Post Updated on 31.03.2017

Max Bupa health insurance has a unique one of its kind product called Max Bupa Family First. Its uniqueness is in its feature of provision for covering 19 relationships of a family in a single plan. Max Bupa family first comes in 2 variants – Max Bupa heart beat and Max Bupa health companion.Relationships can be parents,

Actually Heart beat and Health companion are 2 main products of Max Bupa health insurance, it just to make it suit to different requirement, both of their features are added into Max Bupa family first structure.

Let’s understand Max Bupa family first in detail with comparative analysis of its both variant under Max Bupa heart beat and Max Bupa Health companion.

Max Bupa family first – in brief

Basically, this is an extended version of Max Bupa health insurance family floater policy. In a family floater policies generally, the maximum of 2 adults with the maximum of 2 kids (some policies cover 3 kids also) are covered but in Max Bupa family first you can get 19 relationships covered under a single plan.

Max Bupa family First – List of Relationships that can be covered

| Self | Grand Father |

| Spouse | Grand Mother |

| Son | Grand Son |

| Daughter-in-law | Grand Daughter |

| Daughter | Brother |

| Son-in-law | Sister |

| Father | Sister-in-law |

| Mother | Brother-in-law |

| Father-in-law | Nephew |

| Mother-in-law | Niece |

As compared to floater plans in Max Bupa family first there are 2 types of covers, one is individual which is available to every member separately and other is floater which anyone of the member can use after exhausting his own individual cover.

This is where Max Bupa Health Insurance is pitching its USP but as a buyer, this should not be the only feature your decision be based upon. There are many other features which demand your attention

Max Bupa Family first – basic features

Max Bupa family first features vary with product variants – Max Bupa Heartbeat and Max Bupa Health companion. When Max bupa health insurance was launched in India, it came up with only heart beat version, but later on looking at the Indian requirements and also to provide economical version of health insurance and remain competitive in its pricing, Max bupa Health companion was announced, and also added health companion features in family first too.

