exempted in the annual return

In both the investment options you don’t recieve interest but it gets accrued in the product itself. Whatever interest gets accrued is tax free in nature.

Sir I want to ask one serious question.

I m doing CA n my sir told that during the last five years of PPF we should deposit less amount not 100000 .let say 5000 or 6000 because after 15 years when total amount of last 15years will be shifted to your account than income tax can ask you to show from where this big amount has been credited ..so when you will show last 5 year ppf deposit. It will be less than 35000. So iT officer cannot check income tax returns from more than 6 years..In dis way nothing can be question. .

Please put a light on it..

Sajan, one thing i don’t understand that when you are doing a genuine transaction then why should you be worried of income tax department.

PPF is meant for long term savings, and it generates tax free income. Even Income tax people knows it. If you have been saving in a product for last 15 years, you are bound to get big sum of money.

Help people save more for there goals and let them lead a happy life. You should not be scared of IT people, if your transactions are legal.

I have a running PPF a/c since 1990. I have never extended the account after 15 years. I am still continuing the account by depositing the subscription in every year. I came to know that it is required to extend the account in every 5 years after completion of 15 years, which I have never done. Kindly advice me:-

a) What is to be done now.

b) Will I get the interest for the balance period after 15 years (From the year 1005 to 2014)?

c) What can I do for Continuing / Closing the account?

Hi Sir,

Thanks for your good article. I heard depositing money in yearly basis earns interest more . I have opened my ppf account on month of october how do i deposit my money yearly

Satheesh thanks for appreciating my article. See, its not a question of depositing yearly or monthly. But it is about investing in lumpsum or in parts. This is no brainer that if your invest Rs 1 lakh in lumpsum in april will surely earn more interest, then investing Rs 8000 monthly. PPF a/c in itself doesn’t restrict any one to deposit monthly or yearly, its completely your choice. What it requires is atleast one deposit per year.

dear manikaran

i have 4 ppf accounts

one in my name , one in my wife’s name and 2 on minor children’s name – the collective deposit is rs 4,00,00

my wife opened her account when she was working , she had deposited from her savings for four years .thereafter discontinued as she chose to be a home maker, i continued the ppf by depositing 1,00,000 from my savings and kept the account live

both the children have now turned major and my elder son is now a tax payer , younger son is pursuing studies and has no income of his own . the accounts are maturing next year . we have already brought to the notice of the post office that my children have now become major and that they would operate the accounts themselves . can you please clarify on the following

1. can i continue deposit in my wife account without claiming the benefit under 80c , what happens to the proceeds on maturity

2. what happens when the amount is with drawn by my children next year

3.in general if the amount is not with drawn on maturity and at the same time not extended , will the amount continue to earn interest – can the total amount be drawn any time after maturity, but within 5yrs, if it is not extended

rgds

murali krishna

Pls find my replies in line

1. You can continue depositing amount in your wife’s account. This can be called as gift to spouse which is tax free in the hands of spouse. But the law says that if wife invest this amount and earns income out of this gift then the earning portion will be clubbed in the income of the giver. So in your particular case even if the income out of your wife’s PPF gets clubbed in your income, it will not make much difference as the interst on PPF is tax free.

2. Nothing. This is their money now. and the best part is that the amount will be tax free. But its better not to withdraw, they can use it for their tax saving in future. Continue the account by extending it for block of 5 years.

3. You may extend the account for another block of 5 years without contribution. In this case If extended without contribution, any amount can be withdrawn subject to one withdrawal per year.

Hope it has cleared your doubts

dear Manikaran Singal

thanks for the prompt reply , which has put to rest lot of my worries

under point 2 – thanks for the suggestion to remain invested , unfortunately the amount is required for their education and hence may have to be withdrawn .They will open a fresh account as and when they can afford

under point 3- will the account continue to earn interest

rgds

cmk

Thats great Mr Krishna, I am glad i was of some help.

