When it’s a question of your child’s future, you always aspire for the best. You want to provide her the best education, comfortable lifestyle; grand wedding. Some also want to buy their kids a house, when they grow old and also want to support them in settling down in their business by funding every now and then.

To get what you want you have to have a proper plan at place, which can be worked upon. Planning towards your dreams sometimes sounds like a daunting task, but the insurance advertisements of Child plans makes everything look so easy that just by investing in those policies one can achieve all that he wish for. The word child attached to the products provides necessary emotional appeal and the word “Plan” sounds as a properly laid down process.

All this makes you feel confident in the hands of insurer even if at a later stage you come to know that you should not expect much out of such investments. You don’t surrender these products due to 2 reasons – one the investment was for your child and you are emotionally attached to this , and the other reason is that you are loss averse i.e. you don’t want to come out of any product on loss and want to stay with it at least till it regains the capital value.

This is not a hidden thing that the product that appeals to you emotionally, you stay invested longer in it. Your emotional attachment brings the necessary discipline in you and you ignore all kind of arguments against that product and also take efforts to adjust your cash flows so you can honor the premium payment on time.

Taking note from this behavior, many years ago even Mutual funds houses tried their luck in this segment, by launching children plans. The idea was to bring the required emotional appeal in the product to convince investors to invest more and stay longer.

With the increase in flow of information and financial planning slowly gaining importance, investors have started realizing that Insurance cum investment products don’t serve any purpose, neither of adequate insurance nor of decent returns and this is why Mutual funds are coming up as better investment avenue. And this is also due to the recent rise in the stock market that people feel that mutual funds can be good investment options to make them more money. You consider mutual funds as money making product and insurance plans as saving and safe product…no?

But all said and done, bringing discipline into investments needs some emotional attachment with the product. So now people have started looking up to these child plans of mutual funds. Let’s first understand what these child plans of mutual funds are all about.

What are Child plans of Mutual funds?

Technically these child plans are nothing but hybrid mutual funds having different asset allocation pattern as per the investment objective and structure of the scheme.

Some of these child plans are equity oriented i.e. having more exposure to equity and thus meant for long term investments, and some are debt oriented meant for conservative investors.

To make people stay longer in these funds where the name plays its part, these funds also has high exit load which also restricts investors from coming out early. Also there is one added feature of free personal accident cover which is provided to the parents of the child.

Performance and other features of some Children Mutual funds schemes.

There are around 8-10 children specific mutual funds scheme in market, but I will take only some popular names in consideration. Besides the funds mentioned below there are funds from LIC Mutual fund, SBI Mutual fund, Tata mutual fund etc. under this category.

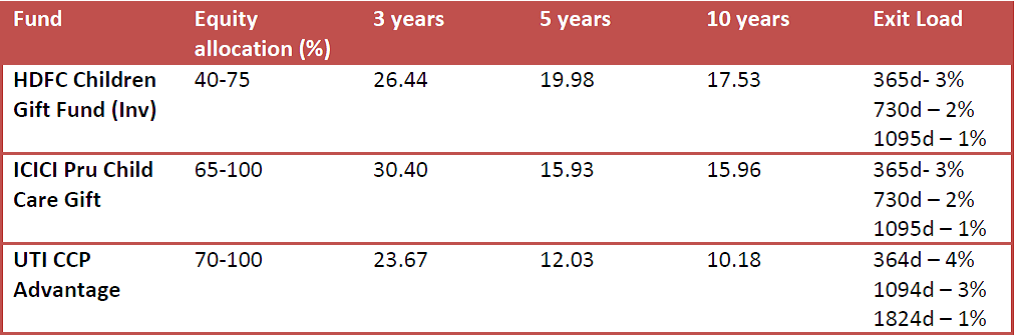

Performance (In CAGR) of equity oriented child plans of mutual funds

(Source: Value express FE, Dt: 23-12-2014)

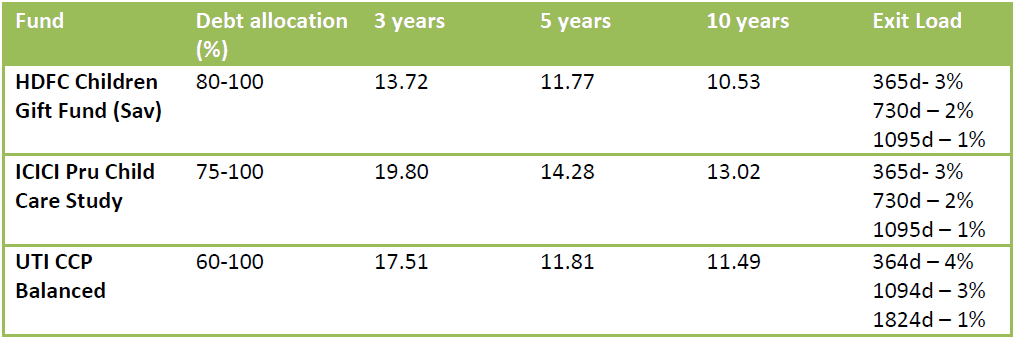

Performance (In CAGR) of Debt oriented child plans of mutual funds

(Source: Value express FE, Dt: 23-12-2014)

From the above tables it is quite clear that these funds have given the impressive long term performance. Even debt category funds are notable. Comparing the after tax returns with traditional saving instruments like Bank Fixed deposits and post office scheme, debt children mutual funds schemes looks very good.

Conclusion: what should investors do?

Child plans of mutual funds are diversified hybrid equity and debt oriented mutual funds with a specific emotional appeal with it. Performance wise these funds are comparable to their specific category like Hybrid equity oriented or Hybrid debt oriented.

I believe that more than the selection of funds it is the process and discipline that takes you towards your goal. If regular investment has become your habit and financial planning is your second nature then you may invest in any good average fund as per your acceptable asset allocation. But when you know that you need that emotional kick to stay invested with the fund or some reason not to withdraw from the investment, then you may consider these child plans from Mutual funds.

( Read : mistakes to avoid while planning for children education)

I feel that Hybrid fund should be invested into for a single targeted goal and children mutual funds scheme surely answers that requirement. These are definitely better than the child insurance plans, performance wise and cost wise, provided you are adequately insured through term life insurance plans.

Did you ever invest in child plans of mutual funds or have any experience to share regarding child insurance plan, then pls do share.

{kind=link}

Hi

Nice blog on securing child’s future. I have one question on securing the child’s future, please try to reply my question.

I had been investing via SIP-growth option in two large cap oriented equity funds FT India Blue Chip and DSPBR Top 100 since from 4 yrs and I have especially alligned these two funds for my two kids aged 1 yr and 6 yrs for their education and marriage which is a fin goal. going to occur from 10 -20 yrs from now. Is this the right move. I mean allocating the above fin. goal (non-negotiable goal) in a large cap oriented equity fund. I think most of the FP says non-negotiable goals should be allocated in large cap fund to minimise volatility. Can you pls comment of this?

Please note I do have a seperate multicaps equity funds for my retirement which is going to occur more than 20 yrs from now.

Thanks Satish for liking the post. Do share it with your friends too.

Regarding your query, the saving strategy looks fine to me. Allocating in Large cap or mid cap funds totally depend on how tolerant are you to volatility and the time horizon of investment. To manage the non negotiability of the goal planners always advise to come out of equity atleast 2-3 years before the target year. If mid cap is volatile then large cap is also though less than mid cap, but on the other side volatility of mid caps comes with potential to generate big returns where large cap lags behind.

So keep your expectation less, do regular investments and stay invested till your goal. Your goal will be achieved comfortably.