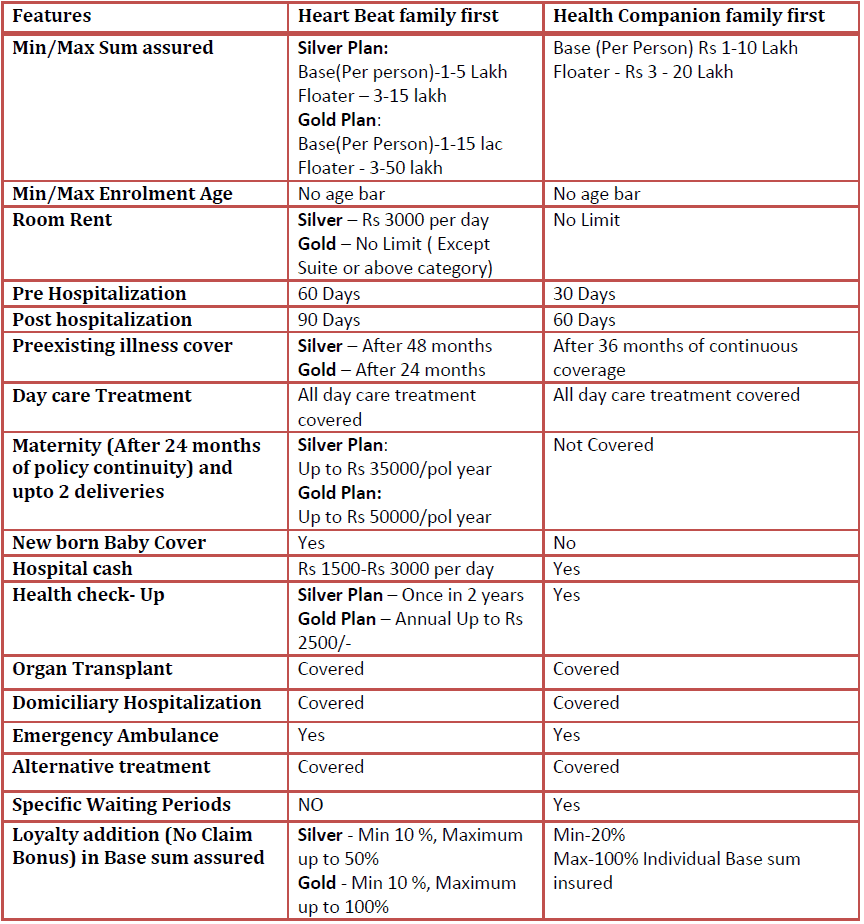

Below table will give you a comparative analysis and also understanding of basic features of Max Bupa family first – Heart beat and Max Bupa Family first health companion.

Besides above, Max Bupa family first heart beat version has one more variant as Platinum, which has a kind of premium features like High sum assured, OPD cover, additional child care benefits, International treatment of specific illnesses.

These are high end features, so if you are looking for a policy with basic cover and affordable premium, then better not get into platinum features. Else you may go through the policy brochure (Click here to download).

Max Bupa Family First – Should you Buy?

As I wrote above that Family first is a product structure where one can cover up to 19 relationships, whereas the features are of heartbeat and health companion only. So if you want to buy respective products on individual or family floater basis then you will find the same features there. However, the benefits may vary depending on the sum assured.

The main attractive and different feature in Max Bupa health insurance policies is that it does not reduce the “No claim bonus” based on future claim. Which means that once No claim bonus is added into your policy, then your policy coverage would not be reduced.

The other good feature that is available in the Max Bupa Heart beat version is that it does not have specific waiting periods, means you are fully covered after the initial waiting period of 30 days. This is one of the main reasons of high premium of heart beat plan.

I just feel only one issue with Max Bupa family first, which is that when you add members from all age brackets into a single plan, then sometimes your overall premium outgo gets increased, as the premium is calculated on the basis of higher age person. But on the other side since the floater cover is the common cover among all, so it should reduce the overall premium. Thus one should compare the premiums in different permutations and combinations

But on the other side since the floater cover is the common cover among all, so it should reduce the overall premium. Thus one should compare the premiums in different permutations and combinations.

Also, there is different zone variations too in health companion product, which one should be aware of while buying the policy…and i am sure that zone conditions would be applicable in Family first too.

Overall I find Max Bupa health insurance is a good company to buy health insurance from. One should be aware of the product features to the T to buy a suitable product.

{kind=link}

Nice and detailed review manikaran. Thanks.

I have one question – My age is 33 years. I have one policy from apollo munich covering me, my wife and 2 kids with Rs 5 lakh separately. I am paying premium of Rs 19900/-. Does it make sense to port my policy to Max bupa family first….since your review shows very attractive features from max bupa. Pls advise

Thanks for liking my article raghav.

As i wrote in the article that for high end cover this product definitely provides a cost effective and much beneficial offering. In your age group this product definitely looks attractive , but do keep in mind that going forward max bupa has a feature of asking co pay in the claims after 65 years of age.

My mom is 58 years old. She doesnot have any health problem. Which health policy is suitable for her. I am looking for a sum assured of 5 lakh.

Saloni ji,

You can select among following policies.

1. Religare Care

2. Apollo Munich Easy Health

3. Icici Lombard CHI

4. Future Generali Individual

5. Star Health mediclassic.

A very nice detailed review of the policy.

I was thinking about porting to Max Buper Family First. However, I needed some help and guidance if it would be advisable for me to do so based on the below information.

We are a family of 3 (41 yrs, 41 yrs and 13 yrs)- I have a policy from Ifko Tokio for 3 lacs each and a four year old policy with New India Assurance for 5 lacs each. Five yrs ago my wife was treated for breast cancer wherein the claims were paid by Iffko Tokio and from the current year New India would also be covering the pre-existing.