I suggest not to withdraw the complete amount so to let the account in operative state, which you can use later on for your requirements. and Yes account will continue to earn interest as long as money is there.

please read the amount as 4 lakhs , 1 lakh in each account

my wife has PPF account in SBI, We have joint account in same SBI branch , Can I linked The PPF account to my account in same SBI branch .so i can esily transfer fund to my wife PPF account By net banking

Since you have joint account in SBI, there will be no problem in transferring amount to PPF account of the SBI by net banking

I have opened ppf account in june 2001 till which year i can deposit the money in the accn prior to maturity

Dear Manikaran

Thanks for this very informative article. I have one query

My son is an NRI who has a PPF account opened before he became NRI (in 2012). Can his account be extended beyond lock-in period of 15 years. Is the interest accruing on the deposit taxable in US

Regards

Rakesh

Dear Rakesh

The answer is NO. Your son cannot extend his PPF account beyond first 15 years. IN US he has to disclose all his investments globally and technically yes, his income from PPF could be taxable over there.

I own a PPF account since 2003. Can i open a PPF account for my son and myself as a legal guardian

2) can deposit the 1.5 lakh on each PPF acc ( my acc and my son acc).

Note : I am using PPF for investment purpose not for tax exemption.

As i checked in many site around web and nowhere i found proper solution.

Some one said that 2 acc ( self & minor) can be maintained but collective deposit shall not be more than 1.5 lakh ( i.e self 80 k + minor 70 k = 1.5 lakh). Is it true.

Or we can deposit 1.5 on each PPF and also avail interest benefit on both.

You can open PPF account in the name of your son with you as guardian, but the total collective deposit in a single year in both the accounts should not increase Rs 1.5 lakh. What you’ve read is correct.

Please brief me about the SBI money back gold plan.Do we opt it or not 12 yyrs plan with saving of 30 k pa

can ppf deposit claimed by assessee onbehalf of major son or grand son

i have open ppf a/c in 2006 & can i partial withdrawal from my ppf a/c in march 2016 & April 2016? and how it is calculated for two consecutive year,

Thank & Regads

Amit

Dear sir,

I have deposited in PPF presently i would like to withdraw the entire amount from my PPF account towards my mother knee replacement surgery

Pls advise what is the procedure and what is the limit

rgds

raja

Few days back, government has come up with guidelines on premature closure of PPF in specific cases. You better visit the bank or post office where your account is and confirm the documents which you need to submit for your requirement.

Manikaranji you have explained everything related to PPF very soundly but still i have a query little bit different,

1. Can my Father-In Law deposit in my already tax payer wife account 70,000 which is her daughter and Grand Son/ Daughter’s 80,000 PPF account like and claim the rebate.

2. Can my Brother – In Law deposit 1.5 lac in his already tax payer sisters account and claim the rebate of 1.5 lac

3. Can my brother in law deposit 1.5 lac in his nephew account who is minor and claim the rebate of 1.5 lac in income tax and have the benefit of it.

Thanks

1. No he cannot do this directly, and also cannot claim any tax benefit. But yes he can give money directly to his daughter and grandchildren, which can further be deposited in their respective PPF accounts. Here your spouse may claim tax benefit.

2. NO.

3. No

I had started an PPF A/C in a post office belongs to one state. Now I am going to settle in another state. Is it required to transfer the A/C also to the state which I am going to settle. Can I operate the A/C any where in India ??

I HAVE A QUERY WIH REGARD TO PPF i.e IF GRANDFATHER PAY FROM HIS BANK A/C THE AMOUNT OF PPF FOR HIS TWO(MINOR) GRAND DAUGHTERS,THEN WHAT WOULD BE THE ACCOUNTING EFFECT IN BOOKS OF IN BOOKS OF GRANDFATHER. AND IF GUARDIAN OF ONE DAUGHTER IS FATHER AND MOTHER IS GUARDIAN OF ANOTER DAGHTER.WHAT WOULD BE THE ACCOUNTING TREATMENT IN BOOKS OF MOTHER AND FATHER

Money from Grandfather to Granddaughters in their PPF is counted as a Gift. But PPF rules will remain the same as respective guardians cannot make more than 1.50 lakh of investments as total of self and kids account including this gift amount. No one can take tax benefit of this gifted amount.

Hello sir,

Why entry in PPF passbook is manually.

What kinds of statement of PPF we can take from bank of Baroda every year.