Based on the above, would it be advisable for me to cancel my New India Assurance policy and port my Iffko Tokio policy to Max Buper Family First wherein the SI is 5 lacs each + a floater for 15 lacs. Also while porting, would all the pre-existing be covered from day 1 in Max Buper. Secondly, while go thru the reviews for max Buper – not many have recommended this company. It seems there alot of issues for cashless and also for making claims after hospitilization.

Your advice shall highly be appreciated.

Ram

First of all thanks for your appreciation.

Based on the facts you have presented, i believe that you should stay put where you are. As after getting Treatment of breast cancer, it would be difficult for your wife to find out a company which accepts your case. Portability benefit is there but the acceptance of the case is no binding on new company. it may reject your proposal based on pre existing illnesses and own underwriting. You may try but it is a difficult case. I hope that the treatment of breast cancer was disclosed in the new india policy, as policy is 4 years old and treatment is 5 year.

As far as claim servicing is concerned, max bupa is a good company. ( as far as my experience goes)

Namaste Sir,

My age is 30yrs and my wife is 27yrs. I am planning to take Max Bupa Family First ( 5 lacks for each and 15 lach as floater). I found premium as Rsa.10263/p.a. which is very high as compaire to Religare care and Appolo munich Optima Restore. I heard about Max bupa that they use to increase premium amount in future so high that you could not pay that. Also the SI in floater ( 15 lack) you can use only for major and critical illness. I want to know at what extent a company can increase the amount of premium in future.

Also kindly give your valauble suggestions regarding Max Bupa Family First, Religare care, Appolo munich Optima Restore as I am confused between these three.

Yes Ritesh. Max bupa’s premium chart does not have any slab structure. They have rates for every age, which means your premium increases yearly with age. The floater part of the policy you can combine with any hospitalization, there’s not any condition of critical illness. To check the extent to which company can enhance its premium , you may visit the company’s site and chk the premium rates for different age yourself, to have the clear picture.

See, plan wise and services wise all the companies are almost same and comparable, you may check the religare review on this blog itself. Premium wise after the age of 65, max bupa’s premium will come down as compared to apollo and religare as the co payment feature of 20% gets activated in that age. rather than getting confused, go ahead with nyone which looks affordable to you.

Thanks for the advice sir.

I decided to go with Religares Care plan. Thanks again.

Namaste sir,

My age is 22 years. I want to take the policy for my parents aged 46 and 41 years..

I am considering 3 products…

1. Oriental Family Floater (As Premium is Rs. 13K approx for 6L SA, if I am as Primary Insured)

2. Religare CARE

3. Apollo Munich Easy Health Standard..

In Apollo optima restore Premium Is very high..

With the bless of God, My Parents have no diseases till now…

Please Guide me In choosing the right option..

Shashank , to me all the policies mentioned are good. Orieantal policy has some sublimits in it ,where as Religare and Apollo has no sub limit. But still Rs 6 L of sum assured, may sort out the sublimit issue too. Just go through the policy wordings once again and understand the restrictions , and if acceptable, then go with any policy.

Hello Sir,

After comparing policy available in the market, Family First from Max Bupa comes out to be fine for me (along with my Wife and Father ) on papers. But not sure about the claim settlement ratio and cashless approval time. Request you to please advice me on same.

Also, while having a discussion with the sales representative of Max Bupa, he gave me in a written mail, that the 20% of Co-Pay is applicable only to person who at the time of enrollment are greater than age of 65 as policy allow enrollment till any age. It is a false promise he is making?

No Saurabh, that guy is misleading you. Its better you should ask for the policy wordings and tell him to show you where it is written.

Dear Saurabh,

Max bupa has compulsory 20% co pay for any insured member , once he turns 65 yrs old. It has no relation with age of entry.

Hello Manikaran,

Thank you for the post. Very informative on the product.

I was on call with a representative from policy bazaar for like 2 hrs today exploring best available health insurances that covers critical illness, cashless hospitalization for my parents. At the end of the call i was convinced that the MAX BUPA Family First Silver is the one. Before i went and purchased it online i thought of doing a bit more research on the internet. The rep i spoke to did not mention about the 20% co-pay for the claims post the age of 65 yrs.

My Dad is 60 and Mom is 54 right now. My Mom is a diabetic which we found out like 6 years ago. But she has been on controlled diet, hence her sugar level is in check. Dad is healthy with minor niggle in the knee and such. Would you recommend this policy to me? I agree that the premium is bit on the higher side and i am ok with it however 20% co-pay is something i am bothered about. Do you have any other recommendations which suits my need?

Also could you please suggest a policy that best suits me(28) and my wife( 24) with no kids yet.

Thank Vikram for your appreciation on my post.

See, you cannot avoid Co payment if you are entering in any health insurance product after 60 years of age. Mostly all policies,has co payment clause. But if you enter before completing 60 years than the policies like Religare or apollo will not ask for co payment in any age. Apollo Optima restore will also suit you if premium is not a concern. Its maximum entry age is 65 years.

In case of your mom, you have to do some hit and trial as it depends on the underwriter to accept/reject a diabetic case . Apollo upfront rejects diabetic cases. I don’t know about max. You may try with some nationalised company which has good bandwidth to accept such cases with some loading on it.

Chk out http://goodmoneying.com/insurance-planning/health-insurance-for-parents . This might help you in some selection.

Thanks a lot for your review. I have a few questions, which I hope you would be able to clarify:

1. What is the claim settlement ratio of the policy?

2. The pre/ post hospitalisation amount is 15-20% of sum insured. Which sum is being considered? The individual cover, or inclusive of the floating cover?

3. What is the annual premium increment like? Is it age-slab linked, or something else?

Thanks for your help!

Siddharth thanks for liking the article. You answers are as below

1. I am not aware about the ratio but my personal experience with Max bupa has been very good. You may get the data on IRDA website.

2. the maximum pre/post cover for an individual would be 15-20% of individual cover Plus 15-20% of floater cover. for e.g 2 persons covered for 5 lakh individually and 10 lakh floater in gold plan. Pre post benefit will be Rs 1 lakh individually and Rs 2 lakh collectively.

3. Annual premium will be increased yearly and is not linked to any slabs.

Hope it helps.

Hi, Really your article gives good insights.. Do share the link or webpage where i can access other similar subjects.. Further i have below query :-

I am holding a policy of Max Bupa Health -Family for past 2 years. My renewal is due in Jan’15. Recently our family is extended with arrival of our Son. We are 3 members family (33yrs(Me),Wife 26Yrs,Son(2 Month)). Since we have to include our son i have been advised by Max to take Max Family first. I am ok for paying the premium (appx 16k) . Kindly advise which if its suitable for me based on below conditions:-

1. I am holding policy from my office (20 Lak cover)

2. This policy i am using just in case i utilise the corporate limit in full or during time i am switching jobs (though chances are remote)

3. I have not claimed maternity benefit from MAX but claimed from my office only

Waiting for your advice.

Thanks Arif for reading and liking my article. You may subscribe to my blog to be in touch with my views and other articles on different personal finance subjects.

Regarding your query, i think you should completely ignore your company policy while taking separate health cover. See though you are adequately covered by your employer and even chances of switching job is also remote, but still you have to understand that once you get diagnosed with some illness ( the probability increase with age), it will be difficult for you to get a new policy or increase the cover in existing policy. So its always advisable to get the affordable and adequate cover during the good times.

Hi,

I am looking for a health insurance policy for me(26) and my husband(33) which covers mternity benefits..after a long search i am thinking of finalizing Max bupa Family first silver plan…can you suggest me is it advisable to go for it and also any other plan which sutits my requirement….as you have mentioned earlier can you suggest me any policy tat doesnt have a copay after 60 yrs if the policy is continued….