Not sure. You need to check with bank of baroda people

dear sir today byfault i have sent 100000 RS to my sbi ppf account which is in same bank .sir i want to add only 10000rs but sir byfault it happens .so sir what can i do withdraw my money plz hell .is it anyway to withdraw my money whole?partially right now plz reply

Unfortunately, nothing can be done now. Once the money is deposited into the PPF account then you have to follow the PPF withdrawal rules or take Loan on PPF

Hello sir

Question 1 : Will the compounding year be calculated as per my date of ppf account opening or the bank’s financial year?

Question 2: I have openend my account on mid november this year.Should i close it and reopen by march-april next year to get more benefits, so that i can invest all money at once in first week of april?

1. Your date of PPf account opening

2. Nope. All is well 🙂

i have opened my account on november 2017. will i have to deposit by march 2018?

i have deposited one amount only on march 16 2018? will i get any interest?

Sir i will appreciate if you can guide me in choosing car loan or PPF withdrawal because i want to buy a car . my PPF is maturing on 1 apr 2018. My matured amount will be approx. around 11 lakh, kindly suggest that should I apply for car loan or withdraw money from PPF account .

This is not a one-line answer. I do not know anything about your other financials, goals and requirements. In my view, you should better get your financial Planning done to have this answer.

On the face of it, it does not make sense to withdraw PPf to buy a car, but this is also not wise to buy a car on Loan. So this calls for understanding your complete financial situation.

Sir can I withdraw my ppf account in June as it has completed 15 years and will I get interest up to June and can I open another ppf account in same name in July same year?

Hello,

Again the law is changed.. NRIs can still contribute to PPF. But NRIs cannot open PPF.

Raj

i deposited 1,50,000 for ppf via clearing cheque in bank on 28.03.2018. but bank clerk wrongly entered as 1,00, 000 in 28.03.2018. but in bank rectified may 10th 2018. how i can show this entry in last financial year and i can only deposit 100000 for 2018-19 .

It’s a mistake at bank’s end…they have to rectify it in their records

If the bank, where I have PPF account, becomes bankrupt , the SB accounts, FDs in this bank will be governed by DICGC rule and the holder of these SB and FD account will get only up to Rs. 100000 /= ( one Lakh) from their account. What happens to PPF account holder, will he also get only Rs. 100000 ( one lakh) or whatever is balance in his PPF account ( even if it is say 2500000/ ( Twenty five lakhs) ?

PPF should not be impacted with bank’s default. It is under Government’s Ownership.

Sir,Actually I had opened a ppf account in sbi last year. But unknowingly I have opened a ppf in post office last month. But after opened the second account I got to know that there would be one ppf account per person. In second account I have diposited 50k. Kindly suggest what can I do?

How to close 2nd account withdraw my money or any better suggestions. Thanks

You better talk to the Postmaster , infact write a letter to them so you have their written reply on this.It is wise to get your account closed. Generally PPF is not allowed to be closed in the system, so the Bank/PO may like to avoid this and may want you to aproach the other Bank/PO where your first account is, so here the written reply on the same would be of help.

Sir ,I had opened a ppf account last year in sbi.but unknowingly last month I have opened a another ppf account In post office. But after opened the second account I got to know that one person can open one ppf account. But I have diposited 50k in 2nd account. Please suggest me what can I do or how to close my 2nd account and get my money.thanks

Hi

I had opened my PPF account in Jan 2014 and have been depositing 150000 in it yearly. Will I be able to do partial withdrawal on it as on 1 April 2019 ?

Yes

I already have one PPF account in my name and one more in my wife’s name. Can we open another account for our minor kid where one of us can be guardian?

Yes, you may open the same. But you cannot deposit more than Rs. 1.5 Lakhs per year combined in the child and guardian account.

I’m often to blogging and i in actual fact respect your content.

How much amount (Max) can be deposited in an account eg

father and his minor sons account(UNG) Combined in a financial year? OR

Can 150000 be deposited separately in both accounts father and his minor sons account in any financial year?

Dear Narender,

You cannot deposit Rs.1.50 lakhs separately in both the PPF accounts. The maximum amount per financial year in both the accounts combined, cannot exceed Rs.1.50 Lakhs.