Max bupa offers maternity benefit after 2 years of continuation, Apollo offers this after 4 continuos years. Apollo doesn’t ask for any co payment after any age except in sme specific senior citizen policies. You may go with any of these.

But i would advise you to go through and understand the terms and conditions carefully especially for the maternity benefit which you are specifically seeking for. so you should know what to expect from these.

Hi

Wish to have policy details for family

Me(38) wife (34) and two kids .

approx premimum for sliver plan

regards

Pnkj

Panakaj, you have to visit max bupa website for premium calculation

Hi,

I have an existing MAX BUPA Hearthbeat silver family floater policy for me and my spouse. My renewal is due in couple of days, I wish to upgrade my policy to GOLD keeping in mind the room benefits, etc. But the confusion is in that should i opt for 5 lac family floater or 2+3 lac family first (i.e. 2 lac sum insured for each individual and 3 lac as floater amount).

Please suggest.

Thanks

Hi Manikaran,

Currently i have Max bupa Family First which covers me and my wife with no kids.

Please suggest how Max bupa Family First is different from Max bupa Family Floater,

and which one is better.

Regards,

Ashish Jain

The difference is in the structure only. In family first you can add upto 13 relations in a single policy, but family floater is limited to your oen family only. Feature wise i don’t think there’s any difference.

hello sir

i am 27 year old and lookin for the family floater, there are 3 members in my family (mother 49 yeras, father 57 years and me). please guide me which policy would be best for me. MY MOTHER IS KNOWN FOR CASE OF HYPERTENSION, WE ARE LOOKING FOR THE COVER OF 3 LAKHS

1. apollo munich optima restore (mother and father ) AND INDIVISUAL POLICY FOR ME

2. MAX BUPA FAMILY FIRST (FOR ALL MEMBERS)

Arif to me both the companies are good. In max bupa do understand the co-payment feature after 60 years of age. Apollo is a good policy with a strict underwriting, so do ask them first as to how they will take up the case of hypertension.

Hello Sir,

I am looking for a health insurance with 10 lac cover for me 34 years and my wife 25 years. Please suggest a plan which is best for me in terms of feature, claim settlement and premium. I’m not looking for any special feature, but may be maternity benefits after some years. (no sublimit, no copay, refill, no claim bonus may be added advantage.

Thanks!

Max bupa Hearbeat should suit you, else you may also check Religare CARE

Hi Manikaran ,

thanks for this informative write up , i hope you will reply to my query

I am having MAX BUPA Heartbeat silver plan for myself(36) , wife (34), son(5) with 5 lakh each + 15 lakh floater . When i have purchased policy in 2012 its premium is around 15,000 , but at every year they increase the premium and now premium reached 20,000, with this pace by the time i turn 60+ , i can think of the premium in Lakhs . IS this general phenomena across health insurance plans/ co

when we started , there is option of interest free EMI from HDFC credit card , which they stops in 2013-2014 , Also as bonus every year , earlier they used to give ponts equal to premium amount , by which you can purchase some vouchers , which also they stops . I know purpose of buying policy is primarily health benefits , but still ,if you are getting some thing along it is good 🙂

OK , so my query is 1) Shall i continue with same policy 2) can you suggest me some alternates with in max /outside

just want to highlight that i was hospitalized in delhi for kidney stone operation in 2015 , and there service was good if not best ! will you suggest for port , to different plan , with less premium

Anand, Max Bupa is a good insurer. At least in my experience. And the Premium of Rs 20k in 36 years of age, with a separate cover of Rs 5 lakh each for all family members with Rs 15 lakh floater cover is not looking that high to me.

You may check Max Bupa’s Health companion policy with a floater cover of Rs 10 lakh for complete family and top it up with a super top-up plan from max Bupa only for Rs 10 lakh. The base cover will increase to Rs 20 lakh after 2 years with No Claim Bonus, and the additional top-up will support in case of emergency. Not sure about the premium cost. Just try it once.

Kidney stone is not a big issue.